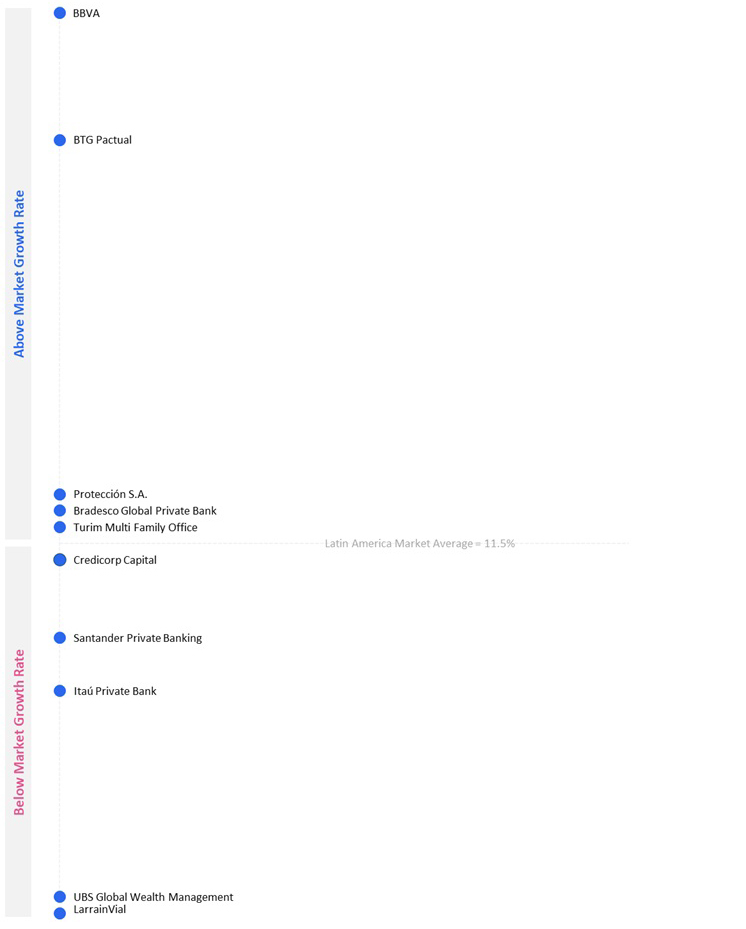

Latin America’s private banks and wealth managers grew assets under management by an average of 16% year-on-year to $752 billion in the year to 1H25, defying timid regional GDP growth and macroeconomic uncertainty. Brazilian heavyweights dominate the ranking, with BTG Pactual leading the pack after a 36% jump to $194.6 billion. But global players and regional specialists are carving out ground, and a more sophisticated wealth management ecosystem is taking shape across the region.

Latin America’s private banks and wealth managers showed strong momentum in the 12 months to 2Q25, according to Euromoney’s debut ranking of the region’s top institutions, with assets under management (AUM) rising by an average of 16% year-on-year to $752 billion.

AUM growth defied a mixed economic picture in Latin America. According to the World Bank, GDP growth in the region was sluggish at 2.4% in 2025, as sticky inflation in key markets such as Brazil and Mexico complicated the case for an easing of interest rates. Global trade tensions – in the form of US tariffs on major Latin American exports – also weighed on the lukewarm growth track record.

A region coming into its own

However, AUM growth in Latin America has been boosted by wealth accumulation associated with industries where the region has comparative advantages – such as agribusiness, energy, infrastructure and natural resources.

Meanwhile, the main MSCI benchmark of Latin America listed companies returned 54% in US dollar terms – higher than any other region. Finally, AUM growth in the region has been reinforced by rising sophistication of capital markets – increasing the likelihood of business monetisation for entrepreneurs – and the evolution of wealth planning and governance structures in these markets.

Brazilian heavyweights lead the pack

Euromoney’s Largest Private Banks in Latin America by AUM/NNA report reveals a landscape dominated by Brazilian institutions, commanding more than 70% of the top 10’s total AUM. The asset growth at these players has in many cases been aided by their vast retail networks and historical market depth, meaning they are often the first stop when it comes to capturing new wealth.

At the top of the ranking sits BTG Pactual with an impressive AUM jump of 36% to $194.6 billion. However, much of this growth has been inorganic, led by the acquisition of Julius Baer’s family office business in Brazil ($11 billion in AUM). In the period covered by Euromoney’s research, the bank also scooped up New York’s MY Safra ($391 million in AUM), Miami-based Greytown Advisors ($1 billion in AUM, much of it for UHNW clients from Central America), and Portland’s JGP Wealth Management ($3.4 billion in AUM).

These moves have helped to increase the bank’s penetration in ultra/high-net-worth (U/HNW) clients across Brazil, Chile, Colombia, the US, Portugal, the UK, Spain and Luxembourg. Strong hiring – BTG Pactual’s client-facing wealth management staff are up 33% since 2021 – combined with digital innovations such as AI-driven personalisation, have also fuelled strong organic net new assets (NNA).

Itaú Private Bank holds second place in Euromoney’s ranking at $175 billion in AUM, up a steady 6% year-on-year. In addition to bringing in senior hires from rivals such as Julius Baer and Credit Suisse/UBS, the bank has launched a number of tailored segments intended to address the specific needs of different client profiles. These include ‘next-gen’, designed to counter the industry-wide challenge of asset leakage following wealth transfers; ‘special’ for clients with BRL10 million to BRL20 million in assets; and ‘GPPC’ for ‘global professional private clients’ and single-family offices. The bank is also increasingly pushing into new Latin America markets including Chile, Colombia, Uruguay, Argentina and Paraguay with a unified onshore-offshore service model that emphasises hyper-personalised advice.

Within the Brazilian contingent, Bradesco Global Private Bank comes next, taking fifth place with a 16% year-on-year lead in AUM to $97.5 billion. This followed a restructuring that has unified its wealth operations under one vertical, encompassing Bradesco Prime (starting at BRL150,000 in assets); a new ‘principal’ client segment (clients with a monthly salary of BRL25,000 and above) and its UHNW global private bank arm.

Strong net new flows during the review period have also helped lifted Bradesco’s market share to what it estimates to be about 22%. With 14 offices across Brazil, plus outposts in Miami and Luxembourg, the bank now serves over 10,000 families with more than BRL$1 billion in assets. The bank’s philanthropy offering draws on the legacy of Fundação Bradesco, Brazil’s largest endowment, while client net promoter scores (NPS) hit 82, reflecting customer praise for Bradesco’s agile, personalised service.

Global players carve out niches

The largest foreign player in Latin America’s wealth space is UBS Global Wealth Management, at $149.7 billion in AUM. This 7% year-on-year gain underscores the value of the Swiss giant’s multi-shoring model spanning Brazil, Switzerland and the US – which has particularly resonated for regional clients seeking diversification across multiple global booking centres. Notable deals for the bank during the review period included a large, landmark unsecured loan to a Colombian billionaire family, as well as the milestone billions of dollars in gold and silver in derivatives trading in a single month. The world’s largest private bank has also focused on digital advances, including a simplified online client onboarding tool that has slashed account opening times, alongside AI pilots for client lifecycle management.

Madrid-based Santander Private Banking grew its Latin America AUM by 10% to $117.9 billion, backed by robust flows in net new money. Its Beyond Wealth global family office service launched in Spain, Brazil and the US, while a new Dubai outpost has helped the Spanish bank to taps wealth flows between Europe, the Middle East and Latin America. Santander’s AUM expansion has been supported by a fast-growing structured products offering, while revenue derived from its network business – specifically for cross-border clients – rose strongly, underscoring Santander’s role as a bridge between continents.

Rounding out our top 10 were pure-plays and regional specialists. Credicorp Capital (focused on Peru and Colombia) saw its AUM rise by 17.5% to $16.8 billion; Chile’s LarrainVial boosted AUM by 8% to $9.9 billion with a focus on the Andean nation’s mining wealth; while Brazil’s Turim Multi Family Office highlighted the growing appeal of the independent wealth management model in the region, with AUM up 17% to $6.9 billion.

Latin America’s fastest-growing private banks by NNA (1H25)

Learn more about the AUM rankings methodology. For more on our private banking benchmarking and insights, contact Euromoney’s head of private banking Daniel Shane.

More reports