Trade finance has always been a collective endeavour, but rarely has that been more evident than in 2025. In a year marked by geopolitical uncertainty, increased protectionism, regulatory change and rapid technological acceleration, the industry did not retreat into silos. Instead, banks, corporates, multilaterals and policymakers leaned into collaboration, recognising that resilience in global trade depends as much on shared standards and education as it does on balance sheets.

One of the clearest shifts we observed this year was how banks increasingly positioned themselves not just as providers of liquidity but as partners for their clients. Corporates consistently told us that guidance and transparency mattered as much as product availability. That focus on education – helping clients understand risk, digital tools and evolving regulations – has become a defining feature of leading trade finance franchises.

Equally important is the pace of innovation. What stood out in 2025 was not experimentation for its own sake but how fast ideas moved from pilot to production. More than vague concepts, digital documentation, automation and sustainability-linked structures are now operational realities shaping daily trade flows.

Perhaps most encouraging is the industry’s expanding lens. Trade finance is no longer discussed solely in the context of large multinationals. Banks are increasingly focused on extending access to mid-sized corporates and small and medium-sized enterprises (SMEs), recognising that inclusive trade is essential to sustainable growth.

Euromoney’s Trade Finance Survey provides a unique window into these dynamics. With insights from 12,694 corporate respondents across 96 markets and feedback on 435 banks, it captures how trade finance is evolving where it matters most: in real transactions, real relationships and real economies.

Core risks faced by corporates in 2025

Trade finance in 2025 operated against an increasingly complex risk backdrop. Geopolitical tensions, expanding sanctions regimes and prolonged high interest rates all weighed on cross-border activity. Yet, trade finance proved resilient, underpinned by its core risk-mitigating characteristics: short tenors; self-liquidating structures; and strong documentary controls. During periods of instability, corporates leaned more heavily on traditional instruments such as confirmed letters of credit (LC), guarantees and credit insurance to secure payments and manage counterparty exposure. Increasing usage of these instruments is seen in the lower corporate segments.

According to Vivek Ramachandran, head of Global Trade Solutions at HSBC, “2025 was a year which was unprecedented in the scale of change.”

To understand how corporates perceive risk today, respondents were asked to identify the top three risks affecting their trade finance activities in 2025. This analysis is based on responses from 9,861 corporates globally.

FX volatility and cybersecurity dominate

Foreign exchange volatility emerged as the most significant risk globally, followed closely by cybersecurity. Persistent currency fluctuations, diverging interest-rate paths and uneven monetary policy normalisation kept FX risk firmly at the top of corporate risk agendas. For companies with cross-border exposure, the challenge extended beyond cost predictability to meeting internal risk governance thresholds.

While banks continue to offer a broad range of hedging tools, corporates increasingly point to execution challenges. The integration of FX solutions into trade workflows remains uneven, with timing mismatches, pricing opacity and fragmented platforms continuing to undermine confidence and effectiveness.

Cybersecurity ranked second globally, reflecting heightened awareness of fraud and operational risk. Trade finance has historically been vulnerable to document-based fraud, including duplicate invoice financing and falsified warehouse receipts. In 2025, the threat landscape evolved further, with evidence that generative artificial intelligence (AI) tools are being used to forge trade documents and manipulate data. In response, banks are accelerating investment in cybersecurity measures, document verification technologies, distributed ledgers and advanced data analytics to detect anomalies and reduce reliance on manual processes.

Geopolitics and trade policy fragmentation

Geopolitical risk remains a defining feature of the trade environment. Among large global corporates, nearly half identified geopolitical tensions as a top-three risk, with the impact particularly pronounced among European-based firms.

“Companies have been incredibly proactive about thinking about levers they can pull,” HSBC’s Ramachandran explains. “Consistent feedback from the market is that companies are rethinking business models and their supply chains.”

Trade policy uncertainty compounds these challenges. The continued proliferation of sanctions and unilateral trade measures has forced banks to expand screening, due diligence and monitoring capabilities, often supported by AI-driven compliance tools. While efforts to reform and strengthen the multilateral trading system could restore confidence in rules-based trade, policy uncertainty remains a material concern for corporates planning their long-term supply chains.

Regulatory change remains a material concern

Regulatory developments also feature prominently among corporate risk perceptions. Basel III final reforms, scheduled for implementation between 2025 and 2027, are an area of focus for the industry. Trade finance stakeholders continued to engage with regulators to ensure that capital rules appropriately reflect the low-risk nature of short-term, self-liquidating instruments. By 2025, several jurisdictions had delayed implementation timelines and early signals suggested a broadly supportive approach. In the EU, for example, the Capital Requirements Regulation III (CRR3) framework included adjustments recognising certain supply chain finance exposures.

Accounting standards represented another structural shift. For some corporates, additional public disclosure of supply chain finance programmes under updated International Financial Reporting Standards (IFRS) and US General Accepted Accounting Principles (GAAP) guidance represented a challenge. While increased transparency did not dampen demand for payables finance, it prompted greater discipline in programme design and documentation, improving clarity around risk allocation and balance-sheet treatment.

A highly regionalised risk profile

Protectionism and tariffs emerged as highly regionalised risks. In the US, 58% of respondents identified tariffs as a top-three risk, making it the most frequently cited concern among US-based corporates. In China, FX volatility was cited by 68% of respondents, followed by protectionism and tariffs at 60%.

Despite the fact EU and US have the largest bilateral trade and investment relationship, tariffs’ concerns ranked much lower in Europe – only 27% of respondents across the 27 EU countries identified them as a top-three risk, placing the risk sixth overall. For European corporates, geopolitical risk, cybersecurity and regulatory change dominated as core risks.

“Following the war in Ukraine and instability in the Middle East, many corporates slowed activity in early 2025 while assessing tariff and geopolitical developments,” explains Francesca Nenci, global head of trade and corresponding banking, UniCredit. “Since Q3-2025 we have seen a partial recovery of trade activity intensity.”

Environmental and climate-related events did not feature prominently among corporates’ top risks in 2025, despite growing regulatory and public attention.

Overall, the risk and regulatory environment in 2025 presented a mixed picture. Heightened geopolitical, fraud and compliance risks reinforced demand for traditional trade finance risk mitigants, while also accelerating innovation in monitoring and digital controls. At the same time, regulatory developments broadly progressed in a supportive direction, with digital trade laws, capital treatment and disclosure standards moving toward greater clarity and transparency.

“We are seeing a rediscovery of trade instruments as risk-mitigation tools with broad-based applications that extend beyond international trade,” adds Guillermo Aymard, global head of trade and working capital, global transaction banking at TD Securities. “One of the most valuable tools we can provide clients right now is optionality, through availability of products, expertise, networks, and partnerships spanning vanilla risk undertakings to more tactical liquidity solutions and structured financing.”

Top ranked trade finance providers

Global and regional

Global trade regained momentum in 2025, providing a supportive and increasingly complex backdrop for trade finance. World merchandise and services trade reached record levels, exceeding $35 trillion, with growth driven primarily by volumes.

East Asia led the expansion, with export growth of around 9% and a sharp rise in intra-regional trade, while major emerging economies including China, India, South Korea and Brazil remained central to global flows. Despite geopolitical tensions, shifting tariff regimes and higher trade costs in some corridors, underlying demand proved resilient.

This resurgence reinforced the role of trade finance as both an enabler of growth and a mitigant of risk. As policy uncertainty persisted, corporates renewed their reliance on structured instruments such as LC to safeguard trade relationships, manage counterparty exposure and maintain compliance. In volatile conditions, trade finance once again demonstrated its value in stabilising cross-border transactions and supporting supply chain resilience.

At the same time, regional dynamics diverged. Asia-Pacific continued to dominate global trade activity and innovation; Central and Eastern Europe (CEE) relied heavily on multilateral risk-sharing; Latin America benefitted from a commodities-led rebound; the Middle East saw strong trade growth underpinned by diversification and Islamic finance; North America focused on working-capital optimisation and digital integration; and Western Europe advanced legal frameworks for electronic trade and sustainability-linked finance. Together, these dynamics shaped a year of recovery and transformation for global trade finance.

Against this backdrop, corporates assessed global providers on how effectively they delivered consistency and their support in navigating continuous uncertainty.

Ranked by corporates as #1 trade finance provider globally, HSBC is valued less for the sheer breadth of its footprint and more for what that breadth enables in practice: operational consistency across markets. Corporate respondents consistently see HSBC’s global presence as a way to reduce complexity rather than add to it. A sector-based approach has become central to how HSBC supports its clients. “We reorganised the trade global team, focused on industry groups,” Vivek Ramachandran, head of global trade solutions at HSBC explains. As trade becomes a board-level lever, he adds, “beyond working capital, CEOs and CFOs are looking at trade as a sales enablement tool, as a risk mitigation tool and as a supply chain resilience tool.”

For globally active corporates, managing trade finance across jurisdictions often means juggling multiple interfaces, escalation paths and documentation practices. HSBC’s perceived strength lies in limiting those internal workarounds, allowing teams to focus on control, visibility and execution rather than exception management. From Ramachandran’s perspective, the value of HSBC Trade Solutions (HTS) platform is structural. A single global instance allows HSBC to support trade activity consistently across markets, now live in 25 countries. “HTS is fully integrated from the client channel all the way through to fulfilment, with one version of data flowing through,” he explains. “Clients are looking for full digital journeys, linked to their systems and embedded in their processes.”

This operational framing comes through in feedback tied to execution quality and digital throughput. A manufacturing corporate operating domestically in Sri Lanka highlights “excellent digital trade finance services, quick processing times and reliable document handling”. A global industrial corporate based in Malaysia echoes this, pointing to HSBC’s “intuitive and secure” online banking, but pairing that with praise for “knowledgeable and responsive” trade staff suggesting that digital capability is most valued when it shortens turnaround time and simplifies issue resolution.

The same theme appears in feedback from larger, cross-border users. A wholesale trade corporate with regional operations in Hong Kong notes that HSBC “supports trade flows efficiently across markets and responds quickly when issues arise”, reinforcing the idea that consistency in execution is as important as product availability.

As a leading global trade finance provider, Deutsche Bank is positioned by corporates as a structural partner for complex cross-border trade. Across regions, clients consistently highlight balance-sheet strength, risk expertise and execution discipline rather than product breadth.

In Asia-Pacific, a wholesale trade client in China points to Deutsche’s ability to support domestic and international transactions seamlessly, while a Vietnam-based corporate highlights reliable execution in high-volume environments. In Western Europe, Deutsche is often chosen by HQs as the mandate winner across the region, reflecting its integration within multinational banking structures and its strength in navigating risk, compliance and sanctions. In the US, clients emphasise “industry knowledge, global scope and professional team”, alongside its digital tools. Balance-sheet capacity anchors these relationships, with many respondents using Deutsche as their primary provider, referencing deeper relationships than trade finance.

For Crédit Agricole, corporates consistently rank its trade finance around service quality, advisory depth and relationship continuity across regions. In CEE, clients in Poland highlight execution and flexibility, while clients in jurisdictions such as Ukraine appreciate their advisory capabilities, especially when handling complex transactions. In Western Europe, Crédit Agricole is associated with structured execution and tailored support. Clients across France, Italy and Germany reference strengths in core trade products, but also complex cross-border transactions.

At a global level, Standard Chartered is positioned by corporates as an international connector, particularly across Asia, Africa and the Middle East. In Asia-Pacific, clients highlight the bank’s credibility and network reach. Execution and digital access reinforce this role, with senior treasurers across the world pointing out their portal and service. Alongside execution strength, Standard Chartered has pushed innovation into sustainability-linked trade. In August 2025, the bank executed the world’s first sustainable trade finance bank guarantee aligned with the ICC’s sustainability principles, a $300-plus-million syndicated structure for Envision Energy, independently validated against green standards.

In Iberia and Latin America, BBVA and Santander are positioned by corporates as specialists with strong global reach. BBVA’s trade finance proposition reflects the realities of operating in fragmented and volatile markets, with a focus on receivables finance, supply chain finance and factoring to support extended payment terms and fluctuating demand. Clients highlight execution quality, accessibility and digital capability. Santander has continued to scale its Trade and Working Capital Solutions franchise across Latin America and Western Europe, combining local execution with structured solutions. Its integrated approach across receivables, payables and inventory finance, including hybrid models such as Invensa, supports liquidity optimisation and supply chain resilience for corporates operating across regional and global supply chains.

BNP Paribas and Societe Generale, European champions with a strong global trade finance footprint, combine scale with depth of capability. BNP Paribas is consistently associated with product breadth and platform strength. Across Asia-Pacific and Western Europe, clients reference reliability, access to credit and efficient processing, with bank guarantees, credit management and factoring cited as core strengths. Platform quality is a recurring theme, with corporates pointing to strong digital self-service and responsive execution in high-volume environments. Societe Generale’s differentiation is also technology-led. The application of AI to document verification, fraud detection and control across trade workflows improves accuracy and insights. This is reinforced by structured implementation support and a transaction banking framework that embeds sustainability, helping corporates classify and benchmark ESG-linked trade activity as disclosure expectations continue to rise.

At Citi, trade finance innovation is centred on digitising historically paper-heavy processes and scaling impact. The launch of Citi Digital Bill replaced paper bills of exchange with an end-to-end electronic workflow, cutting receivables discounting from days to under an hour in live markets, including the US and UK. Alongside this, Citi is piloting smart contracts and tokenised cash to enable self-executing trade settlements. At scale, its supply chain finance platform supports thousands of buyers and extensive supplier networks, with dynamic discounting and sustainability-linked terms increasingly embedded to drive faster liquidity and measurable ESG outcomes.

Asia-Pacific reinforced its position as the engine of global trade in 2025. East Asia recorded the strongest export growth globally, while China remained the world’s largest trade finance market by volume. Intra-Asian trade across Asean, China and India sustained high utilisation as manufacturers expanded production for both Western markets and regional supply chains. Japan and South Korea also saw a recovery in export financing activity, supported by stronger shipments of electronics and machinery.

The region remained at the forefront of digital trade. Financial centres such as Singapore and Hong Kong continue to be digital trade hubs, supported by gradual legal alignment with electronic transferable records and government-backed interoperability initiatives. India accelerated participation in digital documentary workflows through bank-led initiatives, while China expanded domestic digital infrastructure and encouraged greater use of renminbi settlement. A broader regional push to diversify invoicing currencies reflected both risk-management considerations and a desire to reduce exposure to sanctions-related frictions.

Client feedback positions HSBC as #1 trade finance provider in Asia-Pacific, with strong feedback on service responsiveness and operational resilience. Treasury teams describe an environment in which growth ambitions must be balanced against control, and HSBC is assessed on its ability to deliver consistently at scale. For Vivek Ramachandran, HSBC’s head of global trade solutions, the balance between platform strength and people is a defining differentiator. “We’ve demonstrated through our external hires that we are a magnet for talent. The ability to attract and hire the best people in the industry where we need to bolster capabilities is unique,” he says.

A wholesale trade corporate operating domestically in Indonesia highlights HSBC’s “advanced digital channel” for trade finance, alongside strong relationship support that “provide best service to us”. Service quality is frequently linked to issue resolution. A Malaysian corporate notes “timely issue resolution” and a trade services team that “resolves issues on trade facilities in a timely way”. Capacity also matters. A regional trading company based in Singapore adds that HSBC “handles high trade volumes without disruption”, reinforcing the importance of platform stability and processing resilience in the region.

In Asia-Pacific, Deutsche Bank, a leading provider, distinguishes its trade finance proposition through balance-sheet strength, risk expertise and its ability to support complex domestic and cross-border flows. The bank’s role as a global intermediary features strongly in client feedback. A wholesale trade client in China highlights Deutsche’s ability to support domestic and international transactions seamlessly.

Operational robustness reinforces this positioning. An accountant in Vietnam’s transportation sector notes that reliable execution in high-volume environments is what differentiates Deutsche. In India, corporates reference strength in corporate coverage and the ability to manage documentation and confirmations across borders.

DBS’s trade finance proposition in Asia-Pacific is defined by speed and product breadth. A finance manager in Singapore’s utilities sector highlights pricing alongside efficiency, while a financial controller in Hong Kong points to DBS’s role in “simplifying the process”. A wholesale trade client in Singapore notes processing time as a differentiator factor, while another observes that “DBS bank is always fast in its services”.

Product breadth also features prominently. A finance director in Taiwan’s technology sector highlights “different products” including accounts receivable trade finance, while a finance manager in Vietnam’s manufacturing sector references “wider variety of products”.

MUFG’s trade finance proposition in Asia-Pacific is built around support for cross-border flows, particularly across Southeast Asia and North Asia. Clients in Indonesia and Hong Kong consistently highlight commercial terms and service quality. A finance manager in Indonesia’s manufacturing sector describes MUFG’s “best offering and service quality”. Relationship depth reinforces this positioning. A finance manager in Indonesia’s equipment sector highlights “products [and] helpful follow-up”, while a senior financial manager in Hong Kong emphasises customer service. Another client points to “corporate loyalty”, underlining the importance of long-standing relationships.

Standard Chartered’s trade finance strength in Asia-Pacific is shaped by its regional network and its role in connecting Asia with Africa and the Middle East. Clients frequently reference the bank’s credibility as an international partner. A regional finance manager in China’s information technology sector notes that Standard Chartered sits “within the group’s whitelist of partner banks”, highlighting the importance of network trust.

Digital access and execution quality reinforce this position. A head of treasury in India highlights the bank’s “portal and service”, underlining the value of consistent digital access across markets.

OCBC’s trade finance proposition in Asia-Pacific is shaped by a pragmatic approach to regional trade flows. Clients across Singapore, Indonesia and Malaysia consistently cite commercial terms. For larger mandates, credit support remains central. A global finance manager highlights “credit line availability” alongside “processing and support”.

Operational efficiency and reach further strengthen the proposition. A regional financial controller in Malaysia highlights OCBC’s ability to “remit to most of the region”. Relationship depth also appears in feedback. A global head of treasury in the agriculture sector notes that “OCBC Bank stands out in trade finance with efficiency”.

BNP Paribas’s trade finance proposition in Asia-Pacific is shaped by reliability, credit availability and pricing discipline. Clients in India highlight the importance of digital capability and efficient processing. Credit terms and conditions remain critical as well. A head of treasury in India highlights the “availability of credit limits” and LC when managing volatile trade flows.

UOB’s trade finance proposition in Asia-Pacific is defined by regional connectivity and efficient execution. A regional financial controller highlights UOB’s ability to support cross-border activity in key corridors of interest for its organisation. Others emphasise speed and support. A finance manager in Southeast Asia highlights “processing and support”, while a regional head of treasury points to “efficiency”.

Asia-Pacific continues to face geopolitical complexity, particularly in sensitive cross-border corridors. Banks have responded with enhanced risk frameworks and greater digital tracking, to support corporates to navigate the international uncertainty. At the same time, regional integration and industry-led standards continue to reduce friction.

The message from corporates is consistent. In Asia-Pacific, trade finance providers succeed not by innovation alone but by combining competitive pricing, resilient execution at scale and compliance-led control that does not compromise speed or reliability.

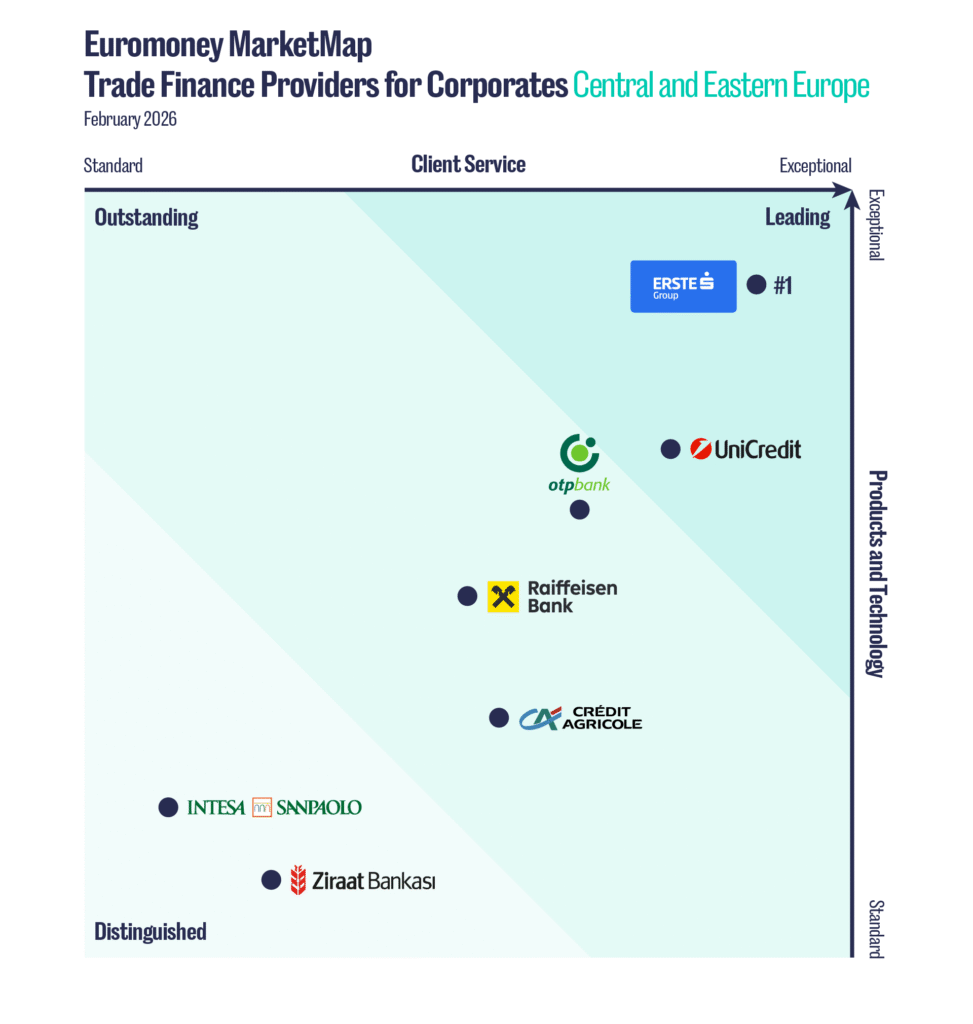

CEE’s trade finance environment in 2025 was shaped by geopolitics and re-routing and less so by cyclical factors. The ongoing war in Ukraine and the broader reconfiguration of European supply chains continues to redefine trade flows across the region.

Countries such as Poland, Romania and the Baltics benefitted from nearshoring, with increased trade volumes linked to EU integration and Asian sourcing. Poland, for example, saw stronger exports into the EU alongside rising imports from Asia as legacy routes closed. By contrast, other countries closer to the conflict zone faced more acute operational constraints, including disrupted logistics corridors, elevated insurance costs and heightened counterparty risk, particularly around Black Sea routes.

Against this backdrop, trade finance in the region remained fundamentally about continuity. Multilateral and development institutions played a critical stabilising role, with the European Bank for Reconstruction and Development (EBRD) expanding its Trade Facilitation Programme (TFP) to provide guarantees supporting LC and trade loans across CEE and Central Asia. These structures allowed local banks to continue financing essential imports and exports that would otherwise have fallen outside risk appetite.

Within this environment, corporate feedback consistently points to the importance of responsiveness, clarity and local decision-making. For many corporates, trade finance relationships in 2025 were tested not by volume alone but by how quickly banks could act, adapt structures and provide certainty.

At Erste Group, long-standing relationships and flexibility stood out as defining characteristics. Corporates across Croatia and Serbia repeatedly emphasised speed of execution and supportive structuring. An accountant in Croatia’s construction sector highlights execution pace, while a finance manager in the consumer discretionary sector points to the “quality of the service”, underlining the importance of reliability in a volatile operating environment. Flexibility also features prominently. A regional finance manager in Croatia’s information technology sector describes Erste Group as “extremely supportive” when structuring transactions. Relationship continuity reinforces this position. A finance manager in Croatia’s manufacturing sector observes, “we have been working with them the longest”, while a managing director in Serbia’s transportation sector highlights predictability, noting that “the results of potential requests are always known”.

For UniCredit, the strength of its CEE franchise lies in local presence combined with regional consistency. “Our model is very clear: we have product at global level, ensuring the same quality and same service level to all our customers,” explains Francesca Nenci, global head of trade and corresponding banking, UniCredit. “People on ground, in the countries, are with clients every day. Then we have a strong back office.”

Clients across Hungary, Romania and Poland point to accessibility and communication as critical factors when managing trade activity. Nenci attributes this to a strong transformation programme: “UniCredit structured its trade finance transformation around three pillars: a digital client interface, internal automation, and process simplification across countries.”

A head of treasury in Hungary’s construction sector highlights communication as decisive. Execution speed and service quality are recurring themes. A chief executive officer in the industrials sector identifies service as the core reason for working with the bank, while others reference UniCredit’s ability to support domestic and cross-border trade through a consistent regional platform. “We deliberately separated high-value advisory from operational processing, building a dedicated trade finance hub in Romania to improve efficiency,” Nenci adds. “We have a very skilled team which we built over the last 10 years.” The message is clear: proximity and responsiveness remain central in fragmented markets.

At OTP Group, corporate feedback highlights local proximity, execution speed and operational focus. Clients across Serbia, Croatia, Hungary and neighbouring markets consistently reference accessibility. An accountant in Serbia’s manufacturing sector points to “proximity to branches and speed”, underlining the value of local decision-making. Execution quality is reinforced by client focus. A finance director in Serbia’s communications sector notes OTP’s ability to “meet client needs”, while a managing director in agriculture summarises the experience as “efficiency [and] speed”. For more complex requirements, stability matters. A finance manager in Hungary’s manufacturing sector highlights “risk sharing and stability”, alongside a broader product set, reflecting the bank’s role in supporting structured trade flows across the region.

At Raiffeisen Bank International, speed of execution and direct access to decision-makers emerge as defining strengths. Clients across Serbia, Bosnia and Herzegovina, Croatia, Romania and Ukraine consistently highlight responsiveness. A finance director in Bosnia and Herzegovina’s retail sector summarises the value proposition as “speed”, while a senior financial manager in Serbia’s wholesale trade sector points to the rapid issuance of guarantees. Relationship access also matters. A senior accountant in Serbia highlights the importance of “contact with managers”, reflecting the premium placed on real-time decision-making in time-sensitive transactions. RBI’s role as a core provider further reinforces its position. A head of treasury in Croatia’s industrials sector describes the bank as the “main provider” for domestic and international trade, while corporates in Romania and food and beverage point to the bank’s willingness to deploy credit and support large construction-related trade flows. Digital capability is increasingly visible, with references to digital guarantee applications and solution-oriented execution.

For Crédit Agricole, trade finance in CEE is defined by service quality, advisory depth and relationship continuity. Clients in Poland consistently highlight execution and flexibility. A chief financial officer in manufacturing describes the experience simply as “service”, while a finance manager in construction points to a “flexible approach” to trade financing. Scope and accessibility also feature, with corporates referencing broader financing support and the bank’s role in issuing guarantees for domestic and cross-border activity. In more complex markets, advisory capability is decisive. A client in Ukraine highlights Crédit Agricole’s “international connections” and ability to deliver “non-standard solutions”. Platform quality reinforces this positioning. A chief financial officer in Poland’s construction sector highlights “top-notch software, efficient processing and quality service”, while another notes faster information processing than peers. Relationship depth remains central. A global chief financial officer in Poland’s industrials sector highlights “people, their knowledge, competence and commitment”, while another concludes: “For us, Crédit Agricole is not just a bank, but a long-term partner.”

Across the region, structural challenges persisted. Currency volatility in non-euro markets and tight monetary conditions constrained trade activity for some corporates, while the war in Ukraine continued to distort insurance availability and risk appetite. Public export credit agencies and multilateral guarantees remained essential. Looking ahead, sentiment by late 2025 was cautiously optimistic.

Latin America’s trade finance environment in 2025 reflected a combination of cyclical opportunity and structural constraint. Commodity strength provided momentum, particularly in South America, where agricultural, mining and energy exports supported liquidity across supply chains. Brazil stood out as a regional driver, benefitting from strong demand for agricultural products and minerals, while higher commodity-linked revenues translated into increased trade finance activity as exporters discounted receivables and importers sought funding for capital goods and production expansion. Elsewhere, macroeconomic volatility continued to shape outcomes. Currency instability in countries such as Argentina complicated trade planning and reinforced the importance of flexible financing structures and reliable access to working capital.

Across the region, development banks and public institutions remained central to sustaining trade flows. In Brazil, the national development bank BNDES expanded programmes to support exports of machinery and equipment, with commercial banks acting as execution partners. In the Pacific Alliance countries, regional cooperation was reinforced through trade credit lines provided by development institutions, supporting intra-regional trade at a time when global risk appetite remained selective. These mechanisms played a critical role in bridging the trade finance gap, which remains significant across Latin America, particularly for SMEs.

Sustainability also featured more prominently in the region’s trade finance narrative. Latin America’s role as a supplier of certified agricultural products and sustainably managed natural resources supported the expansion of green and social trade finance structures, often in partnership with development institutions. Trade finance linked to essential imports and climate adaptation goods gained visibility, particularly in Central America and the Caribbean, where vulnerability to climate events remains acute.

Within this context, corporates consistently framed trade finance relationships around execution, access and the ability to connect local activity with global flows.

At HSBC, Latin American corporates position the bank as an enabler of international connectivity. Vivek Ramachandran, HSBC’s head of global trade solutions, notes rising demand for solutions that help release liquidity, inject funding into supply chains or mitigate risk at specific points in the trade cycle. “There’s been much more demand for bespoke solutions as a result,” he says, particularly as companies experiment with off-balance sheet options.

A wholesale trade corporate in Mexico highlights that HSBC “facilitates cross-border transactions and financing”, pairing this with praise for its “advanced digital tools”. Another Mexican respondent emphasises the value of access to expertise, noting that with international operations they can “easily contact HSBC advisrs and resolve any problems or questions”. These perspectives reinforce HSBC’s role in supporting corporates that require consistent execution across borders and rapid issue resolution when managing complex trade flows.

For Itaú Unibanco, client feedback underscores the importance of balance-sheet access, local market knowledge and flexibility across volatile cycles. Corporates in Brazil and Uruguay consistently reference access to financing and adaptable structuring as defining strengths. A head of treasury in Uruguay’s agriculture sector highlights the importance of financing capacity and conditions when supporting working-capital-intensive activity. Others point to breadth and responsiveness. A head of treasury in Uruguay’s information technology sector highlights “different products, advice [and] response”, while a regional respondent in Brazil points to “agility, especially in credit assignment”, reflecting the value of fast decision-making. Access to core trade instruments remains central. A wholesale trade client in Uruguay references lines of credit and LC as essential, while a finance director in Brazil’s equipment sector highlights Itaú’s role as a primary provider for trade-related activity. A regional finance director in Brazil’s manufacturing sector describes the bank as the “best bank for Brazil – innovative and flexible in its approach”, reinforcing the strength of its domestic franchise.

At BBVA, the trade finance proposition reflects the realities of operating in fragmented and volatile markets. The bank has focused on receivables finance, supply chain finance and factoring to support corporates managing extended payment terms and fluctuating demand. Client feedback highlights execution quality and relationship accessibility. Digital capability increasingly underpins this experience. A senior financial manager in Mexico’s industrials sector points to “software and factoring” as particular strengths, while others reference the breadth and availability of solutions when operating in situational market environments.

Santander has continued to scale its Trade and Working Capital Solutions franchise across Latin America, supporting a broad base of buyers and suppliers through guarantees, documentary trade and supply chain finance. Its regional model links local specialists with global relationship teams, enabling consistency while navigating regulatory and operational complexity. Throughout recent years, the bank has expanded structured solutions that integrate receivables, payables and inventory finance, helping corporates unlock liquidity and strengthen supply chain resilience. Sector-led origination teams have further reinforced advisory depth, aligning trade finance more closely with corporate strategy and sustainability objectives.

At Citi, trade finance in Latin America is closely tied to development-led partnerships and focus on clients to increase resilience of their supply chains. Citi has also enhanced its trade and working capital proposition through digitalisation, replacing paper-based instruments with integrated discounting platforms and improving efficiency for buyers and suppliers. In Colombia and Central America, social trade finance structures have supported access to working capital for local enterprises, reinforcing Citi’s role in linking trade finance with inclusive growth. Sustainability is increasingly embedded in this approach, with trade-linked structures aligned to environmental and social targets supporting the bank’s broader transition finance ambitions.

Overall, Latin America’s trade finance landscape in 2025 was characterised by opportunity tempered by volatility. Commodity strength, nearshoring dynamics – particularly in Mexico – and regulatory progress supported growth, while currency instability and political uncertainty required careful risk management. Trade finance remained essential to unlocking growth across the region and the institutions that stood out were those able to combine access to balance sheet, execution certainty and structured solutions that adapt to local realities while connecting Latin America to global trade flows.

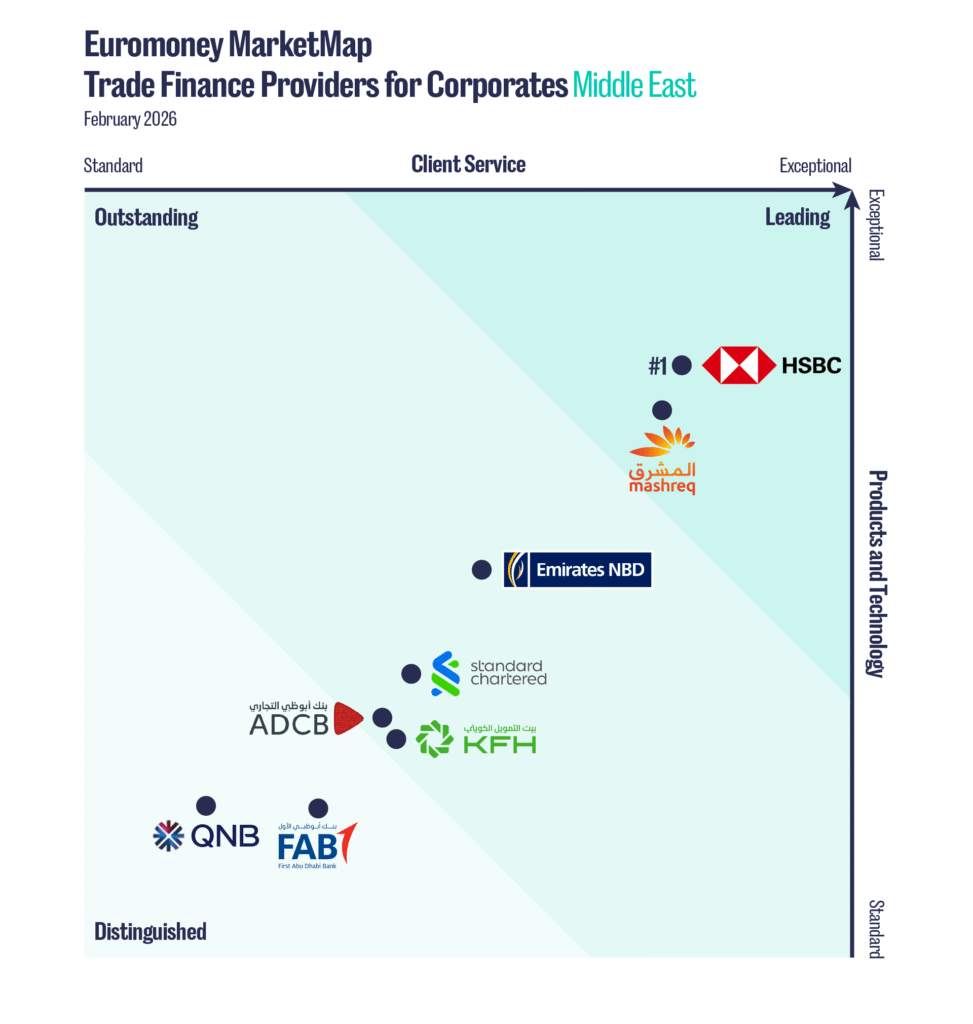

The Middle East’s trade finance landscape in 2025 was defined by volume, velocity and ambition. Elevated hydrocarbon revenues in parts of the Gulf supported liquidity and sustained import demand, while economic diversification strategies across the Gulf Cooperation Council (GCC) continued to generate trade flows linked to infrastructure, manufacturing and renewables. The result was a market in which traditional energy-linked trade remained significant, but non-oil activity increasingly shaped the pipeline, particularly around machinery imports, project supply chains and the early build-out of new export sectors.

In parallel, intra-regional trade gathered momentum as political ties stabilised and regional supply chains deepened, reinforcing demand for dependable trade instruments that could move quickly across borders and regulatory regimes.

Digital trade continued to move from aspiration to execution in the region. The region’s appetite for emerging technology remained visible in pilots around document exchange, transparency and data-sharing, and while not all initiatives reached scale, the practical direction of travel was clear: digitisation in the Middle East was increasingly driven by usability and throughput rather than experimentation.

Across client feedback, the differentiators that mattered most were consistent: the ability to execute at speed; provide certainty in documentation and risk cover; and deliver digital access that reduces friction without compromising control. Respondents also highlight the value of banks that understand local regulatory environments well enough to make global products work smoothly in fast-evolving jurisdictions.

HSBC stands out in this context as a provider that corporates associate with deep advisory capabilities. Respondents highlight the bank’s understanding of regulatory requirements and market dynamics across jurisdictions, not as a substitute for global capability, but as an enabler of smoother delivery. Digital tools are referenced in practical terms, and linked to ease of implementation and efficiency. An information technology corporate operating domestically in Saudi Arabia highlights “fast response” and “automation of paperless transactions”. A Qatar-based financial services corporate with regional scope describes HSBC as offering “a full solution in terms of online banking and trade finance”, while emphasising “timely response and a proactive attitude”. This focus on execution is reinforced by a Bahrain-based construction company, which notes that HSBC’s teams “understand our business and react quickly when needed”. The throughline is not relationship depth for its own sake but relationship management that reduces operational friction and speeds up resolution.

Mashreq is positioned by respondents as a bank built for the region’s high-frequency trade flows, with reliability and consistent delivery emerging as recurring themes. For some corporates, Mashreq is not one provider among many, but the default. A managing director in wholesale trade notes “we exclusively use Mashreq Bank as our principal trade finance provider”, underscoring the concentration of trade activity that certain banks can command in the region when they combine digital access with predictable processing. References to online access and straightforward handling reinforce the idea that digital capability is valued when it removes steps and shortens cycle times rather than when it introduces novelty.

Emirates NBD’s proposition is framed by corporates around capacity, breadth and operational pace, reflecting the importance of balance-sheet-backed support in a region where trade is tied closely to projects and large import programmes. Clients reference access to facilities and trade-related credit support as decisive in managing trade volumes. A finance manager in the UAE’s transportation sector emphasises access to a credit line facility, while a global executive in construction points to the “size and availability of project standby facilities”. Execution speed is repeatedly linked to service quality and turnaround times. A UAE-based healthcare client highlights “service, quick in processing”. Core documentary activity remains central in client descriptions. A finance manager in wholesale trade points to “import letters of credit, export letters of credit handling”, while others reference LC issuance and authorisation, reinforcing that the bank’s strength is judged on the daily mechanics of trade execution.

Standard Chartered is positioned by respondents as an international connector for trade structures that cross regional corridors, particularly those linking the Gulf with Asian counterparties. Client feedback emphasises consistency and dependable processing of core instruments. A manufacturing client highlights the bank’s strength in facilitating LC for transactions involving Asian counterparties, while others reference straightforward handling and reliable execution when trade instruments need to move quickly through approval and documentation cycles.

Kuwait Finance House (KFH) occupies a distinct place in the regional landscape through Shariah-compliant trade and working-capital solutions. Its relevance is strongest where corporates require structured instruments aligned with Islamic finance principles across import and export flows.

First Abu Dhabi Bank (FAB) is framed by clients as a high-throughput provider with a focus on speed, product depth and operational simplicity. Respondents repeatedly highlight execution efficiency and reduced friction in documentation handling. A finance director in the UAE’s real estate sector points to a “speedy process with less documentation”, while a finance manager in wholesale trade states that “the transaction processing speed is better than others”. Service support and responsiveness appear frequently in client comments. A head of treasury highlights “support [and] assistance”, while an accountant in construction notes “quick service”. Others point to facility support as central for working-capital-intensive activity, including references to banking credit facilities and credit facility availability. Regional understanding also emerges where corporates operate across multiple Gulf markets. A regional head of treasury in consumer discretionary highlights FAB’s “strong understanding” of the regional market, reflecting the increasing importance of cross-GCC execution as trade flows expand beyond single-country footprints.

The Middle East’s trade finance story in 2025 is focused on growth. Digitisation is advancing fastest where it reduces steps, shortens turnaround times and improves control, rather than where it adds complexity. As the region’s diversification agenda accelerates, trade finance is increasingly shaped by non-oil sectors, project supply chains and intra-regional corridors that demand scale and precision. The test for providers will be to sustain this execution standard as volatility shifts and as the region’s trade mix becomes broader, more complex and less anchored to a single commodity cycle.

Trade volumes grew modestly across Western European countries, supported by a weaker euro earlier in the year and a gradual normalisation of intra-EU trade as post pandemic and geopolitical effects faded. Germany, France and Italy all recorded export upticks, although elevated energy costs at the start of the year continued to weigh on energy-intensive sectors.

What set Western Europe apart in 2025 was institutional maturity. The region led globally on legal modernisation for trade documentation. The UK’s Electronic Trade Documents Act had moved from theory to practice, with corporates beginning to use eBL and promissory notes in live transactions. Across the EU, progress was tangible: Germany expanded its electronic securities framework to cover trade documents; France clarified what constitutes a “reliable system” for digital originals; the Netherlands moved closer to recognising electronic negotiable instruments. While interoperability questions remain, these developments collectively positioned Western Europe as one of the most legally advanced environments for paperless trade.

Corporate feedback consistently points to the same priorities: transaction efficiency, predictability and access to expertise. Corporates reward banks that execute accurately, communicate clearly and integrate trade finance smoothly into broader treasury operations.

At HSBC, corporates emphasise reliability and access to informed decision-makers. A German industrial corporate with domestic operations describes the bank’s strengths as “local contacts, direct customer contact, quick feedback, reliable service”. Speed and clarity of communication recur across responses. A UK-based retail trade corporate notes that HSBC “excels in trade finance and cross-border business banking”, adding that a documentary credit transaction “went through smoothly, ensuring no delays in shipping”. Another European manufacturing corporate highlights “accurate documentation and timely processing”, reinforcing that in trade-heavy sectors, correctness and turnaround time remain decisive.

For ING, corporates highlight the trade finance proposition around collaboration and breadth rather than transactional execution alone. Clients in the Netherlands and the UK consistently highlight the bank’s ability to combine a wide range of trade and working-capital solutions with a cooperative service model. A chief financial officer in manufacturing describes ING’s approach as offering “different products, ensuring a fair collaboration”, while a senior financial manager in the Netherlands’ construction sector summarises the experience as “helpful”. Automation and digital tooling also feature in the corporates’ feedback.

At Crédit Agricole, trade finance in Western Europe is associated with advisory depth and structured execution. Clients across France, Italy and Germany consistently reference the bank’s strength in guarantees, LC and complex cross-border arrangements. The bank is recognised also by its ability to offer tailored solutions. A senior corporate executive in Italy highlights the bank’s “readiness to accommodate customer requests”. In transaction-driven situations, risk expertise matters. A chief executive officer in Germany’s financials sector points to “risk appetite, forfaiting and bridge financing”. Digital capability reinforces this proposition. A finance manager in France’s transportation sector highlights the efficiency of LC processing, while others point to rapid response and efficiency in global transactions.

Santander has continued to expand its trade and working-capital franchise across Western Europe through a model that integrates local execution with structured solutions. The bank’s co-founding of Invensa – a platform combining trade finance expertise with alternative credit to provide inventory financing – illustrates a broader shift toward hybrid models that extend beyond traditional bank balance sheets. This approach reflects growing corporate demand for integrated solutions spanning receivables, payables and inventory, particularly in capital-intensive sectors.

For UniCredit, corporate feedback highlights service reliability and coordination across borders. “UniCredit operates a matrix model with a global product factory ensuring consistency across markets while allowing local adaptation,” explains Francesca Nenci, global head of trade and corresponding banking, UniCredit.

Clients in Italy and Austria reference dependable execution as a baseline expectation in mature markets. “Our starting point is not the product,” Nenci adds. “We work with the client to understand their liquidity needs and the results they are expecting. Based on that, we propose the best solution, which can be either a trade related one or even another solution offered by the bank.”

A chief executive officer in Austria’s industrials sector points simply to service, while a senior financial manager with regional responsibility in construction highlights communication as a defining strength. In a region where corporates typically work with multiple banks, UniCredit’s value lies in consistency and clarity when managing trade activity across jurisdictions.

Beyond client accolades, Nenci underscores that her business’ progress is reflected not only in sentiment, but in hard metrics: “despite declining trade volumes seen in SWIFT data, UniCredit increased its trade finance penetration. This was the result of our focus on service quality, innovation and digitalization initiatives.”

At Deutsche Bank, trade finance relevance in Western Europe is closely tied to risk-management capability and integration within multinational banking structures. Clients highlight the bank’s role in cross-border trade where mandates are often designated at parent-company level. Risk and compliance expertise are central to this positioning, particularly in managing confirmations, transactions with embedded FX and navigating the sanctions landscape. Service consistency also features, with a healthcare-sector respondent underscoring the importance they place on predictability.

BNP Paribas is positioned by corporates around product depth and platform capability. Clients across France, Belgium, Italy, Germany and Spain frequently reference bank guarantees, credit management and factoring as core strengths. Platform quality reinforces this. A finance manager in the construction sector describes BNPP as having “the best platform for handling bank guarantees”, while others highlight responsiveness, advice and availability of confirmations. The bank’s investments in digital self-service tools and automation resonate in a region where efficiency gains matter more than novelty.

At Societe Generale, trade finance differentiation increasingly comes from technology applied to control and insight. AI is used to support document verification, fraud detection and predictive analysis across LC and trade workflows. These tools are paired with structured implementation and training, ensuring adoption translates into operational value. Sustainability is also embedded in the bank’s transaction banking framework, providing corporates with a structured way to classify and benchmark ESG-linked trade activity as disclosure requirements intensify.

For Commerzbank, corporates emphasise operational efficiency and local execution. Clients across Germany, Belgium, Switzerland and Italy highlight simplified processing and speed. Structured working-capital solutions also stand out. A global head of treasury in transportation points to reverse factoring as a differentiator, while relationship quality remains central. A chief executive officer in German industrials highlights “excellent advice and accessibility of the customer team”, reinforcing Commerzbank’s role as a pragmatic execution partner in demanding markets.

Overall, Western Europe’s trade finance story in 2025 was one of institutional strength. Digitisation and sustainability were not emerging themes but embedded priorities, supported by advanced legal frameworks and deep banking expertise. Even as geopolitical and economic pressures persisted, the region remained a global centre of trade finance capability, defined by precision, compliance and the ability to execute complex trade reliably at scale.

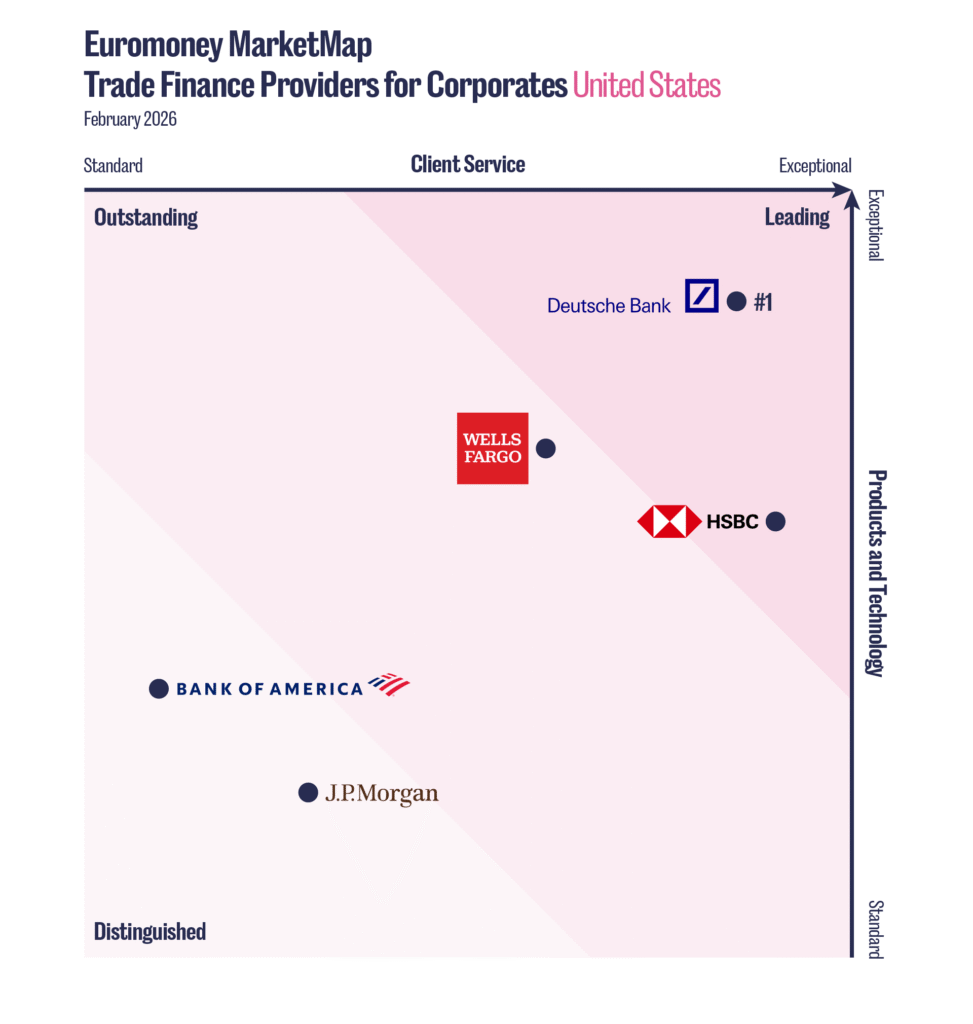

North America’s trade finance landscape in 2025 was shaped by balance-sheet optimisation. Robust consumer demand sustained high import flows into the US, while regional supply chains under the US-Mexico-Canada Agreement (USMCA) framework continued to deepen, particularly across automotive, electronics and energy-related sectors. The US remained structurally open-account driven, with corporates relying heavily on supply chain finance, receivables solutions and credit insurance to manage cash conversion cycles. With interest rates remaining elevated through much of the year, working-capital efficiency became a board-level priority, reinforcing demand for trade-linked liquidity solutions.

Within this environment, banks focused on embedding trade finance more tightly into day-to-day operational flows. The emphasis was on speed and integration at scale. By mid-2025, more than 30 US states had adopted amendments to the Uniform Commercial Code enabling electronic negotiable instruments, a critical step towards recognising eBL and warehouse receipts. While the US still lacks a single federal framework equivalent to the MLETR, the legal trajectory is now clearly supportive, and major banks are actively preparing their systems for wider digital document usage.

Regional trade under USMCA continued to be a structural tailwind. More manufacturing activity flowed through Mexico, supported by US and Canadian banks providing trade loans, factoring and supply chain finance, often alongside development institutions to mitigate risk. Export credit agencies remained central. The US Export-Import Bank and Export Development Canada both played an active role in backstopping exporters and their supply chains, particularly in strategic sectors such as energy, infrastructure and advanced manufacturing.

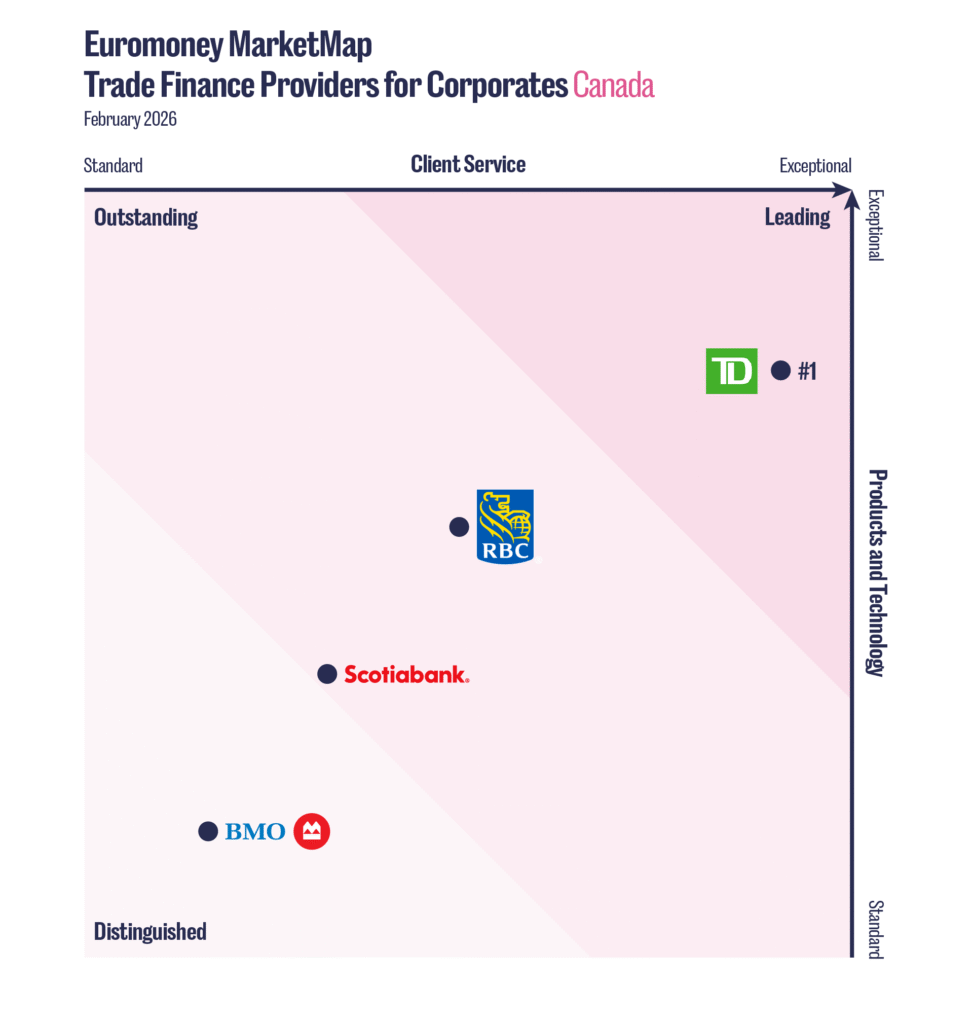

TD’s trade finance strategy in North America is positioned less around standalone instruments and more around platform coherence, workflow simplification and deeper treasury integration. In an environment shaped by working-capital pressure and reconfigured supply chains, the focus has shifted toward integrated trade solutions that support import, export and risk-mitigation requirements within a single, coordinated framework. “Rather than building separate solutions for large corporates, mid-market and SMEs, we are making unified investments in our platform, technology and operations to deliver a one TD solution that serves all client segments,” explains Guillermo Aymard, global head of trade and working capital, global transaction banking at TD Securities.

The product set remains anchored in core instruments familiar to international corporates – import and export LC, standby LC, documentary collections and bankers’ acceptances – but the differentiation lies in how they are structured and delivered. TD places emphasis on tailored risk mitigation and liquidity support, with representatives working alongside clients to calibrate solutions around risks embedded in cross-border activity.

Central to this model is a consultative posture. Rather than leading with product, TD frames client dialogue around treasury priorities and operational friction points, shaping structures in response. “A question we like to ask clients is: what are your two or three key treasury priorities over the coming year? That becomes the jumping-off point for co-creation,” adds Aymard. “Our teams work in lockstep with clients to understand their needs and catalyse idea generation leading to execution. We share our roadmap, incorporate their feedback and maintain open dialogue to align trade finance solutions more closely with their real operating priorities.” The strategy reflects a deliberate move toward institutionalised co-creation, aligning trade finance more closely with the commercial realities and risk profiles of North American corporates.

Aymard explains TD’s success: “it comes down to three things: i) dedicated coverage, ii) a commitment to operational excellence, and iii) a focus on advisory, with the client at the heart of it all. It sounds simple, but it is difficult to get right. Client service is in the DNA of this institution.”

Scotiabank stands out for its corridor-based strategy across Canada, the US and Mexico. As the only Canadian bank with full transaction banking operations spanning all three markets, Scotiabank enables clients to move liquidity seamlessly across North America’s largest free-trade zone. Alongside this geographic positioning, the bank has invested heavily in internal automation. Its global transaction banking team deployed robotic process automation within supply chain finance operations, automatically feeding transaction data into loan-booking systems.

BMO is recognised for its Canada-US corridor. Clients highlight its structured trade capabilities, balance-sheet support and sector-led advisory model, especially in capital-intensive industries.

RBC, meanwhile, is consistently associated with execution reliability and treasury integration. Its strength lies in combining trade finance with broader cash management and FX capabilities, offering corporates coordinated solutions.

Among global banks, Deutsche Bank is positioned in the US as a partner for complex, multi-jurisdictional trade structures. Corporate feedback consistently highlights global reach and execution capability. A head of treasury in manufacturing points to Deutsche’s “industry knowledge, global scope and professional team”, while a managing director in the energy sector highlights support for “different transactions and diversification”, alongside speed and clarity of communication. Structural capability is repeatedly referenced. An analyst in manufacturing cites “facility structure, regional presence and consistent fee structure”, underscoring the importance of predictability when managing large trade-related facilities. Balance-sheet capacity also matters. An accountant notes that Deutsche acts as the “principal provider”, supplying a large credit line that anchors relationships with other banks. Execution responsiveness reinforces this positioning. A finance director highlights “extremely fast processing speed compared with other providers” and a team that is “very responsive and takes initiative to power through situational complications”.

At HSBC, the focus in North America has been on embedding trade finance into specific payment and operational pain points. With tariff uncertainty and elevated duty costs still weighing on importers, HSBC expanded its TradePay proposition in the US to cover import duties. The solution allows the bank to settle customs duties directly on behalf of clients under agreed credit terms, integrating duty financing into the trade workflow and reducing liquidity strain at the point of import. Since its initial rollout, TradePay has seen strong uptake, reflecting corporate appetite for targeted, use-case-driven trade finance rather than generic facilities. Looking ahead to 2026, HSBC sees scope to extend TradePay with additional digital features and to support not only buyers but also sellers. Enabled by the bank’s HTS platform, Vivek Ramachandran, head of global trade solutions describes it as “the right product at the right time.”

“Historically, trade finance has been split between very paper-based trade and highly structured receivables products, leaving a big white space in between,” Ramachandran explains. Companies often filled that gap through overdrafts or short-term facilities. TradePay was designed to address it through a different construct: “a fully digital trade loan, where suppliers are paid directly and the buyer repays the bank. It is self-liquidating, linked to your working capital cycle and fully digital.”

Large domestic banks continued to scale supply chain finance and receivables platforms. Bank of America deepened its focus on automation and supplier accessibility. Its Open Account Automation platform processed tens of thousands of transactions with straight-through processing rates exceeding 95%, compressing invoice approval times from weeks to seconds. Integration into CashPro Supply Chain Solutions allowed buyers and suppliers to manage payables and early payments within a single interface. The bank also piloted automated supplier verification, addressing one of the most persistent onboarding bottlenecks in trade finance and laying the groundwork for broader rollout.

Across the market, fintech collaboration increased. US banks partnered with third-party platforms to extend reach into supplier ecosystems, particularly among mid-sized corporates that historically sat outside large buyer-led programmes. At the same time, blockchain experimentation continued at the infrastructure level.

Risk and compliance remained a defining constraint. Sanctions regimes, anti-money laundering (AML) requirements and internal concentration limits meant banks continued to be selective in certain corridors, even as regulators acknowledged the low-risk, short-tenor nature of trade finance. Supervisors increasingly focused on supply chain resilience, stress-testing exposures to potential disruptions rather than questioning the asset class itself.

Trade products: Importance vs Satisfaction Matrix

Based on corporates’ assessment, Euromoney introduces the Importance vs Satisfaction Matrix, a visual framework that plots the perceived importance of individual trade products against clients’ satisfaction with current bank offerings, across regions. The matrix provides a clear lens on where banks are meeting expectations and where gaps remain.

Further detail on the methodology underpinning these results is available in the methodology guidelines.

Getting the fundamentals right

Products such as guarantees, LC, working-capital solutions, trade loans and foreign exchange services sit firmly in the high-importance, high-satisfaction quadrant. These are high-impact strengths and their positioning reflects a pattern that has remained consistent over recent years: the enduring importance of getting the fundamentals right.

“Trade finance and working capital were going in opposite directions in 2025. Volumes of traditional trade financing lowered according to SWIFT data, with some clients still shifting toward current account and working capital solutions, and others putting big projects on hold due to heightened geopolitical risk,” explains Francesca Nenci, global head of trade and corresponding banking, UniCredit.

For corporates, strong core trade products are non-negotiable. For banks, delivering them reliably is the result of long-term investment. High satisfaction in this category reflects years of work in process standardisation, global risk coverage, operational resilience and platform stability.

“Trade finance is increasingly embedded as a core treasury function, not just to mitigate transaction and counterparty risk, but to optimise collateral, enhance credit standing and improve working capital,” explains Guillermo Aymard, global head of trade and working capital, global transaction banking at TD Securities. “We have a clear commitment and a relentless focus on service and advisory expertise to assist our clients in that journey.”

There are, however, notable regional divergences. In North America, working-capital solutions are rated as medium in importance, yet satisfaction levels are lower than expected. This gap is particularly striking given the rise in uncertainty during the past 18 months, which has renewed corporate focus on liquidity optimisation, especially in sectors such as industrial goods, electronics and agribusiness, where funding flexibility has become critical.

ESG-linked trade instruments

Survey results suggest that emerging product categories – notably environmental, social and governance (ESG)-linked trade finance and dynamic discounting – remain capabilities with limited relevance. Despite their prominence in industry debate, client demand for ESG-linked trade instruments is still limited, and satisfaction with existing solutions is low.

This reflects the structural complexity of the product. On the corporate side, many firms continue to struggle with the cost, data requirements and operational burden associated with tracking verifiable ESG performance across increasingly fragmented supply chains.

On the bank side, ESG-linked trade solutions are often bespoke, resource-intensive and difficult to scale consistently across regions and client segments. In the absence of unified reporting standards or embedded commercial incentives, ESG integration risks staying reputational rather than functional.

A step toward greater standardisation came in December 2025, when the International Chamber of Commerce (ICC) ratified the Principles for Social Trade Finance (PSoTF) and Sustainability-Linked Supply Chain Finance (PSL-SCF), completing its Principles for Green Trade Finance (PGTF) framework. Developed with input from more than 100 institutions, the framework provides the first global standard for defining and structuring green, social and sustainability-linked trade finance. By aligning with established loan and bond frameworks and introducing governance tools for setting and verifying ESG performance, the ICC aims to reduce greenwashing and enable more consistent evaluation of sustainability in trade. Standard Chartered’s early adoption of the principles marks an important milestone in the push for more credible, transparent and scalable sustainable trade finance.

Secondary market trade capabilities

Dynamic discounting, another frequently cited innovation, shows limited adoption among survey respondents. Uptake appears constrained by the operational burden placed on suppliers and the need for deep integration between procurement and finance systems. For many mid-sized corporates, the required level of data maturity and systems connectivity is not yet in place.

More traditional, relationship-led services – including advisory and documentary collections – are also moving toward niche status. In an environment characterised by geopolitical volatility, regulatory fragmentation and shifting trade corridors, expert advisory remains indispensable for a subset of globally exposed, operationally complex corporates. While not universally demanded, these services present a clear opportunity for differentiation. Banks able to deliver sector-specific, policy-aware guidance – particularly around trade re-routing and supply chain reconfiguration – can create meaningful value for high-priority clients.

“It is not simply about issuing a guarantee or an LC,” reflects UniCredit’s Nenci. “Clients require advisory support to determine the most effective structure to achieve their objectives.”

As trade finance continues to evolve toward embedded solutions, real-time liquidity management and ESG alignment, success will depend less on the product breadth and more on delivery.

The question for banks is no longer whether these capabilities exist, but whether they can be deployed at speed, at scale and in ways that measurably improve client outcomes.

Digital trade adoption

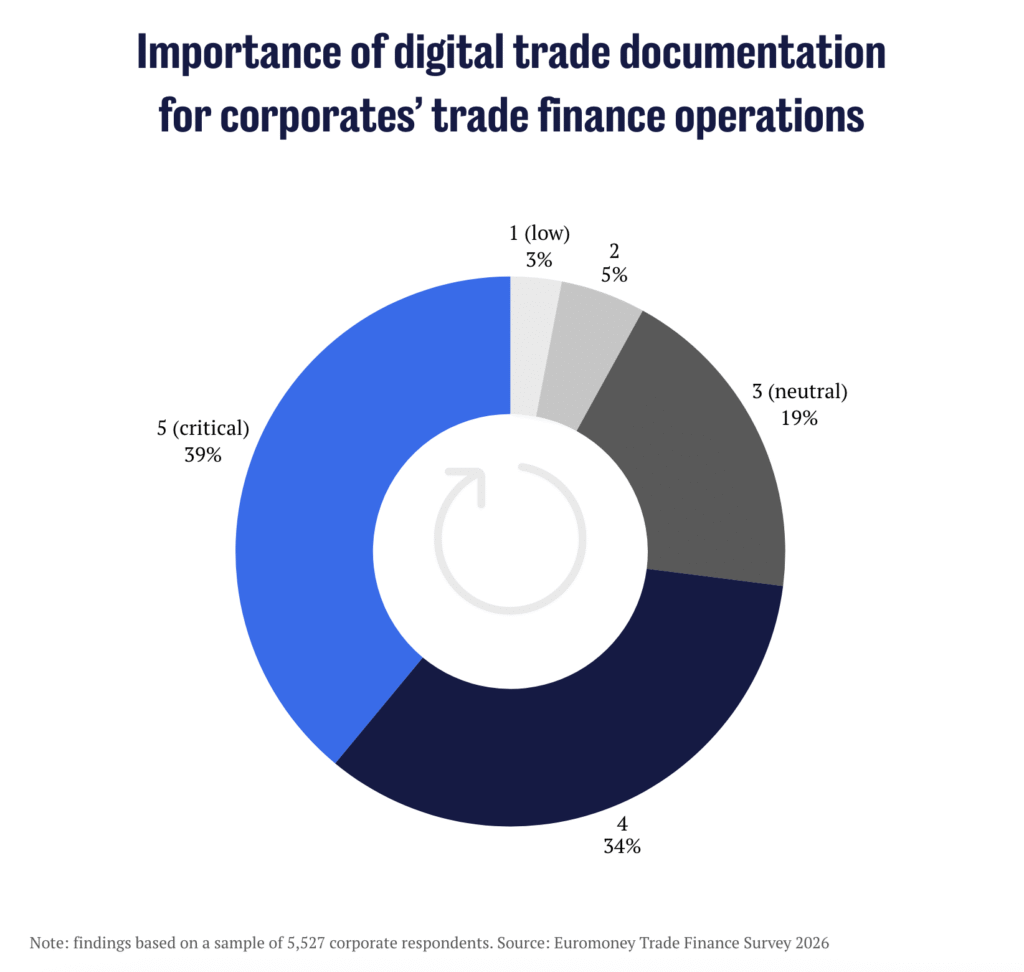

Digital trade documentation is no longer a fringe consideration for corporates. 5,527 respondents ranked the importance of digital trade documentation for their trade finance operations. Of these, 39% consider it critical to their trade finance operations, while a further 34% view it as important. Together, this signals broad recognition that electronic bills of lading (eBL), digital LC and other transferable records will be central to the future of trade finance.

Yet, importance does not automatically translate into adoption. Despite near-universal awareness of the benefits of digital trade documentation, progress remains uneven, shaped by practical and economic constraints rather than conceptual resistance.

“Broadly speaking, the rate of technological innovation and iteration cannot be overstated. In the context of Trade Finance, while meaningful efficiencies have been achieved through digitalization efforts along the value chain, this is just scratching the surface. The challenge to accelerated adoption is that digital ambitions appear to be at odds with analogue dependencies and realities,” says Guillermo Aymard, global head of trade and working capital, global transaction banking, TD Securities.

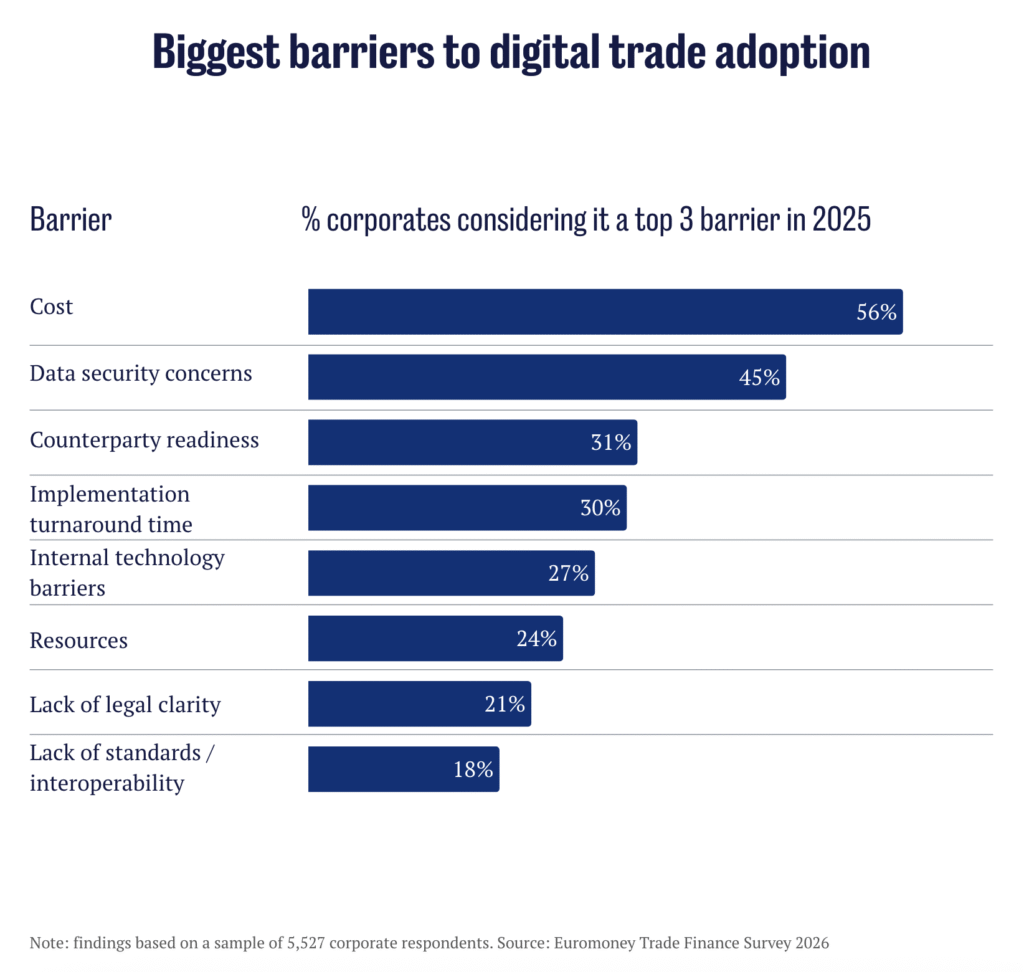

Cost and security dominate adoption barriers

When asked to identify the top-three barriers to adopting digital trade solutions, cost emerged as the most frequently cited obstacle, flagged by 56% of respondents. This reinforces a persistent industry reality: while the efficiency gains of digitalisation are well understood, the upfront investment required to modernise systems, integrate platforms and retrain teams continues to delay implementation. For many corporates operating in legacy-heavy environments, digital trade still competes with other technology priorities for scarce capital and resources.

“For us, it is a balancing act between blue-sky thinking and tackling day-to-day client priorities as we iterate on our product roadmap and deliverables,” adds TD Securities’ Aymard.

Data security concerns ranked second, cited by 45% of respondents. As trade documentation migrates from paper to cloud-based platforms and API-enabled ecosystems, corporates are increasingly sensitive to cyber risk. Document integrity, data ownership and access controls have become central considerations, particularly for firms operating across multiple jurisdictions and regulatory regimes.

Beyond cost and security, the survey highlights a set of ecosystem-related constraints. Counterparty readiness was identified as a barrier by 31% of respondents, while 30% cited long implementation timelines. These findings underscore a core challenge of digital trade: its value depends on network participation. A corporate’s willingness to digitise is often constrained by the other participants in the ecosystem.

Internal constraints also remain material. More than a quarter of respondents pointed to internal technology limitations, while 24% cited resource constraints. In practice, this suggests that many firms possess strategic intent, but lack the operational capacity to execute digital trade initiatives at scale.

Structural barriers recede

Notably, long-standing structural barriers ranked low. Only 21% of respondents cited a lack of legal clarity as a top barrier, while 18% pointed to inconsistent standards and interoperability. This marks a meaningful shift.

“The persistence of paper-based processes is often regulatory rather than technological, with cross-jurisdictional legal fragmentation limiting full digitalisation. On average, we touch 20 jurisdictions in cross-border transactions,” highlights Francesca Nenci, global head of trade and corresponding banking, UniCredit.

Work led by organisations such as the ICC has begun to translate into tangible progress. The adoption of legal frameworks aligned with the United Nations Commission on International Trade Law’s (UNCITRAL) Model Law on Electronic Transferable Records (MLETR), alongside initiatives such as the ICC’s Digital Standards Initiative (DSI), has reduced uncertainty around the legal recognition of electronic trade documents in a growing number of jurisdictions.

Global harmonisation is still incomplete and for many corporates operating across fragmented legal regimes, uncertainty around enforceability and cross-border recognition is still a deterrent. Structural barriers may be receding, but they have not disappeared.

From pilots to production

2025 marked a year of visible progress in digital trade execution. More jurisdictions adopted or advanced legislation recognising electronic transferable records, laying the groundwork for paperless trade finance.

Adoption of eBL also accelerated, with organisations such as Digital Container Shipping Association (DCSA) committing to 100% adoption by 2030. As a milestone in this journey, in May 2025, DCSA, in collaboration with BIMCO and FIATA, successfully completed the first fully interoperable trial between WaveBL and edoxOnline, two major eBL solution providers, enabling the transfer of eBL between platforms without reverting to paper.

At the same time, progress on application programming interface (API) standards and bank connectivity began to reduce fragmentation between trade platforms, banks and corporate systems, improving interoperability and straight-through processing.

These advances remain unevenly distributed, though. Digital trade is scaling fastest in corridors and sectors where regulatory clarity, counterparty alignment and platform maturity converge. Elsewhere, adoption remains cautious and incremental.

Adoption is an economic decision, not a technical one

The Euromoney survey data makes one point clear: digital trade adoption is no longer constrained by lack of awareness or absence of viable technology. Instead, it is shaped by economics, ecosystem readiness and risk perception.

“There is huge potential for AI to simplify and accelerate processes in trade finance, but uptake is currently constrained by the lack of standardised documentation across jurisdictions,” adds UniCredit’s Nenci.

Corporates broadly accept that digital documentation will be critical to the future of trade finance. But for many, the business case remains finely balanced. Without clear cost savings, faster financing outcomes or reduced risk exposure, digital trade initiatives struggle to displace entrenched paper-based processes.

The next phase of adoption will depend on lower-cost deployment models, shared infrastructure, clearer legal convergence and deeper integration into existing trade and treasury workflows.

2026 and beyond

2025 marked a turning point for trade finance, not because volumes returned to record levels, but because the industry evolved in how it supports global commerce. As trade rebounded, banks, corporates and policymakers shifted the focus from scale to quality: faster execution, deeper integration, stronger risk mitigation and clearer alignment with sustainability objectives. Trade finance became more digital, more targeted and more embedded in real economic activity.

Across markets, innovation moved decisively from pilots to production. Fully digital trade instruments, API-enabled workflows and the use of AI in document checking and compliance reduced friction in what has historically been one of banking’s most operationally complex businesses. At the same time, banks demonstrated greater agility, tailoring solutions to specific client pain points and regulatory shifts rather than relying on one-size-fits-all products.

The global trade environment remains volatile, shaped by geopolitics, technology investment and shifting alliances. What has changed is how corporates respond. “Agility has become a real mantra for companies we are talking to,” Vivek Ramachandran, head of global trade solutions concludes.

Yet, challenges remain. The global trade finance gap continues to constrain SMEs and emerging-market firms, with access issues often driven as much by complexity and self-rationing as by outright rejection. Encouragingly, 2025 showed increased momentum behind digital platforms, fintech partnerships and multilateral risk-sharing aimed at narrowing that gap.

“Trade is a business and an instrument that is enabling economies to grow. We have a duty to continuously innovate,” emphasises Francesca Nenci, global head of trade and corresponding banking, UniCredit.

Looking ahead, the direction is clear. Trade finance will continue to matter not simply as a source of liquidity but as infrastructure: connecting markets, absorbing shocks and enabling trade to function in an increasingly fragmented world.