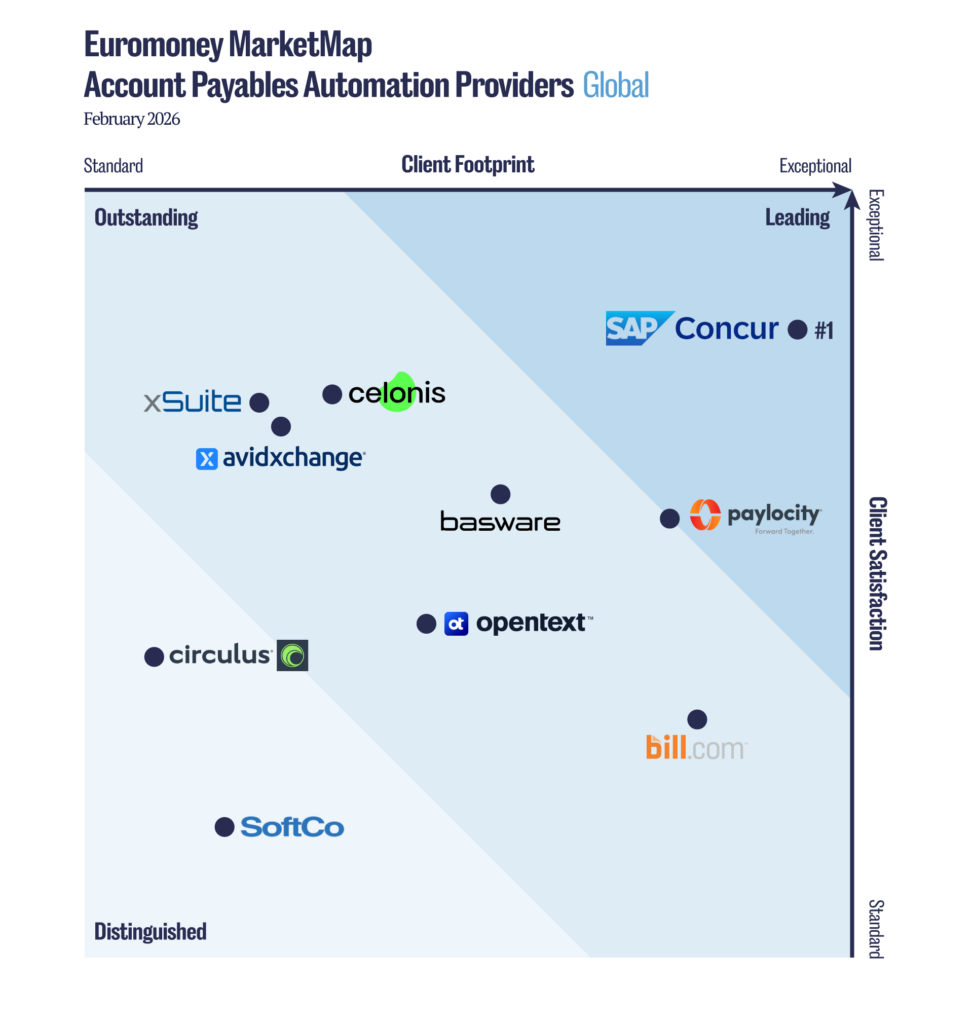

Accounts payable is no longer just about efficiency. More than 1,700 corporates ranked their AP providers, rewarding breadth, targeted automation, fraud resilience and ongoing innovation.

For decades, accounts payable (AP) was primarily judged on efficiency. Success was measured in throughput: how quickly invoices moved through the system, how reliably errors were avoided and how tightly costs were controlled. Early automation efforts reflected that focus, concentrating on digitising paper and removing manual steps, often without addressing how AP connected to upstream procurement or downstream cash management.

That efficiency-first framing is no longer sufficient on its own. Today’s AP function sits at the intersection of working-capital management, data governance, fraud prevention and regulatory compliance. It touches procurement, treasury, supply chain and finance operations more broadly. As expectations rise, finance teams are paying closer attention to the underlying systems: what they can prove; what the system can explain; and the risks it can stop. AP is no longer judged only on speed but on what it reveals about how the business actually runs.

Respondents to the Euromoney Cash Management Survey 2025 identified the top 10 AP automation providers globally. The ranking is based on feedback from 1,722 corporates – ranging from small and medium-sized enterprises (SMEs) to large multinationals – across 68 countries that use AP automation providers in their operations.

The data layer CFOs demand

In many ways, AP reflects the health of the wider organisation. Issues in procurement discipline, supplier management or inventory controls inevitably surface in invoice processing, approvals and payments. Payables is often where upstream problems become visible.

AP tools are being built for the messy middle: the handoffs between intake, procurement, receipt, approval and cash. Invoice automation alone is no longer enough. What matters is how AP connects into the full lifecycle of spend, from intake and procurement through to reconciliation, reporting and cash visibility.

In large, operationally complex organisations, the link is clearest where invoices meet physical goods. In retail and manufacturing, payables automation can influence how quickly deliveries are accepted, inventory is released and products reach the shelf. “If you don’t have the proper data layer, you won’t get the outcomes or accuracy the Office of the CFO needs,” says Sonduren Fanarredha, director of product marketing for finance and IT solutions at Paylocity. “There are deterministic rules that need to be black and white, but there are also use cases where AI can do a lot of the work, as long as it has the right context.”

In practice, automation is no longer a feature decision. It is a process decision about which steps deserve straight-through treatment and which require human intervention, because the risk is real. “If you focus on just one sub-process, you might improve it but create problems elsewhere,” notes Steffen Winkler, finance lead at Celonis. “Without understanding how the business actually runs, automation is blind.”

Top ranked AP providers

The MarketMap presents the top 10 providers on two axes:

• Client footprint, indicating the scale of the solution based on the number of corporates that reference it.

• Client satisfaction, calculated as a simple average of respondents’ ratings. The measure is unweighted and includes the full sample, regardless of respondents’ roles or company size.

The results reflect corporate usage and client satisfaction, with no adjustments from Euromoney.

In today’s market, capabilities such as invoice capture, matching, approvals and payments are table stakes. Corporates ranked highly those AP automation providers that went beyond simply delivering technology and instead worked alongside them to determine where automation would create the greatest impact, how far it should extend across the spend lifecycle and how resilient it would be under regulatory and operational pressure.

“Automation should follow insight, not the other way around,” says Celonis’s Winkler. “Many AP initiatives fail because organisations don’t actually know where their process problems are.” Celonis was ranked by corporates in the Euromoney Cash Management Survey as an Outstanding provider.

Solution breadth matters

Tools that cover more of the spend lifecycle can prevent exceptions earlier and reduce clean-up work later. Narrow tools may remove a single pain point, but leave the underlying complexity untouched.

“We’ve deliberately extended AP beyond bill creation,” Paylocity’s Fanarredha adds. “It starts with intake and guided procurement and runs all the way through reconciliation. That breadth is where you actually remove friction, not just digitise it.”

Cloud platforms and embedded finance models have also lowered the adoption threshold, enabling mid-sized organisations to deploy controls, integrations and payment capabilities that were once the preserve of large enterprises. For example, providers such as BILL, an outstanding provider in the Euromoney MarketMap, have built scale by targeting this segment directly, embedding AP and payment functionality into existing enterprise resource planning (ERP) environments and reducing the need for bespoke infrastructure.

Rethinking e-invoicing

One side-effect of digital payables becoming the norm rather than the exception is their reshaping of regulatory expectations. A critical expression of this shift is the growing wave of e-invoicing mandates being enacted across multiple jurisdictions, forcing finance teams to rethink invoice capture, validation and reporting as regulated processes rather than internal workflows.

While the motive is tax, the burden lands in operations. Each country has its own formats, fields and submission routes, and multinationals are left to make that work without disrupting the process. Basware found that 56% of finance leaders fear their systems cannot keep pace with evolving invoicing and tax mandates, a constraint that is already limiting international expansion.

“At a country level, this is about maximising tax revenue,” says Chris Juneau, senior vice-president and head of product marketing at SAP Concur, which was ranked #1 AP automation provider by corporates. “Compliance isn’t optional and AP workflows have to accommodate that, whether a company operates in one country or 20.”

There’s no need to be bound by the past. People outgrow processes and processes outgrow people

Chris Juneau, SAP Concur

For AP teams, that pressure creates a dual challenge. They must remain compliant across jurisdictions without fragmenting processes or creating parallel workflows that undermine efficiency. More platforms are being asked to sit in the middle, routing invoices and reporting data across different national requirements while keeping a single view of the process.

That shift is pushing AP teams to focus less on interpreting mandates and more on operational readiness, particularly around data quality and supplier behaviour. Vendors such as SoftCo, a Distinguished provider in Euromoney’s MarketMap, increasingly frame e-invoicing compliance as an operating model challenge, where clean master data and a consistent invoice structure matter as much as platform choice.

“This isn’t something you can treat as an add-on,” Fanarredha notes. “If compliance isn’t designed into how the platform works, it becomes a blocker rather than an enabler.”

The market is already moving in that direction. For example, Basware has already secured accreditation to support France’s 2026 e-invoicing mandate, reflecting how platform design and regulatory readiness are now inseparable for companies operating across borders.

Process before platform

Many companies still have not unlocked AI’s full enterprise potential because they lack a shared understanding of how their operations truly function and how to improve them. “This operational context is the essential ingredient AI needs to succeed,” Winkler adds. “Without it, companies will continue to struggle to see a real return on AI.”

This broader framing explains why AP conversations increasingly extend beyond finance. Supply chain disruptions, procurement bottlenecks and even sales operations can all affect invoice accuracy, payment timing and supplier risk. Treating AP as a downstream administrative task ignores those dependencies.

This thinking is also reflected among vendors such as Circulus, another Outstanding provider, which frames AP as one component within a wider CFO technology stack, designed to integrate with ERP, payments and reporting systems rather than operate in isolation.

To make enterprise artificial intelligence (AI) work, AP needs to understand the operational context of how the business runs. Without this shared understanding, companies struggle to see a real return on AI. “By using our Process Intelligence Graph to reveal how processes really work end-to-end, businesses can ensure AI is deployed strategically in the right places rather than just automating in the dark,” Winkler adds. This logic also underpins investment decisions. Rather than rolling out automation uniformly, leading organisations are prioritising areas where invoice volumes are highest, exception rates are costly or payment behaviour directly affects liquidity.

Why automation is not enough

For AP to play a more strategic role, implementation is not a footnote. It is the work. New tools create an opportunity to rethink long-established payables processes. “The goal should never be to automate the current process,” says SAP Concur’s Juneau. “That usually leads to sub-optimal outcomes.”

Approval layers, manual checks and workaround steps often exist for historical reasons that no longer apply. Recreating them in software preserves inefficiency rather than eliminating it. Most of the gains come from subtraction, with fewer approval loops or exceptions created upstream and cleaner supplier data. In systems, applications and products (SAP)-centric supply chains, platforms such as OpenText, an Outstanding provider in the Euromoney MarketMap, increasingly link invoice data to goods receipt, archiving and audit trails, turning what used to be separate handoffs into a single, integrated process.

“There’s no need to be bound by the past,” Juneau adds. “People outgrow processes and processes outgrow people.” Successful AP transformations start with a reset. Best-practice workflows provide a foundation, but flexibility is essential to accommodate growth, acquisitions and regulatory change.

This is particularly acute in the middle market, where finance teams are being asked to scale without additional headcount amid persistent cost pressures. The AvidXchange 2026 Trends Survey found that 96% of middle-market finance teams now feel compelled to “do more with less”, accelerating the move away from manual AP processes.

“Most customers don’t do everything at once,” Fanarredha notes. “They start with AP, solve the biggest pain point and then expand as the organisation is ready.”

AP on the front line of fraud defence

Traditional invoice fraud remains a concern, but the risk profile is evolving. Vulnerabilities now extend well beyond invoice receipt, into supplier onboarding, changes to vendor details and payment redirection. Much of that exposure sits wherever processes still rely on human intervention. “Where there are manual steps, there are gaps in visibility,” says Juneau. “And that’s exactly where risk starts to creep in.”

Fraud attempts are also becoming more sophisticated. Fake invoices are increasingly accompanied by convincing supplier communications, sometimes involving deepfake tactics designed to pressure AP teams into urgent action.

The response is rarely a single new check, but layers of tighter permissions, better audit trails and alerts that flag the odd patterns humans miss. Anomaly detection flags unusual behaviour, while workflow rules restrict changes to sensitive data. Auditability is now assumed. “Customers expect full traceability,” Juneau adds. “Not just what happened, but who interacted with the process and when.”

At a more practical level, some controls are increasingly treated as non-negotiable. “Bank details simply can’t be changed without approval,” says Fanarredha. “That’s not something customers should have to design themselves. It needs to be built in.”

Context again plays a central role. Isolated invoice checks can miss inconsistencies that only become obvious when viewed alongside procurement records, inventory movements or historical supplier behaviour.“What’s becoming more common is not just fake invoices but fake supplier conversations,” explains Winkler. “Cross-process visibility makes those attempts easier to detect.”

Customers consistently say their non-negotiables are don’t pay wrong, don’t pay too much and stay compliant. The challenge is balancing all three without sacrificing speed

Steffen Winkler, Celonis

Despite heightened concern, some finance teams are already seeing tangible benefits. In its 2026 Trends Survey, AvidXchange reports that successful cheque fraud attacks among surveyed customers fell to 25% in 2025, down from 63% the previous year. That progress is changing the focus of AP conversations from fraud prevention alone to how controls are designed, applied and scaled across the business.

As baseline controls mature, the debate in AP is no longer about whether safeguards exist but how intelligently they operate in practice. Invoice matching, approval routing, segregation of duties and audit trails are now expected as standard, particularly in environments subject to regulatory scrutiny and fraud risk.

“Customers consistently say their non-negotiables are don’t pay wrong, don’t pay too much and stay compliant,” says Winkler. “The challenge is balancing all three without sacrificing speed.”

Rigid workflows may satisfy auditors but frustrate users and lead to workarounds. Leading platforms are increasingly focused on configurable controls that adapt based on spend type, value, geography or business unit, rather than enforcing uniform approval paths across the organisation.

“Segregation of duties is non-negotiable,” Fanarredha adds. “But how you apply it – whether it’s single payments, batch payments or thresholds based on materiality – has to be flexible, or people will work around the system.”

What the modern AP function looks like

If the past few years have been about digitising payables, the next phase brings the function closer to decision-making. Processing speed still matters, but it is no longer the primary measure of success. The more telling question is what finance teams can see, influence and anticipate as a result of automating the process.

AP becomes part of decision-making

In the next phase, payables sits closer to decision-making. Data captured at the invoice level feeds cash forecasting, supplier strategy and risk monitoring. Exceptions, rather than transactions, become the focus. When the basics run reliably in the background, the function’s value shifts to interpretation and control.

“The breakthrough is when AP teams only focus on exceptions,” says Fanarredha. “You’re operating from a command centre, with visibility and control in real time.”

That shift changes the skillset and the expectations associated with the role. Familiar operational disciplines such as matching and approvals remain essential, but they sit within a broader framework of data governance, working-capital management and fraud prevention. As platforms connect more tightly into procurement, payments and treasury, the boundaries between functions continue to soften.

For many organisations, the direction of travel is towards a more integrated finance environment in which invoice data informs decisions beyond the payables team. The function becomes a source of insight into supplier behaviour, spending patterns and liquidity exposure, rather than simply a record of what has already happened.

“In five years’ time, AP will be generating key insights back to the business, leveraging the data it processes to inform spending trends, cash-flow management and decision-making across finance,” says Juneau.

An integrated ecosystem

As AP tools assume greater responsibility for timing and control, they are beginning to shape payment execution rather than simply feed it. Several AP specialists are now framing invoice automation as a cash and liquidity visibility tool, emphasising real-time insight into payment timing, auditability and working-capital exposure rather than invoice throughput alone. Dubai-based Serina, for example, positions AP as a shared data layer between finance and treasury rather than a standalone processing function.

That shift is most visible in how payment decisions are made. Payment timing increasingly reflects broader liquidity priorities rather than simple processing efficiency. Early payment discounts, once a straightforward gain, must now be weighed against working-capital needs and funding constraints.

“You can’t optimise payment timing without understanding cash flow,” says Winkler. “Treasury may prioritise liquidity over discounts and AP needs to reflect that.”

No one expects AI to be 100% accurate. What matters is being clear about materiality, where automation makes sense and where humans stay in the loop

Sonduren Fanarredha, Paylocity

This closer relationship between the two functions is reshaping roles. AP teams are expected to provide real-time visibility into invoice status and supplier exposure, while treasury inputs guide payment strategy.

The handoff between ‘processing’ and ‘managing cash’ is becoming harder to distinguish, as invoice workflows are increasingly integrated with payment and working-capital tools.

“I see AP teams moving from being more of a transactional function to a more strategic role in terms of cash management and supplier relations,” says Juneau. “They’re providing real-time insights across the financial process rather than just processing invoices.”

High-tech delivered through human touch

Technology is a clear enabler of the future of AP automation, but it is not the sole determinant. Process discipline, clean data and clear governance remain just as important. The organisations seeing the greatest gains are those that treat automation as a foundation for better decisions, not just a way to reduce manual work.

From that perspective, the most significant change during the next five years may be cultural rather than technical. As platforms link procurement, payments and cash more tightly, the boundaries between functions soften. That is where the role starts to change.

“What we’re seeing is that AP is becoming a source of truth for how the business actually operates,” says Winkler. “If you have transparency over the end-to-end process, you can manage cash, risk and supplier relationships in a much more deliberate way.”

This trajectory does not eliminate the need for careful controls or human judgement. Instead, it raises the level at which those controls are applied. Routine processing recedes into the background, while oversight focuses on exceptions, anomalies and decisions that carry real financial consequences.

The endpoint is not fully autonomous; it is more informed. Payables continues to execute transactions, yet it also shapes how organisations understand and manage their financial flows. In that sense, modern AP is defined by the clarity it provides, a point where operational detail and financial strategy meet.

Where AI actually adds value

The balance between control and efficiency is also shaping how finance teams deploy AI across the payables process. AI attracts a lot of noise, but in most AP teams the reality is quieter.

“We’ve been using AI in invoice processing for more than a decade,” says Juneau. “Often customers don’t even realise it’s there – and that’s how it should be.”

Today, what is changing is how AI is now being applied further along the process, from anomaly detection and exception handling to predictive insights around cash flow.

That expansion, however, brings a different set of questions. As AI moves deeper into the process, finance leaders want to understand how models work, whether decisions can be explained and how data is governed. Recent product updates from providers such as xSuite point in the same direction, using AI to improve line-level accuracy and exception handling through intelligent agents rather than removing human oversight from approvals.

“Fully autonomous approvals make most finance leaders uncomfortable,” Juneau notes. “They want to know when human judgement is applied and why.”

That caution is shaping how AI is deployed in practice. There are also concerns around data exposure, particularly with the rise of large language models (LLMs). Assurance that sensitive financial data remains protected is now a prerequisite for AI deployment.

The goal is straightforward: fewer low-value tasks; cleaner exceptions; and better decisions, without shifting accountability away from the finance team.

“No one expects AI to be 100% accurate,” says Fanarredha. “What matters is being clear about materiality, where automation makes sense and where humans stay in the loop.”