Digital banking in the Middle East has evolved from an emerging trend into a central pillar of the region’s economic transformation. Across the region, the shift from branch-led to digitally native retail banking has been powered by ambitious national visions, advanced payments infrastructure and a young, mobile-first population that expects financial services to match the speed of the digital economy.

For millions of customers, the app is no longer a complement to the bank – it is the bank. Nowhere is this transformation more visible than in the UAE and Saudi Arabia, where digital adoption, regulatory modernisation and investment in open banking and artificial intelligence (AI) have accelerated at a remarkable pace. Kuwait has become a proving ground for youth-focused innovation, while Bahrain continues to punch above its weight in regulatory agility and instant payments infrastructure. Together, these markets illustrate how government policy ambition and private sector execution are converging to redefine what digital retail banking can achieve.

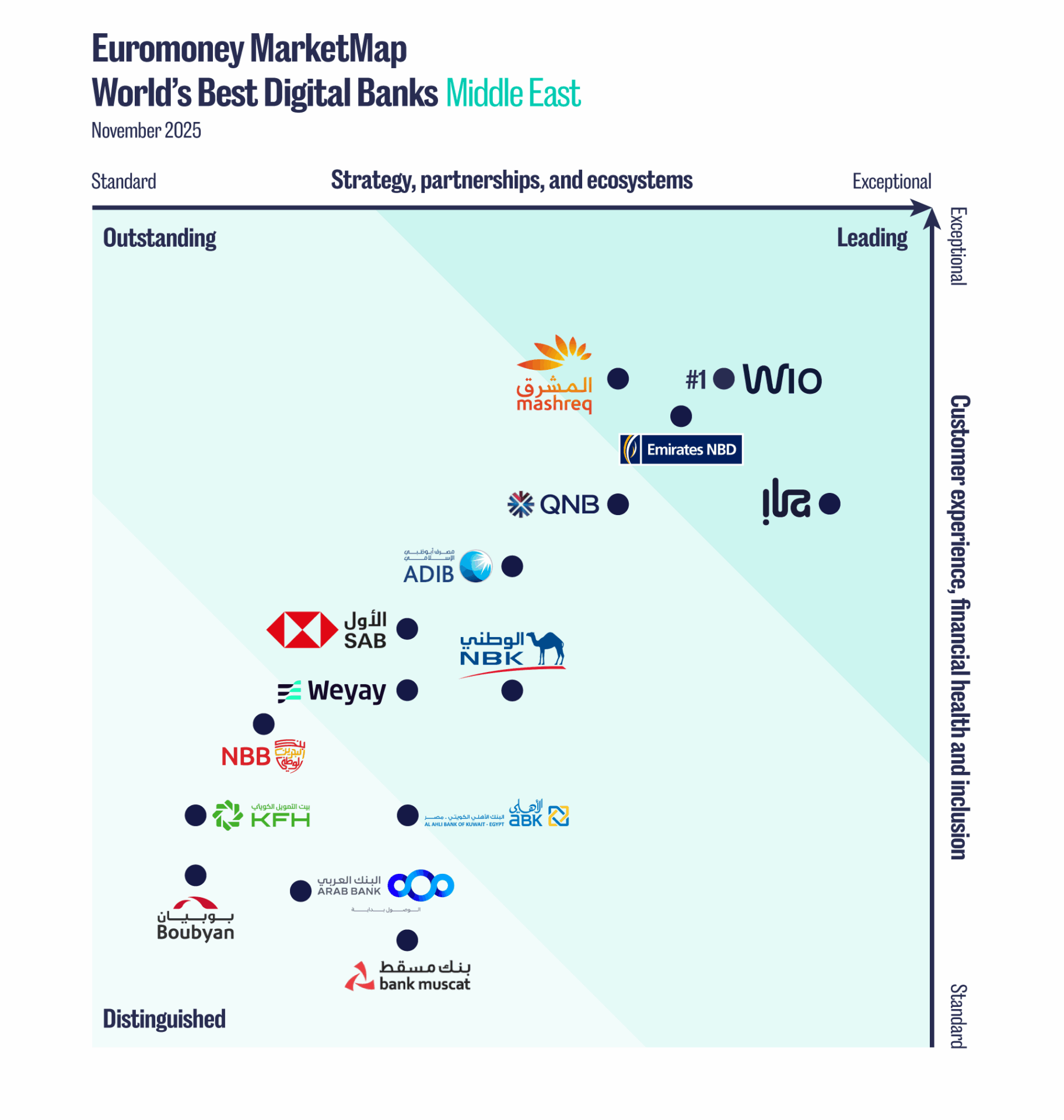

The region’s standout institutions combine technological sophistication with disciplined delivery. Wio Bank has set a new benchmark for how a digital-only model can achieve scale and profitability within just three years, uniting saving, spending and investing within one ecosystem that is now integral to everyday financial life in the UAE. Emirates NBD has demonstrated how a large incumbent can operate with precision at scale, delivering AI-driven personalisation, visible security and one of the region’s most comprehensive mobile experiences. In Bahrain, ila Bank has proven that even in smaller markets, user-centric design and frictionless onboarding can achieve regional relevance. Mashreq continues to bridge both worlds – a legacy institution reengineered with the agility of a challenger, embedding automation and partnerships across its platforms.

This report explores what sets the region’s 15 leading digital retail banks apart through four thematic lenses reflecting Euromoney’s digital benchmarking criteria:

- Paths to success

How are banks translating digital visions into competitive advantage? What distinguishes those combining speed, sustainability and profitability in their digital transformation journeys?

- Ecosystems and open banking

How are Middle Eastern banks evolving from product providers to platform orchestrators? What new models of collaboration with fintechs and partners are defining the region’s retail banking environment? Which is the best approach to third-party services?

- Customer experience in the mobile and AI age

How are banks reimagining onboarding, engagement and protection in an age of AI-driven personalisation? What best practices are emerging as the foundations of digital trust? What are the key steps to boosting digital banking security?

- Financial health and inclusion

What are neobanks doing to widen access to banking and credit? Which incumbents are innovating around financial health while ensuring digital access? How can digital tools encourage us to save and invest?

The findings reveal a region where strategy, ecosystem reach, experience and empowerment have converged into a new model of digital excellence. Middle Eastern banks are showing that technology’s true value lies not in automation but in intelligence, inclusion and trust. They are turning innovation into purpose, execution into progress and scale into societal impact.

As the next wave of digital banking takes shape, this report provides a clear view of where the Middle East now stands in digital retail banking – and where its leaders are taking it next. The region is no longer adapting to global standards – it is helping to set them.

More reports

The MarketMap methodology

This report is based on Euromoney’s assessment of retail banks in the Middle East as part of its annual research cycle. It combines qualitative insights from interviews with senior executives – CEOs and other C-suite executives, heads of retail banking and digital banking, heads of strategy and transformation, among others – with written submissions from institutions. The research covers the capabilities of digital-focused incumbent banks and their digital-only subsidiaries, as well as standalone digital-only challenger banks.

The quantitative analysis is grounded in a proprietary scoring framework that evaluates each bank against six criteria driving excellence in the fiercely competitive and fast-changing world of digital banking for consumers. The Middle East’s best digital banks MarketMap highlights 15 top-performing retail banks, across two central pillars:

1. Strategy, partnerships and ecosystems

This pillar examines the most effective and successful digital banking strategies, financial and technology partnerships, and infrastructure enhancements that support the digital transformation and growth of the banking industry.

» Strategic execution of digital banking strategies, including growth and financial success;

» Ecosystem development including digital partnerships and open banking integration;

» Innovative consumer benefits and rewards programmes promoting customer loyalty.

2. Customer experience, financial health and inclusion

This pillar examines improvements to customer experience including onboarding and digital customer support tools, anti-fraud and banking security tools and initiatives, as well as products and services promoting financial empowerment and well-being, including savings, budgeting and financial planning features.

» Customer onboarding processes, digital support services and initiatives promoting digital product use;

» Banking security measures including cyber-resilience and anti-fraud measures, promoting trust;

» Tools and programmes to foster wider financial-sector access and better financial habits.

Due to its general-purpose nature, the adoption of AI – including generative and agentic AI – was considered within each section.

Each bank is evaluated using a consistent 0–100 scoring framework across all six dimensions. Banks are benchmarked using evidence from documentation reviews, structured expert interviews, platform demos and usage data.

Based on their performance across the pillars, the top-performing institutions feature in one of three tiers:

» Leaders, who are ahead in both axes;

» Outstanding, who demonstrate excellence in one of these two axes;

» Distinguished, who offer strong capabilities across multiple digital fronts.

Euromoney MarketMap: The Middle East’s best digital banks

Wio Bank

In just over three years, the UAE’s first platform bank has evolved from a challenger concept into a full-spectrum digital ecosystem across retail, small and medium-sized enterprises (SME) and personal wealth. Built on a cloud-native, microservices-based architecture, Wio unites saving, spending, credit and investing within one integrated experience. Its engagement levels are exceptional: around 89% of accounts are actively funded, and its net promoter score (NPS) of 74 ranks among the region’s highest. Digital from inception, ecosystem-driven and simple to use, Wio’s next test will be sustaining intimacy as customer volumes and partnerships expand – ensuring transparency and trust remain the foundation of its growth.

Emirates NBD

Emirates NBD has set the regional benchmark for digital execution at scale. Guided by its i3 framework – instant, intelligent and innovative – the bank has embedded automation, AI and customer experience (CX) transformation throughout its operations. By end-2024, mobile banking app ENBD X had achieved a 91% customer adoption rate and delivered more than 200 services. Visible, behaviour-based controls helped cut ENBD X fraud cases and total volume tenfold year-on-year in Q4 2024. As transaction volumes and customer expectations rise, the opportunity lies in extending this precision-engineered CX architecture beyond bank-owned platforms.

ila Bank

Bahrain’s ila Bank, designed for lifestyle-led, mobile-first customers, has sustained exceptional momentum since launching in 2019, with monthly app users up more than 100% and mobile sessions up 120% between mid-2023 and end-2024. Its three-minute, electronic know-your-customer (eKYC)-enabled account-opening journey exemplifies frictionless design, while open banking APIs enable secure connections with wallets and fintech platforms. Expansion into Jordan and Egypt demonstrates the scalability of its cloud-based model. By prioritising simplicity, cultural relevance and continuous enhancement over product proliferation, ila has built durable engagement. The challenge now is to preserve that user-centric ethos as its regional footprint expands.

Mashreq

Mashreq demonstrates how a legacy institution can operate like a digital challenger. Nearly all new-to-bank customers now onboard digitally, supported by extensive automation and AI across origination and servicing. Its platform strategy extends beyond its own channels, from embedded insurance marketplaces to banking-as-a-service (BaaS) collaborations with telcos. Intelligent automation has streamlined operations, while data-driven design personalises experiences across segments. By pairing innovation discipline with ecosystem ambition, Mashreq has shown that legacy scale can evolve into platform agility. The next step is exporting this model consistently across its international markets.

Qatar National Bank (QNB)

QNB has transformed retail banking in Qatar through scale and simplicity. It was the first Qatari bank to offer fully digital account opening, compressing onboarding to minutes and linking instantly to virtual cards. Partnerships extend its reach beyond bank channels – from wallet interoperability and instant payments to blockchain-enabled remittances. The bank offers Qatar’s broadest digital payment suite, including Apple Pay, Google Pay, Samsung Wallet and QR Pay by QNB, plus the QNB Pay Wallet has been integrated with the national mobile payment system. The next opportunity is deeper personalisation – leveraging its vast data assets to provide proactive, insight-led experiences across its footprint.

Abu Dhabi Islamic Bank (ADIB)

ADIB has demonstrated what faith-based digital banking can achieve at scale. In 2024, digital channels drove most of its retail growth, with more than 216,000 new customers onboarded through journeys integrating biometric verification and government databases. Its ‘branch in hand’ digital banking channels deliver more than 150 straight-through services, and 96.6% of customers are digitally registered. ADIB’s internal development team uses generative AI and automation-driven design tools to accelerate product delivery, while innovations such as fractional sukuks have made retail investment more accessible. The next step is expanding its open banking and ecosystem capabilities to match its digital execution strength.

National Bank of Kuwait (NBK)

NBK continues to pair scale with discipline in its digital evolution. Its mobile app – rated highly for customer satisfaction and usability – has become the main gateway for everyday banking, integrating geolocation, analytics and tailored offers to simplify decisions and improve engagement. The re-engineered Al Jawhara ecosystem offers instant, gamified savings to millions of users, while Al Jawhara Junior introduces children to healthy digital financial habits. The next opportunity is to extend its analytics and payments strengths into lifestyle ecosystems that deliver deeper, daily relevance for users.

Saudi Awwal Bank (SAB)

SAB has emerged as one of Saudi Arabia’s most comprehensive digital transformation stories. Following the full integration of Saudi British Bank and Alawwal Bank in 2021, the board approved a SAR1.5 billion investment in technology, helping build one of the Kingdom’s top-rated retail-banking apps. SAB 360° brings budgeting, insights and financial education together in one ecosystem. Having launched open banking integrations and behavioural-biometric fraud controls, SAB’s next opportunity lies in deepening data-driven innovation and ecosystem partnerships to sustain its leadership in Saudi Arabia’s evolving digital finance landscape.

Weyay Bank

As Kuwait’s first fully digital bank, Weyay has moved swiftly from novelty to norm. Targeting digital-native youth, it now serves about a third of the segment, with customer numbers up 34% year-on-year in 2024. Its three-step onboarding, integrated with Kuwait’s national ID system, sets a benchmark for simplicity, while features such as Saving Pots and the gamified Jeel app for children promote healthy financial habits. Lifestyle partnerships drive engagement through relevance rather than rates. Further potential lies in deepening its ecosystem and personalisation capabilities – using data, partnerships and purpose-led design to make youth banking smarter, greener and more connected.

Al Ahli Bank of Kuwait (ABK)

ABK’s digital transformation blends bold physical-digital innovation with disciplined execution. Its hologram-equipped digital branch and ‘digital island’ kiosks highlight the bank’s pioneering approach to phygital banking in Kuwait, while a revamped mobile app – now with more than 100,000 active users – combines biometric security and personalised financial dashboards with significantly enhanced processing speeds. ABK is now focused on integrating its financial services more deeply into digital ecosystems, as it prepares to launch AI-powered personalisation and new finance capabilities through strategic partnerships. Turning these initiatives into scalable, data-driven value creation for customers comes next.

National Bank of Bahrain (NBB)

NBB’s transformation blends customer-centric discipline with social purpose. Its emphasis on CX and security has earned national recognition: device binding, in-app soft tokens and app shielding have helped eliminate mobile-app fraud incidents in 2024. The Yalla Family Account promotes financial inclusion and literacy among young customers, while digital onboarding and instant loan approvals make everyday banking faster, simpler and more secure. These advances reflect a philosophy that sees technology as empowerment rather than disruption. The next step is leveraging its secure, trusted platform and environmental, social and governance (ESG) credentials to drive deeper inclusion and purpose-led innovation across Bahrain’s financial landscape.

Kuwait Finance House (KFH)

KFH is redefining Islamic banking for a digital generation through Tam, its fully Shariah-compliant digital banking platform launched in late 2023. Tam combines instant onboarding and virtual cards with gamified features such as badges, cashback and peer-to-peer transfers, creating a community-style experience for younger users. Built on KFH’s core infrastructure, Tam benefits from biometric authentication, secure verification processes and real-time payments through the WAMD and AFAQ networks. The next step is deepening Tam’s role as a fintech and lifestyle hub – expanding its partnerships and data-led guidance beyond gamification to drive long-term financial empowerment and inclusion across the fast-growing halal economy.

Bank Muscat

Oman’s Bank Muscat has turned its market-leading scale into a platform for national digital inclusion. Under its three-year medium-term strategic plan, it digitised more than 80% of services across mobile and internet channels, surpassing targets ahead of schedule. AI-driven analytics and fraud detection now underpin operations, while the Maliyat financial literacy platform has empowered more than 23,000 users across Oman. Continuous enhancements to KYC, payments and remittances reflect a commitment to simplicity and access. Linking inclusion with insight will take it further – using its data and reach to measure financial wellness outcomes and extend digital enablement to underserved segments.

Boubyan Bank

Kuwait’s Boubyan has delivered a digital strategy grounded in Islamic values and small business empowerment. Its ePay platform – enhanced in 2024 with subscription and scheduled payment features – has become a leading SME collection tool, while eRent extends Boubyan’s reach into the property ecosystem. Results from 2024 were clear: SME clients up 165%; digital usage up 57%; and card spending up 104%. By concentrating on the needs of the real economy, Boubyan has demonstrated the value of purposeful execution. There is further potential in translating rich transaction data into actionable insights that help entrepreneurs manage growth, risk and cashflow more intelligently.

Arab Bank

Jordan-based Arab Bank’s regional network gives it impressive scale, yet its digital execution shows the agility of a challenger. Its in-house AI credit-scoring model – now live across Jordan, UAE and Egypt – delivers rapid, explainable lending decisions, reducing loan approval times to minutes while lowering default risk. The bilingual gen-AI frontliners assistant is transforming service quality, giving staff real-time access to data across systems and saving thousands of hours each year. Having proven the value of AI internally, further potential lies in applying these capabilities across more customer journeys and markets, supported by deeper fintech collaboration and open-API integration.

The digital paths to banking success

From roadmaps to results: Retail strategies that deliver

For more than a decade, digital transformation has been the central ambition of Middle East retail banking. Every major institution set out roadmaps promising to reinvent customer journeys, migrate transactions online and capture the loyalty of a digital-native generation. By 2025, the question is no longer who has the boldest vision – the real test is who has executed those strategies; embedding them into daily operations and producing measurable results.

The evidence reveals a region where digital execution is now tangible. Leaders are not just investing in technology – they are delivering adoption at scale, embedding digital into their operating models and building platforms that customers actively prefer. Across the region, banks are showing how digital strategies can be translated into outcomes that enhance performance and reshape customer behaviour.

Scale as a measure of strategic impact

Perhaps the most striking proof of strategy executed well is scale – not a handful of projects and services but millions of transactions migrated online, and customers adopting digital as their default.

Wio Bank exemplifies this. When it launched in 2022 as the UAE’s first platform bank, its strategy was bold: to build an integrated proposition that could serve retail customers and SMEs in a market dominated by established giants. Execution has been emphatic. In its first 17 months of operation, Wio signed up more than 140,000 retail customers, and states that approximately 89% of accounts are actively funded, which is high compared with global benchmarks for neobanks.

By end-2024, Wio had acquired more than 90,000 SME clients, with around 5,000 new accounts opened each month. Its core focus is on micro and small enterprises, freelancers and sole traders, though features such as multi-user workflows also enable it to accommodate larger SMEs with more complex needs. According to the bank, two in five new businesses in the UAE now choose Wio Business, underscoring how execution has made it integral to the economy’s most dynamic segment. Customer deposits have trebled, catapulting Wio into the UAE’s top 10 banks by retail and SME deposits.

Crucially, Wio has combined growth with profitability, breaking into the ranks of the world’s top-10 most profitable neobanks in 2024 – a notable achievement in a sector where many challengers still struggle to reach breakeven. Its NPS of 74 is another signal of delivery: strategy has translated not only into adoption but into customer advocacy. The bank estimates that three out of five new retail and business customers are a result of referrals from existing users, despite Wio having no referral incentive programme.

The implication for the wider industry is clear: Wio shows that with the right execution model – digital from inception, ecosystem-driven and relentlessly focused on ease of use – a new entrant can scale faster in the Middle East than in many mature markets, aided by supportive regulation, digital-savvy populations and rising demand from individuals and small businesses.

Also based in the UAE, Emirates NBD demonstrates how a large incumbent can execute digital transformation at scale. Emirates NBD has anchored its digital transformation around two complementary strategies: the i3 banking framework – instant, intelligent and innovative – and a holistic CX transformation programme. The i3 strategy sets clear priorities: instant banking through advanced automation and straight-through processing; intelligent banking by harnessing AI, analytics and data-driven personalisation; and innovative banking by developing new propositions, ecosystems and business models.

Execution has been visible across these pillars. On ‘instant’, the bank’s mobile app, ENBD X, now offers more than 150 instant services, with 98% of new current accounts opened via mobile or assisted tablet banking. On ‘intelligent’, the bank has activated more contextual push notifications targeted at the exact time of need and enabled travel mode on ENBD X to notify users of travel-related features when overseas. On ‘innovative’, it has launched features such as Liv Lite – a family finance app – and gamified deposits, while investing in digital asset custody and new ecosystem partnerships.

The CX transformation programme, launched in 2023, reinforces this execution by aligning journeys, governance and culture around customer experience. With more than Dh200 million invested, more than 50 journeys digitised in 2024 and 163 digital services live on the app, 90% of service requests are now handled digitally.

These results show how Emirates NBD has translated its strategic frameworks into measurable outcomes. ENDB X adoption has reached 91% across its customer base, while the number of active customers on digital channels increased by 30% year-on-year in 2024. The i3 and CX strategies have not only been articulated but delivered, embedding digital and customer experience at the centre of the bank’s operating model.

Mashreq, the UAE’s largest privately held bank, has delivered another notable story of digital strategy execution. Despite being established nearly 60 years ago and ranking as the UAE’s fifth largest bank by assets, Mashreq positions itself as a challenger bank with a digital-first mindset.

We are focused on being digitally native, which means embedding technology into processes rather than simply digitising manual ones. This shift demands AI literacy, new ways of working, and rethinking roles and risk models

Mohamed Abdel Razek, group head of technology, transformation and information, Mashreq

For Mashreq, execution has meant embedding digital origination throughout the customer lifecycle. Almost every new-to-bank customer onboards digitally, with the bank investing heavily in machine-learning and AI solutions to avoid friction and minimise the need for human intervention at any stage of the process. Its digital investments have been accompanied by efforts to actively reduce the branch network, with only five full-service units and 12 electronic service units now serving approximately 1.3 million customers across the Emirates.

The gains are clear: lower cost-to-serve, higher acquisition velocity and an operating model resilient to market shocks. In recent years, Mashreq has expanded its digital retail model into large, underbanked markets such as Egypt and Pakistan, using a single, cloud-based platform designed for scalability. The bank uses as much common code as possible in these international expansions, with the remaining localised to align with local regulatory requirements.

The experience of Emirates NBD and Mashreq shows that Gulf incumbents are not constrained by legacy models. With disciplined execution, they have re-engineered operations to meet the demands of fast-digitising markets.

Digital-only banks: strategy and execution intertwined

For all-digital banks, execution is inseparable from strategy – success or failure depends on converting design into adoption.

Weyay Bank in Kuwait has achieved this with speed. Launched in late 2021 as a fully owned subsidiary of the National Bank of Kuwait, it is designed to target younger, digital-native customers, with a focus on seamless onboarding, secure and transparent services, and products designed to encourage healthy financial habits. Execution has been evident in the numbers: Weyay now holds a 36% market share in the youth segment, with total digital customers growing by 34% year-on-year in 2024.

Its three-step onboarding process, integrated with Kuwait’s national digital ID system, illustrates strategy delivered in practice: removing friction while ensuring security. Its diverse product set – from Saving Pots to Jeel, a gamified banking and financial literacy app for children aged eight to 14 – shows how strategic intent to foster long-term loyalty has been executed in real offerings that resonate with customers.

For ila Bank in Bahrain, execution has been about proving that a small-market, digital-only bank can achieve sustainable adoption. Launched in 2019 as a subsidiary of wholesale banking incumbent Bank ABC, it was designed to target retail customers seeking seamless customer journeys integrated with their lifestyles. During the past six years, ila has shown that its vision can be translated into consistent growth. By end-2024, ila reported an increase in monthly app users of more than 100% since May 2023, over 530% growth in customer onboarding since January 2023, and a 242% rise in customer deposits since December 2021. The lesson here is not just about technology but about cultural fit: ila’s execution demonstrates that when digital design matches customer expectations, adoption follows naturally. Buoyed by its success in Bahrain, ila has since successfully expanded its digital-only model to Jordan and Egypt.

Strategies executed with purpose

Execution is not only about scale. For some banks, it is about delivering strategies that carve out a distinct competitive position.

Boubyan Bank has chosen this route. Its strategy has been to become the Islamic bank of choice for digital-first customers, with a strong emphasis on SMEs – particularly small enterprises operating in key segments such as retail, wholesale, hospitality and real estate. Execution has been visible: SME client numbers rose 165% year-on-year in 2024, digital channel usage by 57% and credit card usage by 104%. Its ePay platform for collections, enhanced in 2024 with tailored subscription models and Apple Pay support, has become the most popular payment solution for SMEs in Kuwait, while its eRent property management system, which is integrated with the wider banking platform, has extended Boubyan’s reach into the real estate ecosystem.

By focusing on small businesses, Boubyan has captured a segment often underserved by larger incumbents, translating strategy into measurable adoption and loyalty.

Regional patterns in digital strategy execution

What emerges across these cases is a regional picture where digital banking strategies are no longer aspirational statements but embedded operating models.

The most advanced banks – whether recent entrants such as Wio and ila or incumbents such as Emirates NBD and Mashreq – have achieved digital adoption and penetration levels that place them firmly at the forefront of the regional leadership pack.

But purpose also matters. Boubyan shows how strategy executed with focus – in this case, small enterprises and Islamic banking – can create a distinct market position. When translated into measurable outcomes, these choices differentiate banks in highly competitive markets. Taken together, these themes position the Middle East as one of the world’s most fertile proving grounds for digital retail banking.

New partnerships, growing ecosystems

From apps to ecosystems: The next battleground for Middle East banks

The first wave of digital retail banking in the Middle East focused on digitising existing processes: moving journeys online, building apps and streamlining onboarding. Those efforts were necessary, but they were largely inward-looking. Today, competitive advantage is increasingly defined by how well banks connect beyond their own channels.

Banks must now act as orchestrators of ecosystems. Instead of trying to own every customer interaction, they are embedding services into the platforms where people already spend their time and money. Open banking provides the technical rails for much of this shift, while loyalty schemes, fintech collaborations and lifestyle partnerships have become the visible levers of customer engagement.

This shift is no longer optional. Ecosystems generate richer data, deepen loyalty and open new revenue streams beyond traditional lending and deposits. For retail banks across the Middle East, the transition from closed silos to connected ecosystems represents the new frontier of competition.

Meeting customers at their point of need

This shift is driven in part by changing customer expectations, especially among younger digital users who expect financial tools to surface instantly, in context and inside the digital journeys they already inhabit. Success now depends not only on integrating with external platforms but also on overhauling internal architecture. Adopting API-first, real-time, partner-ready infrastructure ensures services are agile enough to appear wherever and whenever customers need them most.

For example, UAE-based Mashreq has introduced an insurance marketplace module within the Mashreq app, offering travel insurance to customers via API integration with insurers. Customers are provided with customisable, competitively priced insurance packages covering various travel-related risks and offering wide-ranging geographic and group coverage options. In the second half of 2024, this feature attracted 25,000 new leads, with a 10% conversion rate.

Mashreq’s platform orchestration is evident in Egypt through BaaS initiatives such as e&Mashreq NEO, enabling millions of telecom subscribers to open and manage bank accounts without leaving the My Etisalat app. The model repurposed Mashreq NEO Egypt’s modular digital capabilities into software development kits (SDKs), embedded directly into the telco platform.

Launched in Q2 2024, the service had attracted more than 280,000 new accounts by January 2025, with an STP rate exceeding 90%. By eliminating the gap between everyday digital activity and formal banking, the initiative has also widened access to financial services among previously underserved segments, highlighting the role of BaaS in advancing inclusion in a large, underbanked retail market.

Elsewhere in the region, Qatar National Bank (QNB) has broadened its digital ecosystem through partnerships and platform integrations that extend retail banking beyond its own channels. Its collaboration with Ooredoo Mobile Money enables customers to move funds directly between bank accounts and telco wallets for everyday transactions. QNB introduced a first-to-market Ripple-based remittance service in Qatar, facilitating instant cross-border transfers via blockchain to key corridors such as the Philippines and Turkey. In parallel, the bank’s QNB Pay Wallet supports the national Qatar Mobile Payment System QR standard and is available to non-customers and visitors as well as QNB account holders – evidence of a strategy that uses national payment rails to project influence across the wider consumer economy.

Building value from open banking

In Saudi Arabia, open banking has moved beyond regulatory compliance for Saudi Awwal Bank (SAB). The Saudi Central Bank issued its open banking framework in 2022 with a first phase focused on account information services (AIS), followed in 2024 by payment initiation services (PIS). In line with this roadmap, SAB has already enabled and launched AIS with multiple fintech partners, enabling customers to share their financial data securely with licensed third-party providers. Work is now under way on PIS, opening the way for fintechs to initiate payments on behalf of SAB’s customers.

SAB has gone further by tying its strategy to fintech investment, building an ecosystem of valuable synergies that accelerate growth opportunities.

We’re not just interested in partnerships with fintechs, but also in investing in them – particularly in areas that accelerate the pace of financial innovation such as open banking and embedded finance, where we plan to use the technology ourselves to enhance our value proposition

Tony Cripps, managing director and CEO, SAB

To date, three of the 14 fintechs in which SAB has invested through its direct and specialised funds focused on the enablement of strategic growth opportunities and disruptive commercial business models – from revenue-sharing and referral frameworks that strengthen fintech partnerships to infrastructure supporting SAB’s BaaS and embedded finance capabilities. This approach ensures that SAB is not only integrating with new players but also helping to shape the ecosystem in which they operate.

In Bahrain, ila Bank has similarly approached open banking as a growth opportunity rather than a compliance burden. Launched less than a year before the country’s open banking framework came into effect in late 2020, ila built its platform around APIs that allow customers to share account information securely with approved third-party providers and to initiate payments from non-bank platforms. These capabilities have enabled collaborations with fintechs offering budgeting, wallet and aggregation tools, giving customers more personalised financial management while keeping control of their data. By embedding its infrastructure into external applications, ila has enhanced the relevance of a relatively new domestic challenger, showing how open banking can amplify reach and accelerate adoption.

Turning rewards into retention

Alongside open banking’s technical foundations, reward ecosystems have become the customer-facing battleground for loyalty in digital retail banking. The leading digital players in the region are using partnerships and campaigns not just to hand out points, but to hardwire themselves into customers’ everyday spending habits. By linking financial activity with lifestyle benefits and discounts, they are creating incentives that drive adoption, encourage higher transaction volumes and keep customers coming back.

In the UAE, Wio has used partnerships with everyday consumer brands to deepen engagement and encourage repeat use. Structured campaigns with food delivery platform Talabat, supermarket chain Carrefour, e-commerce firm Noon, travel booking platform Trip.com and ride-hailing and delivery app Careem tied financial activity to tangible benefits such as discounts on spending and bundled memberships such as Talabat Pro. These offers were designed to boost adoption, raise average transaction spend per customer and help build brand advocacy. Wio’s strategy to link rewards directly to daily consumption patterns has created incentives for customers to route more of their spending through the bank, strengthening loyalty in a competitive retail market.

In Kuwait, Weyay has applied the same logic to the youth segment, recognising that younger customers are less motivated by traditional product features than by lifestyle value. The bank has partnered with brand franchise group Alshaya to launch the co-branded Weyay Aura prepaid card, which offers a dual-reward structure: cashback on spending across Alshaya’s retail brands as well as on everyday purchases more broadly. Complementing this, the bank’s Select programme provides university students with discounts and benefits designed around their lifestyle and spending habits. By embedding itself in the networks most relevant to students and young professionals, Weyay aims to turn early engagement into lasting loyalty.

Kuwait Finance House (KFH), meanwhile, has fused loyalty with Shariah principles through Tam, its fully digital Islamic bank. Here, rewards are integrated with gamification and social features, so banking feels more like a lifestyle app than a utility. Customers earn badges for positive financial habits and cashback for transactions, while peer-to-peer transfers and merchant tie-ups add a social layer to everyday transactions. By combining these features with strict Shariah compliance, KFH has built a distinctive model that appeals to a digital-native generation seeking engagement, community and values-driven finance.

The next phase of competition

The rise of ecosystems and open banking marks a fundamental shift in how retail banks in the Middle East position themselves. The most advanced institutions are already moving away from a product-provider mindset towards operating as nodes in wider networks. The prize is richer data, deeper engagement and a reach that extends well beyond their own digital channels.

While many of the earliest open banking wins in the region have been in corporate and payments infrastructure, retail applications are still at a relatively early stage – making developer experience, partner onboarding and clear consumer value propositions the next battleground. The coming years will determine how effectively banks can translate regulatory frameworks into scalable, customer-facing use cases.

The trajectory is clear: the winners will be those that orchestrate ecosystems with precision, blending open banking infrastructure with compelling customer-facing partnerships. Banks that succeed will weave themselves so seamlessly into commerce, lifestyle and digital platforms that financial services become invisible – ever-present, trusted and indispensable.

Customer experience in the new era

CX as the visible edge of digital strategy

In digital retail banking, customer experience (CX) is where strategy becomes tangible. The best-designed platforms and the heaviest technology investments only matter if they translate into interactions that feel easy, empathetic and secure. From onboarding to the resolution of a query or the reassurance of a fraud alert, CX is the point at which customer adoption is either won or lost.

The Middle East’s leading retail banks recognise that CX is no longer about incremental improvements. With most daily banking now conducted on digital channels, CX is the brand. Banks across the region have re-engineered their customer journeys to reduce friction, anticipate intent and build visible trust.

The region’s leaders are showing that the hallmarks of strong CX are clear: effortless onboarding at the outset; support that listens in real time; and security built visibly into every interaction.

From friction to funnel: Seamless onboarding

Account opening was once the industry’s biggest bottleneck, where enthusiasm often stalled under paperwork and compliance. The combination of progressive regulation and digital innovation has now turned onboarding into a moment of differentiation, where banks compete to make first impressions fast, simple and trustworthy.

QNB illustrates this transformation. In 2024, it became the first bank in Qatar to offer fully digital account opening, allowing new customers to complete the entire process in a few minutes – from identity verification to receiving a virtual card and instant access to mobile banking. Designed to eliminate the need for any branch interaction, the service combines simplicity with advanced security, turning a compliance-heavy process into an effortless entry point.

In Bahrain, ila Bank has positioned itself as a mobile-only, lifestyle-led digital bank, offering onboarding that can be completed in just three minutes using advanced facial recognition and eKYC with only an ID and a selfie. With no physical branches, ila is built entirely around its app, designed to resonate with younger, tech-native customers while also appealing to broader demographics. Its positioning has been reinforced through lifestyle-focused partnerships such as the Gulf Air Mastercard and Booking.com offers, which are intended to incentivise onboarding and product usage. The result is a branchless model in which rapid digital entry serves as the foundation for deeper customer engagement.

Elsewhere, ADIB in the UAE has enhanced its account-opening experience by combining biometric verification with government infrastructure. In 2024, the bank onboarded 216,000 new customers, supported by a simplified digital journey that more than halved the number of steps required. Customers authenticate their identity through facial scans linked to UAE government databases, ensuring accuracy without the need to upload documents.

The wider trend across the region is that onboarding has shifted from being a compliance burden to a strategic lever for growth. Regulatory frameworks, national ID systems, cloud-native design and targeted marketing are converging to make account opening an exercise in building trust from the first click.

Proactive support across channels

If onboarding sets the tone, ongoing support is where loyalty is earned or eroded. Across the Middle East, banks are moving beyond reactive service models to create support that is proactive, integrated and empathetic.

Mashreq in the UAE is at the forefront of embedding AI directly into customer support. Its AI-powered virtual assistant is not designed simply to deflect calls, but to meet customers inside their digital journeys. By the end of 2024, it was handling more than 100,000 conversations every month in the UAE, supported by more than 80 automated service journeys now available in-app. The bank is rapidly evolving the service beyond query handling towards what it describes as “agentless fulfilment”, where virtual agents can complete transactions end-to-end without human intervention.

The goal of the virtual assistant is not just to answer basic questions but to understand intent in real time, converse in natural dialogue and resolve issues before they become problems

Fernando Morillo, group head of retail banking, Mashreq

This anticipatory model reduces escalation by embedding support within the flow of transactions rather than after the fact. Customer support is no longer reactive troubleshooting but a proactive, AI-enabled system that reduces friction, boosts satisfaction and allows staff to focus on more complex needs.

Jordan-based Arab Bank adds another dimension by using generative AI to support staff rather than replace them. Launched in July 2024, its frontliners assistant tool consolidates multiple internal sources into a single conversational interface. Instead of navigating five separate systems for products, credit policies, compliance rules, forms and process manuals, customer service staff can query the assistant in English or Arabic – including a mix of both languages or dialectal Arabic – and receive concise, verified answers with source references.

Early results were promising: the initial phase covered 400 employees and saved around 700 staff hours per month, with wider rollout under way throughout 2025. The assistant also mitigates human error by ensuring that all required steps and documents are captured before a customer query is answered.

Beyond efficiency, the initiative marks a shift in how Arab Bank approaches customer service – from static process adherence to continuous knowledge enablement. By giving staff real-time, AI-assisted access to accurate information, the bank helps frontliners respond faster, more confidently and more consistently, strengthening service quality and customer trust.

Elsewhere, ABK uses carefully placed physical touchpoints plus AI to nudge customers deeper into digital. Its flagship digital branch features touch-free interactive screens and a first-of-its-kind hologram, with tablets for account opening and digital signature services in collaboration with the Public Authority for Civil Information, alongside advanced interactive teller machines that connect customers to remote agents for real-time help. Complementing this, ABK’s ‘digital island’ smart self-service points in high-footfall malls offer 24/7 kiosks for cash and account services, interactive guidance screens and tight linkage back to digital channels.

On the support layer, ABK blends automation with human assistance. An AI-powered virtual customer-service representative allows customers to complete selected transactions remotely in around 30 seconds and escalate to live video assistance when needed. In parallel, ABK reports further AI-enabled advancements such as fraud-detection algorithms and AI-assisted credit decisions – with outcomes including a 35% increase in customer engagement and a 25% reduction in fraudulent activity.

In essence, ABK’s CX model is a phygital on-ramp plus AI-assisted service: immersive spaces and smart kiosks to teach and transact; and remote, time-compressed fulfilment to resolve issues with minimal effort.

Taken together, these examples show how customer support in the Middle East has become an always-on layer of the banking relationship, blending AI-driven anticipation, staff-empowering knowledge systems and phygital touchpoints.

Trust by design: Embedding security in CX

As digital adoption deepens, customers want to see clear safeguards around their money. Security has become part of the experience itself – and the region’s leading banks are embedding trust into design in visibly distinct ways.

For recent entrants such as Wio Bank, the imperative is to build confidence from day one. Wio has implemented device binding with facial recognition and a cooling-off period before transacting with newly added beneficiaries. By making these protections explicit, Wio turns them into part of the value proposition, signalling that safety is integral to the brand. Behind the scenes, this is reinforced by an identity and risk stack that includes Onfido and Emirates facial recognition for verification and Feedzai, Ingenuous, LSEG Risk Intelligence, Moody’s and Archer for fraud and compliance, strengthening prevention without sacrificing simplicity.

If Wio built trust from the outset, NBB illustrates how trust is sustained through disciplined, purpose-driven execution. In response to a spike in social-engineering fraud across Bahrain in 2023, NBB overhauled its digital security model around customer protection. It introduced device binding, multi-factor authentication and an in-app soft token, all embedded directly within its mobile platform rather than using external authenticators. The bank also implemented app shielding to block rooted or compromised devices and accepted short-term business impacts to prioritise customer safety. The results were striking: fraud cases on NBB’s digital channels fell from approximately BHD80,000 per month to zero, and the Central Bank of Bahrain recognised the model as a national benchmark.

Emirates NBD, facing some of the region’s highest digital transaction volumes and a diverse customer base, has tailored its fraud controls to specific behavioural risks. Within its ENBD X app, adding a new beneficiary now triggers two warnings, including a check on whether the customer is being prompted by someone claiming to represent a government agency or police, and shows partial name confirmation from official databases. Transfers attempted during an active call – a common scam pattern – are blocked outright, and payments to newly added beneficiaries are allowed only after a two-hour cooling-off period. In addition, customers can raise disputes and replace compromised cards instantly through the app. Together, these measures helped cut fraud cases and total fraud volume on ENBD X tenfold between Q4 2023 and Q4 2024, demonstrating how smart, visible controls can protect users without adding friction.

The broader picture is that security in the Middle East has shifted from back-office infrastructure to a front-line component of customer experience. Controls are designed to be visible, understandable and reassuring. The best practice emerging from the region is to integrate protection directly into journeys, align it with real-world risks and communicate it in ways that build confidence.

Towards a holistic CX model

The Middle East’s digital leaders are converging on a model where CX spans the entire customer lifecycle: frictionless onboarding; empathetic support; and trust by design. Fully digital account opening has transformed compliance into convenience. Support has evolved from reactive to proactive, often AI-augmented and seamlessly omnichannel; and security has become a visible part of reassurance rather than an invisible back-office function.

With young digital-native populations, progressive regulators and robust government identity systems, the region is well placed to pioneer new standards in CX. The challenge ahead will be scaling human-AI collaboration, balancing speed with security and extending CX excellence into third-party ecosystems.

Financial health that empowers

Beyond convenience: How digital banking is building financial confidence

The most sophisticated digital banks in the Middle East are moving beyond convenience. Once defined by speed, design and efficiency, digital leadership is now also measured by its impact on financial well-being – helping people to plan, learn and participate more fully in the financial system. From the Gulf’s largest incumbents to its youngest challengers, the focus has shifted toward building healthier financial habits and widening access to the benefits of banking.

Everyday prosperity and wellness

Among the region’s digital pioneers, Wio Bank has built its model around empowering customers to take control of their finances in simple, measurable ways. The Wio Personal app combines everyday spending, saving and investing within a single interface that encourages consistent, goal-based behaviour. Its savings spaces allow users to create sub-accounts for specific goals, automate transfers, track progress visually and monitor interest earnings – a design that promotes disciplined saving and greater financial awareness.

For customers ready to move beyond saving, the Wio Invest function within the app opens a convenient pathway to wealth creation. With a single tap, users can purchase low-commission global and UAE stocks, fractional shares, exchange-traded funds, cryptocurrencies and local IPOs, and even choose to receive cashback as stock investments – turning consumption into capital formation. Wio has combined its diversified retail investment offering with features to simplify and enrich the experience, including analyst ratings, stock lending to earn passive income and recurring orders to boost systematic savings. Together, these features translate financial awareness into tangible action, showing that financial well-being can be aspirational and accessible.

A similar philosophy guides NBK, which has sought to make digital retail banking a source of guidance rather than complexity. The bank’s mobile app – responsible for nearly two-thirds of all retail transactions in 2024 – uses data analytics, geolocation and predictive modelling to make customer interactions more relevant and transparent. By tailoring offers and information to each user’s circumstances, NBK aims to simplify decision-making and build confidence in how customers manage their finances.

That same emphasis on clarity extends to its savings products. The Al Jawhara account, its flagship prize-linked savings product, has been re-engineered for digital life. Customers can open and manage accounts instantly, monitor draw eligibility based on their savings deposits and receive full visibility over the process. Meanwhile, the Al Jawhara Junior introduces saving to children through simple goals and rewards. Together, these tools promote responsible saving and show how digital design can make financial discipline more accessible across generations.

Confidence through clarity

SAB has adopted a structured approach to financial well-being through the 2024 launch of SAB 360°, its personal-finance-management platform. The tool gives customers a complete view of their income, expenses and financial goals, using tailored budgets and predictive insights to help them plan ahead. Weekly and monthly reports summarise spending patterns and forecast income and outgoings for the coming month, while notifications keep customers on track with category budgets and overall targets.

What distinguishes SAB 360° is its educational layer. Within the app, customers can access a dedicated section of short articles and tips on topics such as budgeting, saving and debt management – embedding financial literacy directly into everyday banking. Adoption has been striking: more than 518,000 customers were active on the platform by end-2024, underscoring strong demand for contextual guidance rather than static dashboards.

SAB has complemented this focus on education with empathetic design choices that recognise moments of financial strain. Its personal finance deferral option, available entirely online, allows customers to reschedule one loan instalment per year without penalty – a simple but powerful feature that acknowledges the realities of fluctuating household cash flow. By combining education with flexibility, SAB is providing retail customers with the confidence to plan, adapt and take control of their finances.

Empowerment from an early age

For a growing number of Middle Eastern banks, digital empowerment begins with the youngest customers. As Kuwait’s first fully digital bank, Weyay has captured more than a third of the youth market by treating money management as a skill to be learned, not merely a service to be used.

Its Saving Pots and Saving Pots Pro features allow users to set visual goals, automate contributions and earn returns of up to 1%, transforming the process of saving into an interactive journey. Progress bars and notifications create instant feedback loops, rewarding consistency and reinforcing discipline. For younger customers still learning the basics, Jeel – a first-to-market app for children aged eight to 14 – combines education, security and sustainability. Parents oversee spending through real-time alerts and adjustable limits, while the app uses gamified experiences to teach children about saving, budgeting and spending responsibly. By turning banking into a series of teachable moments, Weyay is cultivating informed financial behaviour from childhood to adulthood.

NBB has embraced a similar philosophy in its youth proposition, applying the principles of literacy, independence and oversight through its Yalla Family Account. Integrated within the NBB Digital Banking app, it enables parents to open and manage accounts for their children, set daily and monthly allowances, and monitor transactions in real time. Young users have their own dashboard to view balances and spending, helping them develop sound saving and budgeting habits in a safe, engaging environment.

The Yalla proposition is an example of how we are meeting the needs of all segments of society. Our approach is to use digital means to encourage financial literacy and provide youth with exposure to banking products and some independence, while allowing for parental oversight

Usman Ahmed, group CEO, National Bank of Bahrain

That balance – between autonomy and guidance – reflects a broader mindset across NBB’s retail strategy – that empowerment begins with understanding customers’ needs.

Financial literacy as a bridge to inclusion

In Oman, Bank Muscat has used its market-leading scale to address a different challenge: how to extend financial literacy to the unbanked and under-served. As part of its corporate social responsibility strategy, the bank launched Maliyat, an innovative online platform designed to enhance financial awareness across all age groups. Available in Arabic and English, the bilingual platform offers interactive lessons and practical budgeting tools that teach participants how to set savings goals, manage debt and plan for emergencies – essential skills often absent from formal education systems.

Since its launch, more than 23,700 participants have benefitted from Maliyat’s content, which can be accessed via smartphone, tablet or computer. The same principles of simplicity and accessibility guide the bank’s digital channels. Within the Bank Muscat mobile and internet banking platforms, customers can open minor accounts linked to a guardian and access more than 100 digital services including payments, savings and investments.

Faith-based inclusion through digital design

In the UAE, ADIB has taken a faith-based approach to financial inclusion that blends digital innovation with ethical education. Its moneysmart platform, available online and within the ADIB mobile app, delivers bilingual tutorials and interactive content that teach customers about Shariah-compliant finance, responsible consumption and financial planning.

ADIB has complemented these literacy efforts with digital tools that broaden inclusion more widely, including the Money Management Tracker – developed with Emirati fintech Lune – which helps customers categorise spending, automate budgets and set savings goals. The bank has also lowered barriers to Islamic investment through its fractional sukuk feature, allowing retail investors to participate from as little as $1,000. In this way, ADIB is combining faith-based principles with digital design to make financial empowerment more inclusive and accessible.

From literacy to leadership

The Middle East’s digital retail banking agenda now places a greater emphasis on purpose and participation. Across markets, banks are reimagining their role from service provider to educator, designing digital ecosystems that teach users to budget, save, invest and plan.

Financial health has become the cornerstone of this evolution. Personal finance tools, behavioural nudges and micro-education features are making it easier for individuals to understand and manage their money. At the same time, empowerment is expanding through inclusive design: youth banking ecosystems; bilingual literacy programmes; and simplified digital onboarding are opening formal finance to everyone.

Collectively, these developments signal a broader transformation in the region’s retail banking landscape. Banks are now competing on how effectively they can translate technology into knowledge – empowering every customer, regardless of age or income, to enhance their financial well-being.

Looking ahead: From digital delivery to intelligent ecosystems

Middle Eastern retail banking has crossed a threshold. The past decade’s transformation roadmaps have delivered: digital adoption is now near-universal, customer experience has become the main battleground for loyalty, and a new generation of platforms is reshaping how people manage, spend and grow their money. The question is no longer who has gone digital, but who is using digital maturity to build smarter, more inclusive and anticipatory banking models.

This year’s MarketMap reveals that execution is now the true differentiator. The region’s leaders have moved beyond proof-of-concept innovation to deliver measurable impact – apps that have become ecosystems, automation that has become intelligence, and customers who are more engaged, secure and financially confident than ever before.

The next frontier: Intelligent, anticipatory banking

The next phase will be defined by intelligence. AI and open finance are expanding the boundaries of what digital banking can see, predict and deliver. Banks are beginning to anticipate intent, compress decision-making and personalise services at the level of the individual.

Generative AI will likely soon link data, dialogue and delivery across every function – from product design to compliance. Open finance will extend visibility beyond the bank, linking with insurance, investments and everyday utilities to make financial management more predictive and holistic. In this environment, competitive advantage will hinge on foresight: the ability to meet needs before customers articulate them.

Defining the next decade of digital leadership

Key competitive differentiators for the cycle ahead:

- Execution with intelligence: Strategy must now be measured by adoption, engagement and outcomes.

- Ecosystem orchestration: The winners will embed their services into the fabric of everyday digital life.

- CX as trust: Empathy, security and personalisation will converge into one unified experience.

- Empowerment through inclusion: Banks will be judged by how effectively they extend confidence, literacy and access through digital means.

- AI as capability: Success will depend not on automating judgement but on augmenting it.

Middle Eastern retail banking is now defined not by access to technology but by access to intelligence. The next generation of leaders will turn data into foresight, ecosystems into advantage and inclusion into growth.