Speed, reliability and visibility now shape how many companies judge trade finance providers. A delayed document check, unresolved discrepancy or slow compliance review can postpone cargo release, disrupt production schedules or extend working capital cycles.

In documentation-heavy markets such as Egypt, these frictions can determine whether a manufacturer receives inputs on time, whether a distributor can replenish stock or whether an exporter gets paid within the expected cycle.

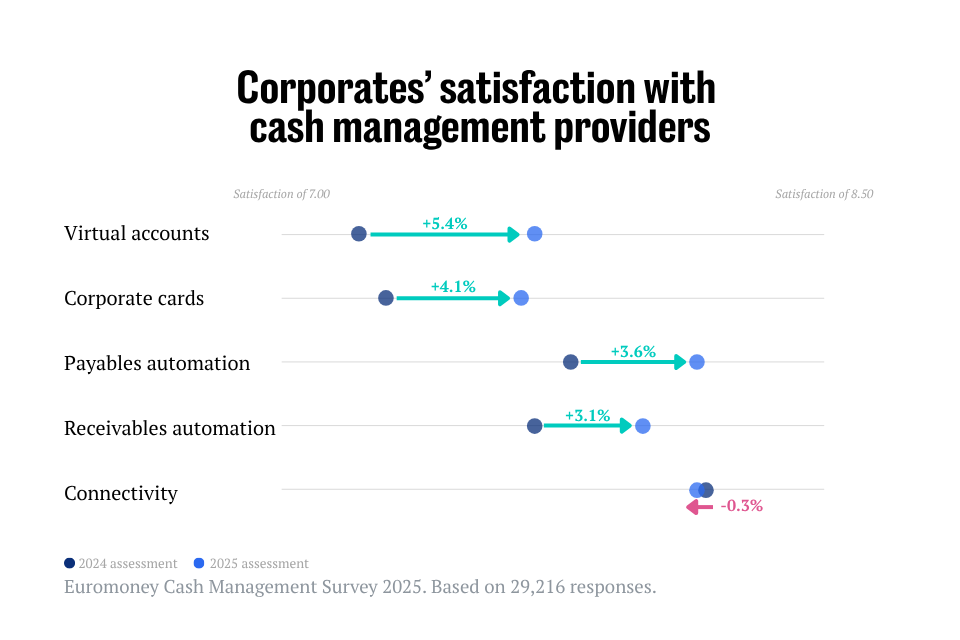

This reflects a broader shift across global trade finance. In Euromoney’s 2025 Trade Finance Survey, corporates consistently highlighted that “guidance and transparency mattered as much as product availability”, underscoring how operational execution and client experience are becoming increasingly central to trade finance relationships.

The shift is visible across African trade corridors, where fragmented documentation processes, uneven digitisation and cross-border compliance requirements continue to affect transaction flows.

Why operations now matter more

Letters of credit, documentary collections, guarantees and receivables-backed structures all depend on the accurate movement of information between clients, banks, shipping companies, customs authorities, insurers and correspondent banks.

For corporates, the issue is predictability. Delays in documentation or approvals can create uncertainty around inventory, liquidity and supplier relationships. This is especially acute for import-dependent manufacturers and high-volume distributors, where timing affects both production continuity and cash conversion cycles.

Operational execution has become even more important as some corporates seek to optimise inventory and working capital cycles more aggressively. Treasury teams at the more sophisticated corporates increasingly expect real-time transaction visibility, faster discrepancy resolution and seamless integration between trade finance, payments and foreign exchange management.

Trade transformation in Egypt

Egypt offers a useful case study because trade finance remains highly documentation intensive. At Commercial International Bank (CIB), the response has been to treat execution quality as a strategic priority rather than a back-office concern.

“CIB has launched a trade transformation project to reduce end-to-end processing turnaround time, enhance client experience, and improve trade processes through automation and near-STP,” says Islam Zekry, Group Chief Finance and Operation Officer and Executive Board Member.

That transformation programme’s first phase has focused on workflow automation, system integration and reducing manual intervention across trade operations. This includes integrating limits with core systems, automating collateral reservation for time deposits and certificates of deposit, and streamlining internal communication through tracer automation.

CIB is now building on that foundation by targeting the more complex and labour-intensive aspects of trade processing through artificial intelligence (AI) deployment.

“The second phase of the project presents advanced document recognition, examination, and business analytics,” says Zekry.

According to CIB, the system is designed to automate screening, discrepancy checks, document classification and validation against international, local and internal banking rules. It uses optical character recognition, natural language processing, machine learning and cognitive AI to extract and validate data from scanned and electronic trade documents in English and Arabic. Additional functionalities include vessel tracking and commodity price monitoring.

But CIB’s AI initiative is not a standalone technology experiment. It sits on top of a broader operational transformation programme designed to improve turnaround times, visibility and process consistency. That distinction matters because AI tools are most useful in trade finance if they are embedded within controlled workflows, clear approval processes and well-governed operating procedures.

The limits of digitisation

Digital tools can reduce errors, improve transparency and help banks scale trade operations. But trade finance in Africa remains difficult to automate fully. Transactions are exception-heavy, documentation standards vary, and external parties often operate at different levels of digital maturity.

There is also a legal dimension. UNCITRAL’s Model Law on Electronic Transferable Records is intended to give electronic transferable records legal effect equivalent to paper-based instruments, but adoption remains uneven globally. Until more jurisdictions recognise electronic trade documents consistently, banks and corporates will continue to operate in a hybrid world of digital workflows and physical documentation.

At the same time, digitisation is introducing new forms of operational and fraud risk. Euromoney’s 2025 Trade Finance Survey highlighted growing concerns that generative AI tools are increasingly being used to forge trade documents and manipulate data. As banks automate more aspects of trade processing, the need for stronger verification, anomaly detection and cybersecurity controls is becoming more acute.

This is why operational efficiency cannot be separated from risk control. Faster processing is valuable only if it preserves auditability, regulatory compliance and documentary integrity.

At CIB, Zekry says trade operations and branch network teams operate through standardised procedures that incorporate risk and regulatory considerations. “Prior to implementation, each standard operating procedure is reviewed and approved by the Operational Risk, Compliance and Customer Rights Department,” he says.

A broader African differentiator

The same execution challenge is visible across African trade corridors. In markets where ports, customs, correspondent banking, local regulation and client documentation practices do not always move in sync, operational reliability becomes a source of competitive advantage.

For banks, the next phase of trade finance competition may be less about who can provide access in principle, and more about who can execute reliably in practice. Balance sheet strength will still matter, but so will workflow design, document intelligence, client interfaces, compliance integration and the ability to give corporates confidence that transactions will move predictably from initiation to settlement.