Consolidation, southern European growth and the continuing dominance of Switzerland’s giant define Europe’s private banking landscape. Euromoney’s 2026 ranking of the continent’s 30 largest wealth managers by assets under management maps a sector where average AUM growth hit 14.1% in the 12 months to mid-2025 – outpacing the sluggish GDP expansion weighing on the broader European economy.

Europe may be grappling with geopolitical fragmentation, sluggish GDP expansion and persistent political uncertainty, yet Euromoney’s ranking of the continent’s 30 biggest private banks by assets under management (AUM) shows how its wealth engine continues to accelerate.

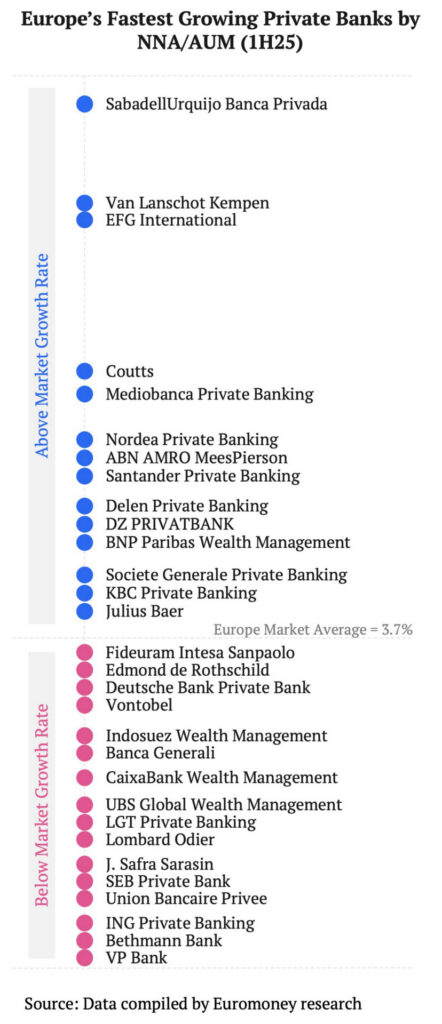

Average European AUM growth across the private banks featured in this report reached 14.1% in the 12 months to the end of 1H25, representing more than $680 billion in new client assets.

Against that backdrop, Euromoney’s performance ranking research reveals a sector reshaped by consolidation, competing strategic models and a clear geographic divergence between northern and southern Europe.

Scale, strategy and the battle for Europe

UBS Global Wealth Management continues to anchor the market, maintaining its wide lead as the region’s largest private bank with $1.8 trillion in European AUM, a 10% increase year-on-year. Its $37 billion of net new assets reflected the ongoing assimilation of Credit Suisse and UBS’s ability to turn global scale into productivity and efficiency gains.

In second place, with $485 billion in European AUM, comes Deutsche Bank Private Bank. The German bank has rebuilt momentum around its ‘Global Hausbank’ model, leveraging the combined capabilities of its investment bank, corporate bank and asset manager to deepen client relationships. Profitability and returns improved sharply in 2025, supported by strengthened coverage of ultra-high-net-worth (UHNW) families and entrepreneurs, and by selective hiring in core regions.

M&A is redrawing Europe’s competitive map

Consolidation continues to be a defining feature of Europe’s private banking landscape. BNP Paribas Wealth Management, fourth in the ranking, recorded $444 billion in European AUM and 16% annual growth. The bank strengthened its organic performance with a second quartile net new assets (NNA) performance, confirming its position as the eurozone’s most credible emerging wealth champion. But the acquisition of HSBC’s private banking operations in Germany, completed in late 2025, expanded the French bank’s reach in one of the continent’s most important wealth markets.

UBP’s 30% increase in European AUM to $196 billion was driven by its acquisition of Societe Generale’s Swiss and UK private banking operations, underscoring how targeted deals can rapidly reshape scale positions. LGT Private Banking also leaned on acquisitions, including abrdn’s UK wealth business.

In the Benelux region, consolidation has become the central engine of growth. Delen Private Bank’s 39% expansion – fuelled partly by its acquisition of the Netherlands’ Servatus Vermogensmanagement – reflects a strategic environment in which smaller players increasingly rely on transactions to achieve scale efficiencies, strengthen product platforms and compete with larger cross border institutions.

Southern Europe: The continent’s growth engine

While Switzerland and northern Europe continue to dominate at the top end of our performance ranking bench, the data also shows strong organic growth is now coming from southern Europe.

Fideuram Intesa Sanpaolo, Europe’s second largest private bank by European AUM, delivered 17% expansion, adding $14 billion in net new money. Its advisory centric, relationship driven model and deep penetration of Italian mass affluent and affluent households provide a structural advantage.

Santander Private Banking posted similarly impressive results. Its AUM grew 21% to $251 billion, and the bank ranked in the first quartile for NNA performance. What distinguishes Santander from many regional peers is its connectivity to Latin America, the US and the Middle East.

CaixaBank Wealth Management, Spain’s most powerful domestic private banking franchise, expanded AUM by 17% to $207 billion. Its growth was supported by robust distribution through its extensive retail network and strong adoption of discretionary mandates, underscoring the effectiveness of its integrated banking–wealth model.

Looking ahead

Europe’s private banking sector is entering a period of rapid strategic divergence. Southern European banks are gaining ground thanks to strong organic inflows and modernised advisory models. Consolidation is reshaping competitive positions, creating new regional champions capable of competing with the global giants. Scale, technology investment, adviser productivity and the ability to combine organic growth with disciplined M&A will determine the winners when it comes to gaining wallet share in the continent.

Learn more about the AUM rankings methodology. For more on our private banking benchmarking and insights, contact Euromoney’s head of private banking Daniel Shane.

More reports