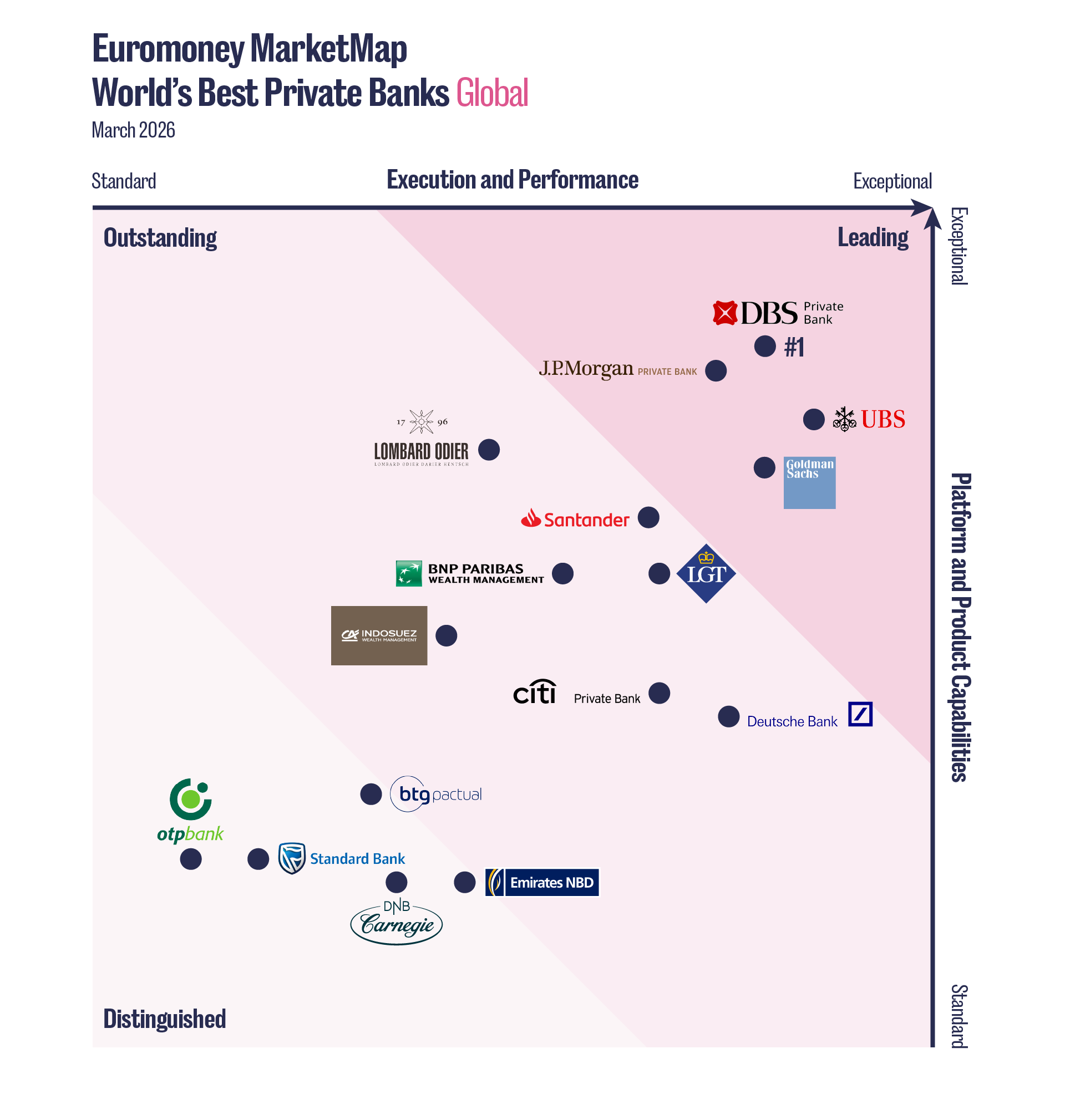

The world’s leading private banks enter 2025 riding record asset growth, but the gap between those that have invested in technology, alternatives and talent, and those that have not is widening. Euromoney’s inaugural MarketMap for The World’s Best Private Banks assesses institutions across two axes of competitive performance – execution and platform – to reveal who is best positioned to capture wallet share as clients consolidate relationships, alternatives go mainstream and AI reshapes the front office.

In the 12 months to 1H25, the world’s leading private banks saw their assets under management (AUM) hit new highs, supported by a favourable alignment of macroeconomic and market dynamics. Falling interest rates reduced the appeal of holding excess cash, prompting private banking clients to redeploy liquidity built up during the prior tightening cycle. This shift was reinforced by a powerful artificial intelligence (AI)-driven rally in US equities, lifting overall portfolio performance.

At the same time, private markets became firmly entrenched as a core allocation for ultra-high-net-worth (UHNW) and high-net-worth (HNW) clients. Private banks expanded their alternatives platforms across private equity, private credit and infrastructure, positioning these assets as tools for long-term growth and income generation in a lower-rate environment.

However, this supportive backdrop did not benefit all players evenly. Private banks that had invested in modern technology platforms, broadened their alternatives offering and strengthened advisory coverage in high-growth regions such as Asia, the Gulf and Latin America captured a disproportionate share of net new assets (NNA). Those that delayed such investments saw competitive gaps widen, even as markets rose.

It is this edge that the Euromoney World’s Best Private Banks MarketMap seeks to highlight – showing how leading institutions are balancing product depth, technology, client service and talent to win wallet share among the world’s wealthiest families.

The world’s best private banks in 2025 were those that built an integrated operating model in which products, digital capabilities, client segmentation and talent density reinforce one another. In a world in which UHNWs and HNWs are increasingly looking to consolidate – rather than expand – their number of wealth management relationships, no single axis of competence is enough to consistently capture client flows.

Singapore’s DBS Private Bank, the leader in this inaugural MarketMap, demonstrates that a focused Asian platform with genuine product innovation and execution discipline can outperform global incumbents on both axes of our assessment. The MarketMap report plots the competitive landscape and examines the themes that define world-class private banking today.

More reports

The MarketMap and methodology

Methodology

The Euromoney MarketMap is a proprietary analytical framework designed to assess and position the world’s leading private banks against two thematic axes of competitive performance. The MarketMap combines four evidence sources to produce a composite positioning for each private bank. All are drawn from submissions made by institutions in the Euromoney Private Banking Awards 2026 research cycle, supplemented by publicly disclosed financial data.

- Quantitative data: encompassing AUM, NNA, revenue, cost-to-income ratios, return on assets and relationship manager productivity metrics.

- Qualitative data: detailing strategic initiatives, client capabilities, product innovation and investment in people and technology.

- Structured interviews: conducted by the Euromoney research team with senior executives including chief executive officers, heads of private banking, chief investment officers and heads of key product and regional business lines.

- Proprietary Euromoney analysis: Scores, evidence and peer comparisons compiled by Euromoney analysts during the Private Banking Awards 2026 research cycle.

Each institution is scored against criteria organised against two axes.

- Execution and performance (x-axis): evaluates execution of stated market strategy, AUM growth, NNA generation and wallet-share gains, revenue and margin performance, relationship manager productivity and recruitment, and M&A integration track record.

- Platform and product capabilities (y-axis): assesses depth and innovation of private banks’ product shelves – including trading and execution, funds, alternatives and discretionary management – digital platforms, commitment to sustainability and environmental, social and governance (ESG) integration, and client segmentation.

Based on composite scores across both axes, institutions are placed into one of three tiers. The Leading tier comprises banks that are exceptional on both axes — delivering superior growth, product depth and execution simultaneously. The Outstanding tier recognises institutions that excel across most criteria with notable strengths, but may have some differentiation gaps. The Distinguished tier identifies credible performers with strong specialisms or compelling growth stories in specific segments or markets.

Strategy and execution excellence

In global private banking, success is not just about the size of an individual institution’s AUM but also the rate at which it is growing via NNA – and, critically, the quality of these client flows and their generation of ROA.

The Leading tier institutions distinguish themselves not merely by generating large NNA numbers in absolute terms but by sustaining that momentum across multiple markets and client segments while maintaining or improving revenue margins.

DBS Private Bank earns the top spot in the MarketMap by virtue of a strategy that has converted Singapore’s structural advantages as a wealth hub into a genuinely differentiated private banking platform. The bank’s record AUM growth during the review period was built on a wealth continuum model that graduates clients from DBS Treasures into the private banking tier, creating a pipeline of domestically sourced HNW relationships that supplements its cross-border business.

In a region where most competitors rely heavily on poaching relationship managers and their client books, DBS has built an organic growth engine. Its UHNW and family office servicing, discretionary portfolio management (DPM) and chief investment office (CIO) are among the best in Asia-Pacific. Meanwhile, the firm’s digital infrastructure – a legacy of DBS’s broader transformation into one of the world’s most digitally advanced banks – provides an execution platform that few rivals match. Its geographic expansion – particularly into the Middle East, India and UK – give the bank tremendous optionality to tap new sources of wealth creation beyond its traditional strongholds of Southeast Asia and Greater China.

We’ve outperformed our global peers … on growth, on returns, on client flows, on stability of operations and on innovation. We doubled our AUM in five years and achieved record-breaking income, consistently outpacing global competitors in growth and execution

Joseph Poon, group head of DBS Private Bank

JPMorgan Private Bank delivered impressive performance metrics in terms of asset gathering and top line. The bank’s $239 billion in NNA during 2024, on a base of $1.16 trillion in total AUM and $2.9 trillion in global client assets, represents a growth rate that few institutions of comparable scale can match. The firm added thousands of net new clients during the year, with revenues also rising strongly. The appointment of bank veteran David Frame to unify the US and international private banking divisions under a single leadership structure was a strategic decision that has already yielded results – with strong AUM growth in Asia, EMEA and Latin America. The opening of a Munich office in 2024 and the expansion of its Dubai team signalled the firm’s willingness to invest in physical presence when relevant opportunities present themselves.

UBS Global Wealth Management faced a unique execution challenge in 2025: the ongoing integration of one-time rival Credit Suisse while simultaneously delivering growth on the bank’s key performance metrics. By most measures, the firm’s performance was remarkable. Global invested assets reached $6.1 trillion as of 1H25, with NNA of $54.8 billion in the first half of 2025 alone. Revenue for the Global Wealth Management division reached $12.4 billion in 1H25. But crucially, the bank’s cost-to-income ratio improved to 75.8 % from 79.7% in 2024, with more than half of the bank’s $13 billion in targeted cost savings achieved. The bank’s CET1 ratio of 14.3% demonstrated that growth was not coming at the expense of capital discipline. The integration of Credit Suisse’s client books – a process that risked destroying significant value if not handled delicately – has instead expanded UBS’s addressable market across Switzerland, Asia and the Americas.

Goldman Sachs Private Wealth Management has focused relentlessly on the UHNW segment, where its institutional-grade investment platform creates a moat that many smaller and pure-play peers cannot match. The firm commands sizeable wallet share in the $1 billion-plus client segment globally, reflecting the sophistication of its service and platform across alternatives investments, co-investments and bespoke structuring. The alternatives business, a more than $1 trillion in AUM business at group level, feeds directly into wealth management, giving UHNW clients exposure to strategies that are unavailable elsewhere.

In the Outstanding and Distinguished tiers of our MarketMap, two private banks deserve acknowledgement for strategy and execution excellence. Santander Private Banking has built a strong HNW platform at scale across Iberia and Latin America, leveraging the group’s balance sheet and local market knowledge. BTG Pactual has emerged as one of the notable growth stories in global private banking, with AUM rising 36% year-on-year to $194.6 billion as of 1H25, underscoring its transformation from a Brazil specialist into a pan-Latin America player.

Client segmentation focus

Leading institutions in the private banking space are moving beyond simple AUM-based tiering when it comes to building genuinely differentiated service models for the HNW, UHNW, family office and next-generation client segments. Those in the Leading tier of our MarketMap recognise that each segment demands fundamentally different capabilities, not merely different service levels.

JPMorgan’s 23 Wall initiative is one of the most ambitious family office strategies in global private banking. Named after the historic address of the House of Morgan, the programme now serves hundreds of families controlling trillions of dollars in aggregate private capital. The launch of the Global Family Office Practice in 2025, alongside the firm’s 40×40 Conference – bringing together the next generation of family office principals – signals an intent to institutionalise these relationships across generational transitions. The bank’s commanding position in the ultra-wealth segment is the product of decades of investment in people, products and platform. The next-gen programmes have been designed not as marketing exercises but as genuine relationship-building platforms that create loyalty before the wealth transfer occurs.

In the eyes of Goldman Sachs, its target UHNW client looks and behaves more like an institutional investor than a retail one. As such, the bank’s family office solutions emphasise co-investment access, direct deal flow and bespoke structuring at a level of complexity that requires genuine institutional infrastructure. The Ayco platform, originally designed for corporate executives, has become a gateway to the firm’s broader wealth management capabilities, capturing clients at the point of significant liquidity events and transitioning them into the private banking relationship. The selectivity of the model – Goldman does not compete for market share in the HNW space – is a strategic choice that allows the firm to maintain the depth of coverage and investment access that its target segment demands.

We have a leading investment bank, global markets, asset management and wealth management franchise. And when you bring all those things together for clients, it’s a very powerful offering

John Mallory, global co-head of wealth management, Goldman Sachs

UBS has formalised its client segmentation through the Wealth Way framework, which structures client portfolios and advisory conversations around three pillars: liquidity; longevity; and legacy. This is more than a marketing construct – it has become an organising principle for the firm’s product development, adviser training and client engagement globally. The bank’s Family Advisory and Philanthropy Services division addresses the non-financial dimensions of multi-generational wealth, an area where some competitors default to third-party referrals rather than building in-house capability. The firm’s $1.1 billion raised for social impact bonds in 2024 demonstrates the integration of values-based investing into the core client proposition. UBS’s next-gen programmes, operating across the Americas, Europe and Asia, aim to build relationships with the heirs to its existing client base – a critical defensive strategy given that many next-gen clients review their family private banking relationship during a wealth transfer event.

Under the leadership of Claudio de Sanctis — Euromoney’s Private Banker of the Year 2026 — outstanding Deutsche Bank Private Bank has rebuilt its UHNW and family office capabilities with a particular focus on its internationally mobile client base. The One Bank model, which integrates private banking with the firm’s investment banking and corporate capabilities, gives Deutsche a distinctive proposition for entrepreneurial families whose needs span personal wealth management, corporate finance and capital markets. The holistic family office coverage model that De Sanctis has championed treats each family as an institution, deploying multi-disciplinary teams that combine investment expertise, lending, trust and estate planning, and philanthropic advisory.

Nobody else can go to a client and say: ‘Let’s talk about your company and your private affairs as one continuum.’ We just have one conversation

Claudio de Sanctis, head of Deutsche Bank Private Bank

Citi Private Bank has built one of the industry’s most coherent client‑segmentation models for globally mobile UHNW families, anchored by its Global Client Service framework. Designed for clients with assets, residences and business interests spanning multiple jurisdictions, the model enables cross‑border onboarding, harmonised advice and coordinated execution across regions. Teams of relationship managers collaborate as a single global unit, addressing issues global clients often face, such as regulatory fragmentation. This is reinforced by a breadth of specialist advisory capabilities spanning governance, philanthropy, art, aircraft and sports finance. A multi‑generational coverage model and targeted next‑gen programmes further strengthen continuity, positioning Citi as a strong choice for UHNW families with complex global requirements.

Lombard Odier and LGT, also in the Outstanding tier, both leverage the advantages of their pure-play positioning to serve the UHNW and family office segments with a degree of alignment and long-termism that universal banks often find difficult to replicate. Lombard Odier’s strength in next-gen and succession planning reflects its deep roots in Genevan private banking, where multi-generational relationships are time-tested over centuries. LGT’s ownership by the Princely House of Liechtenstein gives it a unique credibility with family offices: it is, in effect, one itself. The alignment of interests that this creates resonates strongly with UHNW clients who value discretion, stability and a genuinely long-term investment horizon. The firm’s owner-managed ethos and growing presence in Asia have made it a serious competitor for relationships that might otherwise default to larger global banks.

In the Distinguished tier, the newly combined entity of DNB Carnegie has successfully targeted entrepreneurs, family offices and other UHNW clients across Sweden, Denmark and Norway by leveraging Carnegie’s equity and capital‑markets heritage alongside DNB’s balance sheet and international reach. A focus has been extending the reach of institutional capabilities, such as Nordic equity research and private markets, across client tiers via digital channels.

Attracting and retaining key talent

The private banking talent market in 2025 was characterised by intense competition for a shallow pool of senior relationship managers with the right combination of UHNW networks, product knowledge – particularly in more complex private markets investments – and multi-jurisdictional experience. The rapid growth of wealth in Asia, the Gulf and Latin America created demand for experienced coverage capacity in markets where the local talent pipeline remains immature. Banks that had invested in structured hiring programmes and internal development pathways found themselves better positioned than those relying solely on lateral recruitment.

JPMorgan Private Bank made significant leadership hires across Asia-Pacific, including the expansion of its Singapore and Australia teams, and the appointment of David Frame to oversee a unified private banking division that spans the US and international operations. The firm’s structured programmes for next-gen talent – including its private banking analyst programme and rotational schemes – are designed to build a pipeline of relationship managers from within, reducing dependence on external hires. The scale of the platform, and the breadth of career paths available within the JPMorgan ecosystem, gives the firm a retention advantage that smaller competitors cannot easily replicate.

UBS Global Wealth Management faced the most complex talent-management challenge in the industry: integrating key relationship manager talent from Credit Suisse while rationalising overlapping coverage and retaining high performers. The bank’s ability to execute this integration without catastrophic attrition – while simultaneously making key hires in Asia-Pacific and the Middle East – is a standout of its post-acquisition performance. The firm has invested in cultural integration programmes and revised compensation structures designed to align incentives across the legacy UBS and Credit Suisse populations.

DBS Private Bank has pursued a distinctive approach to talent, building out coverage capacity in Singapore and Hong Kong through a combination of targeted external hires and internal development via its wealth continuum model. The continuum – which allows relationship managers to progress from the Treasures mass-affluent segment into private banking – creates career paths that incentivise retention and build deep local market knowledge that externally recruited bankers may lack.

In the Outstanding tier, Santander has assembled specialist HNW coverage teams across Iberia, Latin America and its international markets, leveraging the group’s brand and local presence as a hiring advantage.

Among the Distinguished banks in our MarketMap, Standard Bank’s talent strategy in Africa is built on local hiring and development across sub-Saharan markets, recognising that the cultural and linguistic diversity of the continent demands relationship managers with depth of local knowledge.

Product and solutions strength

The quality and breadth of an investment product shelf have become arguably the most important factor when it comes to capturing wallet share in the UHNW space. Clients in this segment – often those with $100 million in investable assets – expect access to the same strategies that are available to the world’s largest institutional investors, such as private equity, private credit, infrastructure and co-investments. The private banks that can deliver this access at scale, with appropriate due diligence and structuring, have an advantage that no amount of client service or digital innovation can offset.

JPMorgan Private Bank’s alternatives platform is the largest in the industry, with $200 billion in AUM and dozens of new funds launched in 2025 alone. The firm is targeting tens of billions of dollars in fundraising for its evergreen structures, which are designed to provide UHNW and HNW clients with access to private markets without the lock-up periods and capital-call structures of traditional institutional funds. The Morgan Private Capital co-investment programme gives the firm’s largest clients direct access to deal flow alongside JPMorgan’s own balance sheet – a proposition that few competitors can replicate. The firm’s sports investment franchise, which has facilitated billions of dollars in transactions, including the $6.1 billion Boston Celtics sale, has become a highly visible dimension of its UHNW offering.

We did an end-to-end lifecycle journey … now processing four times as much with the same-sized middle office – and the experience is as easy as buying on Amazon

Kristin Kallergis Rowland, global head of alternative investments, JPMorgan

UBS Global Wealth Management’s product strength is anchored by a CIO function that oversees trillions of dollars in assets and produces the UBS House View, one of the most widely followed investment strategy publications in wealth management. The firm’s structured products and separately managed account leadership reflects the scale of its distribution network, while My Way – its digital DPM service – has reached billions of dollars in AUM. The breadth of the platform means that UBS can offer clients a full spectrum of solutions from standardised model portfolios to fully bespoke mandates, with pricing and service levels calibrated to each segment.

Goldman Sachs Private Wealth Management leverages its institutional alternatives franchise – one of the largest in global asset management – as a differentiator for its private banking clients. The firm’s co-investment access and ability to originate proprietary deal flow for UHNW families creates a product moat that generalist private banks cannot breach. The Marquee digital platform, originally built for institutional clients, has been adapted to provide wealth management clients with analytics and execution capabilities that blur the line between institutional and private banking. Goldman’s strategy is hinged on the idea that, at the UHNW level, access to institutional quality alternative products defines the client relationship.

In the Outstanding tier, BNP Paribas Wealth Management has established itself as a leader in structured products and fund advisory, with a recommended funds track record that delivered nearly all positive returns in the 12 months to 1H25 across a range of strategies spanning disruptive technology, Asia long-short equities and global bonds. A sharp rise in fund advisory AUM reflects the credibility of the investment team and the breadth of the bank’s European distribution network.

Indosuez Wealth Management has materially strengthened its European DPM proposition after the integration of Degroof Petercam and a concerted effort to unify its investment platform. The combination has led to an almost doubling of discretionary penetration within overall client assets, reflecting the successful migration of acquired portfolios and strong commercial momentum across core European markets. One notable launch was of the Compass mandate, providing a cost‑efficient entry point into discretionary mandates through exchange-traded fund (ETF)‑ and index‑based strategies. Meanwhile, structured products and private markets mandates have expanded portfolio flexibility and access to alternative assets.

Deutsche Bank Private Bank’s success in the Euromoney award for Europe’s Best Private Bank CIO Office reflects an integrated investment strategy platform that links the private bank with the firm’s investment banking and research capabilities. Deutsche’s ability to structure bespoke products for its largest clients – drawing on the corporate and investment bank’s derivatives and structuring expertise – is a competitive advantage that pure-play private banks generally cannot match.

Meanwhile, LGT has built a pure-play alternative investment platform that emphasises impact investing and private markets access, leveraging the Liechtenstein royal family’s own investment experience as a credibility signal.

Lombard Odier’s DPM heritage is one of the longest in the industry, and its CLIC investing framework – structured around Circular, Lean, Inclusive and Clean investment principles – integrates sustainability into portfolio construction in a way that goes beyond standard ESG screening. The firm’s technology edge in portfolio construction, delivered through Lombard Odier Technology Services, gives its investment managers analytical tools that are comparable to those of far larger institutions.

In the Distinguished tier, BTG Pactual operates one of the most integrated alternatives platforms for private wealth clients in Latin America, combining origination, distribution and in‑house management across asset classes, including private equity, private credit, hedge funds and real assets. Institutional-grade due diligence, a proprietary feeder fund structure and partnerships with leading global managers differentiate the offering from peers in the market.

Staying on the cutting-edge of digital

For most of private banking’s recent history, digital investment has been primarily defensive – focused on compliance automation, risk monitoring and back-office efficiency. However, this is fast changing, with 2025 being characterised by the increasing deployment of generative AI into the front office, transforming the tools available to relationship managers, the speed and quality of client onboarding, and the personalisation of advisory. The banks that have led this transformation have been those that have invested in the platforms, infrastructure and governance frameworks necessary to deploy large language models (LLM) at scale.

JPMorgan Private Bank has more than 500 AI use cases in production across its private banking operations, ranging from its LLM Suite – which provides relationship managers with natural language access to client data and investment research – to Connect Coach, an AI-powered training tool for advisers. The bank’s mobile-first JPOI platform achieved a more than doubling in year-on-year increase in active mobile users, reflecting a client base that expects digital-first engagement even from an UHNW-focused bank. The incorporation of AI into client onboarding processes has substantially reduced errors, delivering compliance benefits and an improved client experience during the critical early stages of the relationship.

UBS Global Wealth Management has executed one of the largest AI deployments in global financial services. The firm’s 50,000 Microsoft Copilot licences – spanning wealth management, investment banking and corporate functions – have given its advisers generative AI tools for client communication, research synthesis and portfolio commentary. The internal AI assistant Red is now available to 30,000 employees and is used for tasks ranging from regulatory research to meeting preparation. The Smart Technologies and Advanced Analytics Team (STAAT) platform, which has facilitated more than 15 million AI-generated interactions, delivers personalised investment insights to advisers based on each client’s portfolio characteristics, risk profile and market conditions. UBS My Way, the firm’s digital discretionary service, represents the integration of technology into the investment management process itself, offering clients a digitally managed portfolio with the depth and rigour of UBS’s CIO function at a lower minimum than traditional DPM mandates.

We want to use AI clearly to further augment the relationship. Our bankers will become much better, more effective, more efficient, more accurate. We will have a lot more client time going forward

Benjamin Cavalli, head of strategic clients, UBS

DBS Private Bank brings to private banking the technology DNA of one of the world’s most digitally advanced consumer banks. The firm’s app-based advisory tools, AI integration in the CIO process and digital wealth infrastructure have earned it recognition as the best private bank for digital solutions. Its seamless digital experience across the wealth continuum – from Treasures through to private bank – creates a client journey that is technology-enabled at every stage, from prospecting and onboarding to portfolio monitoring and reporting.

OTP Private Banking is an instructive case study in digital innovation in Europe’s emerging markets. The firm’s OTP SingleMarket platform provides access to more than 1,000 instruments in a unified interface, while its robo-adviser launch achieved a 10% conversion rate – reflecting both the quality of the digital proposition and the unmet demand for digital private banking tools in Central and Eastern Europe (CEE). The wealth management platform automates advisory workflows, and a dedicated trust management IT solution has been deployed to support the more complex end of the client base.

Deutsche Bank Private Bank has invested in front-to-back digital integration, with digital client reporting and AI-assisted portfolio monitoring improving adviser efficiency and client transparency. Emirates NBD has developed digital private banking tools tailored to the Middle Eastern market, with app-based wealth management capabilities that reflect the region’s high smartphone penetration and appetite for digital-first financial services.

Based on this evidence, the most effective private banks are not using AI to replace the relationship manager but to make the adviser more productive, better informed and more responsive.

Meanwhile, digital assets remain an emerging product for clients, with most private banks adopting a cautious approach to cryptocurrency custody and trading, but investing in the infrastructure to scale if client demand accelerates. The technology leaders in private banking are those that have built platforms capable of supporting the efficiency gains of automation and the personalisation demands of UHNW clients.

Crypto holdings with us have exceeded gold holdings – a clear signal of client trust and future readiness

Joseph Poon, group head of DBS Private Bank

Leading on the sustainable investing frontier

Sustainability and impact investing in private banking entered a period of recalibration in 2025. The ESG backlash in the US – driven by political and regulatory pressure on the use of ESG criteria in investment decision-making – created a divergence in client demand that private banks were forced to navigate with care.

The most successful institutions are those that have moved beyond the binary debate over the merits of ESG investing, and instead built the analytical frameworks to integrate sustainability considerations into portfolio construction as one dimension among many.

BNP Paribas Wealth Management – winner of the Euromoney Award for Best Private Bank for Sustainability 2026 – has built one of the most comprehensive and client-centred sustainable investing frameworks in the global private banking industry. The bank’s ESG-by-Design approach has resulted in 94% of its recommended investment universe meeting Article 8 or Article 9 classification under the EU’s Sustainable Finance Disclosure Regulation (SFDR) – well above the European market average of 52%. This spans more than 20 Article 9 thematic funds covering climate transition, water security, forests, health and social inclusion. Recently, BNP Paribas introduced a solidarity mandate in which 85% of the portfolio is allocated to sustainable investments and 15% to solidarity funds, with management fees channelled to projects in the public interest.

LGT’s commitment to sustainability is structural rather than cosmetic, embedded in the investment process through its blended finance platform and reinforced by the personal commitment of its owner, the Princely House of Liechtenstein. The firm’s approach – integrating impact criteria alongside financial return targets rather than treating them as a constraint – has become a model for the industry.

Lombard Odier’s CLIC investing framework – structured around Circular, Lean, Inclusive and Clean investment principles – represents one of the most intellectually rigorous approaches to sustainable investing in the private banking industry. The firm has embedded sustainability ratings into its portfolio construction process, ensuring that ESG considerations are not a separate overlay but an integral part of the investment decision. Its pure-play independence allows it to take positions on sustainability that might be difficult for a universal bank with significant fossil-fuel lending exposure, and its recognition as Euromoney Best Pure-play/Boutique in Europe reflects the credibility of this approach.

UBS has deployed its scale to advance sustainable investing through product development and capital mobilisation. The firm raised $1.1 billion in social impact bonds in 2024, and sustainable investing is embedded as a pillar of the Wealth Way framework that underpins its advisory conversations. The appointment of a chief sustainability officer within Global Wealth Management signals the strategic importance that UBS attaches to this agenda, while its net-zero commitment provides a framework for portfolio-level decarbonisation advice.

OTP Private Banking has embedded ESG into its advisory model across its nine CEE markets, offering ESG-compliant model portfolios that reflect both EU regulatory requirements and emerging client demand in a region where sustainable investing awareness is growing rapidly. Standard Bank’s sustainability narrative is anchored in the African context – green finance and impact investing take on a distinctive character when the continent faces simultaneous challenges of economic development, climate adaptation and energy transition. The firm’s approach to sustainable wealth management in Africa is necessarily different from the European model, and its ability to navigate that complexity is a competitive advantage.

The world’s best private banks

DBS Private Bank

DBS Private Bank earns the highest overall placement in the inaugural Euromoney MarketMap for The World’s Best Private Banks, a distinction that reflects the institution’s exceptional performance across both the execution and performance, and strategy and product capabilities axes. The bank’s record AUM growth during the review period was propelled by Singapore’s consolidation as Asia’s premier wealth management hub, a structural tailwind that DBS has exploited more effectively than any competitor by virtue of its domestic market position, regulatory relationships and deep integration with the city-state’s entrepreneurial and family office ecosystem.

The wealth continuum model – which creates a seamless graduation pathway from DBS Treasures to DBS Private Bank – generates organic AUM growth and builds client loyalty from an early stage. The bank’s UHNW capabilities have matured significantly, with DPM and CIO functions recognised as best-in-class in the Asia-Pacific region. Digital integration is a hallmark of the DBS approach, drawing on the broader institution’s reputation as one of the world’s most technologically advanced banks. The firm’s regional expansion across Indonesia, Hong Kong and India positions it to capture the diversification of Asian wealth creation beyond its Singaporean home base. In a MarketMap that rewards the combination of execution discipline and strategic depth, DBS’s achievement in delivering both simultaneously places it at the apex.

JPMorgan Private Bank

JPMorgan Private Bank is the private banking industry’s most formidable growth engine, and its placement in the Leading tier of the MarketMap reflects a combination of scale, execution and strategic ambition that is unmatched in the global peer set. The bank’s $1.16 trillion in AUM and $2.9 trillion in global client assets make it one of the largest private banks in the world by any measure, but the 2024 performance – $239 billion in NNA, thousands of net new clients, and revenue of $11.4 billion – demonstrates that the firm continues to grow at a rate that belies its size.

The 23 Wall initiative, serving approximately 800 families with $5 trillion in aggregate private capital, positions JPMorgan at the centre of the global family office ecosystem. The unification of US and international operations under David Frame has created a coherent global platform where regional growth – Apac AUM up 43%, EMEA AUM up 25%, Latin American wealth at $220 billion – is coordinated rather than siloed. The alternatives platform, at $200 billion in AUM with 68 new funds in 2025, gives the firm product depth at a scale that few competitors can approach. Combined with $18 billion in annual technology investment and more than 500 AI use cases in production, JPMorgan has built a private banking franchise that competes on every dimension simultaneously.

UBS

UBS is the world’s largest private bank by invested assets, with $6.1 trillion under management following the transformational acquisition of Credit Suisse. Its placement in the Leading tier of the MarketMap reflects not merely the scale of the balance sheet but the quality of the integration execution and the ambition of the firm’s technology and product strategy. NNA of $54.8 billion in the first half of 2025, following $42.4 billion in 2024, demonstrate that the integration has not disrupted the firm’s growth trajectory. Revenue of $12.4 billion in the first half of 2025, a cost-to-income ratio improving to 75.8% and a CET1 ratio of 14.3% speak to an institution that is delivering growth, efficiency and capital discipline simultaneously.

The technology transformation is among the most ambitious in the industry: 50,000 Microsoft Copilot licences, an internal AI assistant available to 30,000 staff, and more than 15 million AI-generated interactions through the STAAT platform. The CIO function oversees $4 trillion in assets and produces the UBS House View, while the My Way digital discretionary service – at $15 billion in AUM – demonstrates the integration of technology into the investment process. UBS has expanded its geographic footprint into Australia, the Bahamas, Spain and the Middle East, and client satisfaction scores of 88% “very or extremely satisfied” – up three percentage points year-on-year – suggest that the firm is managing the complexity of integration without sacrificing the client experience. The challenge ahead is to complete the cost-savings programme and convert operational scale into sustained margin expansion.

Goldman Sachs

Goldman Sachs occupies a distinctive position in the MarketMap: it is the only Leading-tier institution whose strategy is built explicitly around depth rather than breadth. The firm’s commanding market share in the $1 billion-plus wealth segment reflects a deliberate focus on the UHNW client for whom Goldman’s institutional-grade investment platform, alternatives access and bespoke structuring capabilities are not merely attractive but essential. The alternatives business, which operates at significant scale globally, provides UHNW clients with co-investment opportunities and proprietary deal flow that are simply not available through generalist private banks.

The Ayco platform for corporate executives creates a natural pipeline of clients at points of significant liquidity events – IPOs, corporate transactions, executive compensation realisations – and transitions them into the full wealth management relationship. The family office solutions capability offers governance advisory, investment structuring and succession planning at a level of sophistication that reflects Goldman’s heritage as a firm built to serve the world’s most demanding financial counterparties. The model is deliberately selective, prioritising relationship depth and product sophistication over client volume. In a market where many competitors are pursuing scale through technology and segmentation, Goldman’s refusal to dilute its UHNW focus is itself a strategic differentiator.

LGT

LGT is the world’s largest pure-play private banking group, and its ownership by the Princely House of Liechtenstein gives it a unique positioning in the industry. The alignment of interests between owner and client – both are families managing multi-generational wealth – creates a credibility that universal banks cannot replicate. LGT’s alternatives and impact investing credentials are among the strongest in private banking, and its DPM has been recognised for consistent quality. The firm’s growing presence in Asia reflects the appeal of its owner-managed ethos to UHNW families in the region who value stability, discretion and a genuinely long-term investment perspective. Named Euromoney Best Pure-play/Boutique globally 2026, LGT is a compelling example of how focus and alignment can compete with scale.

Santander Private Banking

Santander Private Banking has built a credible HNW franchise at scale, leveraging the Santander Group’s balance-sheet strength, local market knowledge and distribution reach across Iberia and Latin America. The bank’s core markets in Spain and the major Latin American economies give it a natural advantage in serving the HNW segment, where group-level capabilities – lending, trade finance, corporate banking – complement the private banking advisory offering. Strong NNA in core markets and developing family office capabilities reflect the institution’s progress in moving upmarket, while the internationalisation of the franchise extends its reach to globally mobile clients within its natural catchment area.

BNP Paribas Wealth Management

BNP Paribas Wealth Management brings European scale, structured products leadership and a fund advisory track record that has delivered nearly all positive returns across its recommended funds in 2025. The fund advisory AUM rose sharply between 2022 and the first nine months of 2025, reflecting the strength and credibility of the investment team. The firm’s cross-border wealth solutions for European UHNW clients benefit from the depth of the BNP Paribas group’s institutional capabilities, while expansion in Asia and the Middle East broadens the addressable market. BNP Paribas’s distinction as winner of the Euromoney Award for Best Private Bank for Sustainability 2026 further cements the franchise’s position as one of the most complete wealth management platforms in Europe, combining commercial performance with leadership on the sustainable investing agenda.

Citi Private Bank

Citi Private Bank occupies a unique competitive position as the only private bank operating with genuine banking capabilities in more than 160 countries. This global infrastructure – the ability to provide lending, cash management, custody and foreign exchange alongside investment advisory in virtually every jurisdiction – is a powerful differentiator for ultra-wealthy, globally mobile families whose financial lives span multiple countries and currencies. The bank was named Euromoney Best for Client Service globally and in North America at the Private Banking Awards 2026, reflecting the quality of the advisory experience that sits on top of this institutional platform. The UHNW and family office capabilities are built around Citi’s institutional-grade infrastructure, creating a proposition that seamlessly links private and institutional banking.

Deutsche Bank Private Bank

Deutsche Bank Private Bank has undergone a strategic transformation under Claudio de Sanctis, named Euromoney Private Banker of the Year 2026. One major strength is the bank’s CIO, providing an integrated investment strategy platform that draws on the firm’s research, structuring and execution capabilities across the investment bank. The One Bank model – which connects the private bank to Deutsche’s corporate and investment banking divisions – gives the institution a distinctive proposition for entrepreneurial families and family offices with complex, multi-dimensional needs.

Lombard Odier

Lombard Odier is the quintessential Geneva pure-play: independent, owner-managed and built on a DPM heritage that stretches back more than two centuries. The firm’s CLIC investing framework – Circular, Lean, Inclusive, Clean – is among the most intellectually rigorous sustainable investment methodologies in the industry, and its integration into portfolio construction goes well beyond standard ESG screening. Lombard Odier Technology Services provides the firm with a proprietary technology edge in portfolio analytics and client reporting. The institution’s strengths in next-gen and succession planning, combined with its open-architecture investment approach, place it among the most popular choices for European families seeking an independent, long-term advisory partner with genuine sustainability credentials.

Indosuez Wealth Management

Indosuez Wealth Management, part of the Crédit Agricole group, offers a global product shelf with genuine breadth in structured products and fund advisory. Strong capabilities in Western European and cross-border wealth management are anchored by operations in Switzerland and Luxembourg, with the full Crédit Agricole balance sheet providing lending and product depth behind the private banking offer. DPM excellence and the ability to draw on the resources of one of Europe’s largest banking groups make Indosuez a credible competitor for internationally mobile European UHNW families.

BTG Pactual

BTG Pactual is Latin America’s largest private bank and scored highly on our MarketMap in terms of NNA growth. The firm’s alternatives and DPM leadership in Latin America, combined with family office capabilities and multiple Euromoney award wins across the region, position it as a dominant private banking franchise in a market that remains one of the world’s largest and fastest-growing pools of private wealth.

Standard Bank

Standard Bank is Africa’s largest private banking franchise, serving the full spectrum of HNW and UHNW clients across sub-Saharan Africa. The institution’s cross-border capabilities serve African UHNW clients with offshore needs – a critical requirement in a region where international diversification is both a financial and a political imperative. As the only private bank to combine depth of coverage across South Africa, East Africa and West Africa at scale, Standard Bank stands as a regional champion.

Emirates NBD Private Banking

Emirates NBD Private Banking has benefitted from Dubai’s continued ascent as a global wealth hub, with AUM growth driven by the migration of HNW and UHNW individuals into private banking structures in the Gulf. The institution’s Islamic wealth management capabilities are a significant differentiator in a region where Shariah-compliant investment solutions are not a niche but a mainstream requirement. Digital innovation in the Gulf Cooperation Council (GCC) context, combined with broad coverage across the UAE and the wider GCC states, positions the bank as the region’s leading private banking franchise.

DNB Carnegie Private Banking

DNB Carnegie Private Banking is Norway’s leading private bank for UHNW clients. Dedicated multi-disciplinary UHNW teams provide holistic advisory across investment management, lending, tax and estate planning. The firm’s Zurich representative office and Luxembourg platform serve cross-border Nordic families, while the integration of investment banking capabilities provides clients with corporate finance and capital markets access. The recent launch of a robo-adviser demonstrates a commitment to digital innovation that complements the firm’s traditional advisory strengths.

OTP Private Banking

OTP Private Banking was named Euromoney’s Best Private Bank in CEE for 2026. The firm manages approximately €11 billion in AUM across nine CEE countries, serving more than 32,000 clients. The CETOP ETF – which achieved 36-times net asset value (NAV) growth from launch – exemplifies the innovation capacity of the platform, while the OTP SingleMarket digital platform provides access to more than 1,000 instruments. A nearly one-third market share in Hungary anchors the franchise, and the regional standardisation strategy is creating a scalable operating model across a fragmented market. Digital innovation, including the robo-adviser and automated advisory workflows, positions OTP as the dominant and most forward-looking private banking platform in the region.

Looking ahead

The inaugural Euromoney MarketMap for the World’s Best Private Banks captures a competitive landscape at a point of inflection. The convergence of three structural forces – the deployment of AI at scale, the democratisation of alternatives access through evergreen fund structures and the onset of the largest intergenerational wealth transfer in history – will reshape competitive dynamics over the next three to five years. To stay ahead of the pack, private banks will need to act on the following imperatives:

Win wallet share through client consolidation: As HNW and UHNW clients reduce the number of private banking relationships they maintain, institutions with the deepest product breadth, most credible CIO function and most trusted advisory relationships will capture a disproportionate share of consolidating assets. Primary bank status will become the defining battleground.

Deepen alternatives and product leadership: Access to institutional-grade private equity, private credit, infrastructure and co-investment – via scalable evergreen structures – is no longer a differentiator for the largest banks; it is a baseline expectation. Mid-tier institutions that cannot close the alternatives gap risk ceding the UHNW and upper-HNW segments to peers with superior product depth.

Accelerate AI and technology investment: Generative AI is moving from pilot to production across the front office. Banks that embed AI into relationship manager workflows, client onboarding, CIO commentary and portfolio monitoring will extract meaningful productivity gains – and banks that do not will face widening cost and service-quality gaps against leaders such as JPMorgan and UBS.

Embed sustainability as a commercial imperative: As European regulatory requirements intensify and client demand for impact investing grows – particularly among next-generation wealth holders – banks with credible, integrated ESG frameworks will be better positioned to retain assets through generational transfers.

Build local execution capacity in high-growth markets: Asia, the Gulf and Latin America are producing new wealth at a rate that demands on-the-ground coverage rather than offshore servicing. Institutions that invest in physical presence, local hiring and regional product customisation in these markets will capture flows that global platforms served from London or New York cannot reach.

Build digital asset infrastructure ahead of demand: Cryptocurrency holdings are becoming a mainstream component of UHNW portfolios in leading markets. Private banks that develop regulated custody, trading and advisory infrastructure for digital assets now will be positioned to capture this allocation – and the trust that comes with it – as institutional adoption accelerates.